16.08.2022 - Comments

Since prices in supermarkets have risen, there has been intense discussion about inflation and its social consequences at the dinner table at home and in the social media. Not so long ago, it was a special topic that only economists were interested in.

When people discuss inflation, they usually refer to consumer prices. These have risen by an average of two percent a year since 2014. If you ignore the rise over the last 12 months, the price increase was actually only around one percent - too low to leave a footprint on society.

But consumer prices do not fully describe inflation. In fact, there has already been tremendous inflation over the last eight years. It was so strong, that it changed our society significantly. However, one did not notice this at the supermarket checkout. It occurred on capital markets and on real estate markets and is referred to as asset price inflation.

Asset price inflation describes the price increase of real assets (e.g. real estate or business wealth) and financial assets (e.g. saving deposits or fund shares). The price of such assets is not included in the calculation of the consumer price index.

Since 2014, asset prices raced off. The average annual increase in asset prices has been six percent, significantly greater than the much-discussed consumer price inflation. In the fall of last year, asset price inflation was as high as twelve percent.1 A level that has not been reached even recently for consumer prices.

Admittedly, the picture seems to have turned around in the first half of the year, as consumer price inflation (over seven percent) is for the first time above asset price inflation (three percent) again. Nevertheless, the asset price inflation of recent years has left its footprint on our society. The resulting structural changes will be felt for decades, if not irreversible.

While all population groups generally suffer from rising consumer prices, this is different in the case of rising asset prices: Those who own assets benefit from them. However, asset price inflation also describes how much more expensive it has become to build up wealth. So if asset prices rise, it becomes all the more difficult for anyone who does not own any assets worth mentioning to build up wealth and thus a standard of living and retirement provision.

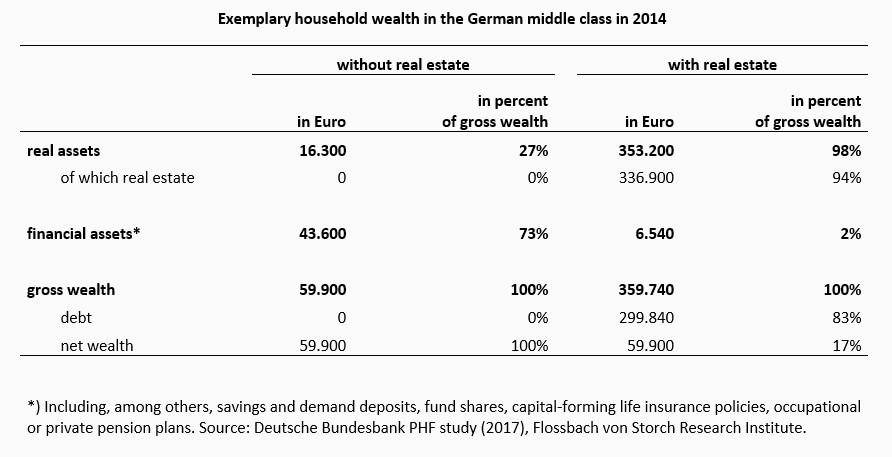

This becomes clear in an exemplary comparison of two households typical of the German middle class2. For this purpose, we consider two households that have the same net wealth, but with one important exception. The first household owns a real estate property, the second one does not. As equity, the first household has contributed 85% of its financial assets for this purpose. The debt of the real estate owner is equal to the value of the real estate minus the equity contributed.

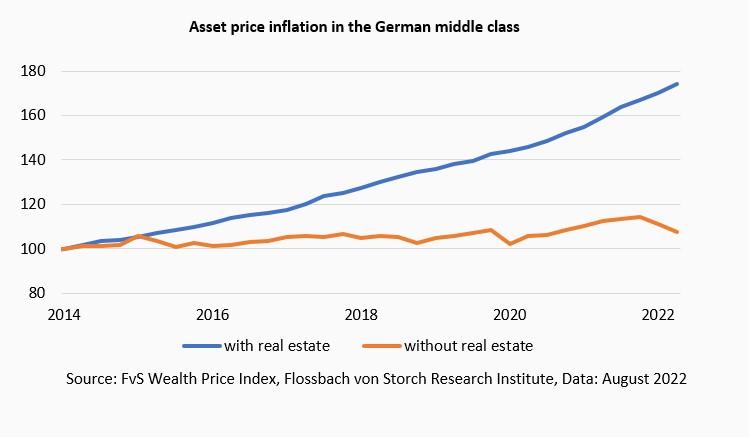

The bottom graph shows how asset prices have evolved for the two households. Excluding real estate, there has been no significant asset price inflation for the typical middle-class household. Just under one percent annually, the prices of what they own have risen. Cumulatively, this corresponds to a price increase of only seven percent over the eight-year period.

With real estate ownership, this looks entirely different. Within the relatively short period of eight years, real estate owners in the German middle class can enjoy a 74% increase in the price of their assets. The reason for this is that their real estate has risen in price by 79%.

The difference in asset price inflation between the two households corresponds to the increased cost of wealth accumulation, which has arisen in addition to the other benefits of real estate ownership. Accordingly, wealth accumulation has become 67% more expensive in eight years, making it seriously more difficult3. Only the very few will be lucky enough to have a salary increase to compensate for this.

It is not only real estate ownership that makes a difference. Other assets such as business wealth (55% increase in price since 2014) or shares (32% increase in price since 2014) have also become significantly more expensive over the period. Ownership of these two types of assets also varies strongly between social classes.

Even though asset price inflation has eased significantly in the past two quarters and the development of some asset prices may be volatile, structural changes in the cross-section of German households will persist for a long time to come.

Asset price inflation in Germany is closely related to economic growth and to the monetary policy of the European Central Bank (ECB). The ultra-loose monetary policy of recent years has caused asset prices to rise massively. Since wealth is not equally distributed among the German population, inflation has exacerbated structural wealth inequalities in the cross-section of wealth, age, occupational groups, etc. The next rung on the wealth ladder has now become out of reach for many households.

Given these findings, it is surprising that the inflation issue has only recently gained public traction. It would have deserved a central place in the public discussion already in the past eight years.

1 Cp. Wealth Price Index for Germany: Q3-2021.

2 The household wealth composition is derived from the PHF study of the Deutsche Bundesbank (2017).

3 Difference in asset price inflation: 74% - 7% = 67%

15.08.2022 - Wealth Price Index

15.07.2022 - Macroeconomics

by Thomas Mayer

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.