28.03.2020 - Comments

![[Translate to English:]](https://www.flossbachvonstorch-researchinstitute.com//fileadmin/_processed_/9/1/csm_kommentar-pablo-duarte-klein_dcf2d22790.jpg)

The corona crisis has caused the strongest capital outflows from emerging and developing countries in recent history. The next turbulences are close.

The COVID-19 pandemic has caught emerging and developing economies in bad shape. Not only are their health systems overwhelmed and large segments of their population are very poor and employed in the informal sector, but also their levels of external debt and current account deficits are high. With the outbreak of the coronavirus in Europe, the US Dollar has appreciated as investors looked for safe havens causing an unexpected dry up of foreign financing in emerging markets: a “sudden stop”. As the daily tracker by the IIF shows, the size of the outflows are the largest in recent history. The vulnerability of an economy to the sudden stop depends on its macroeconomic conditions before the shock, its access to dollars and its capacity for economic policy reaction.

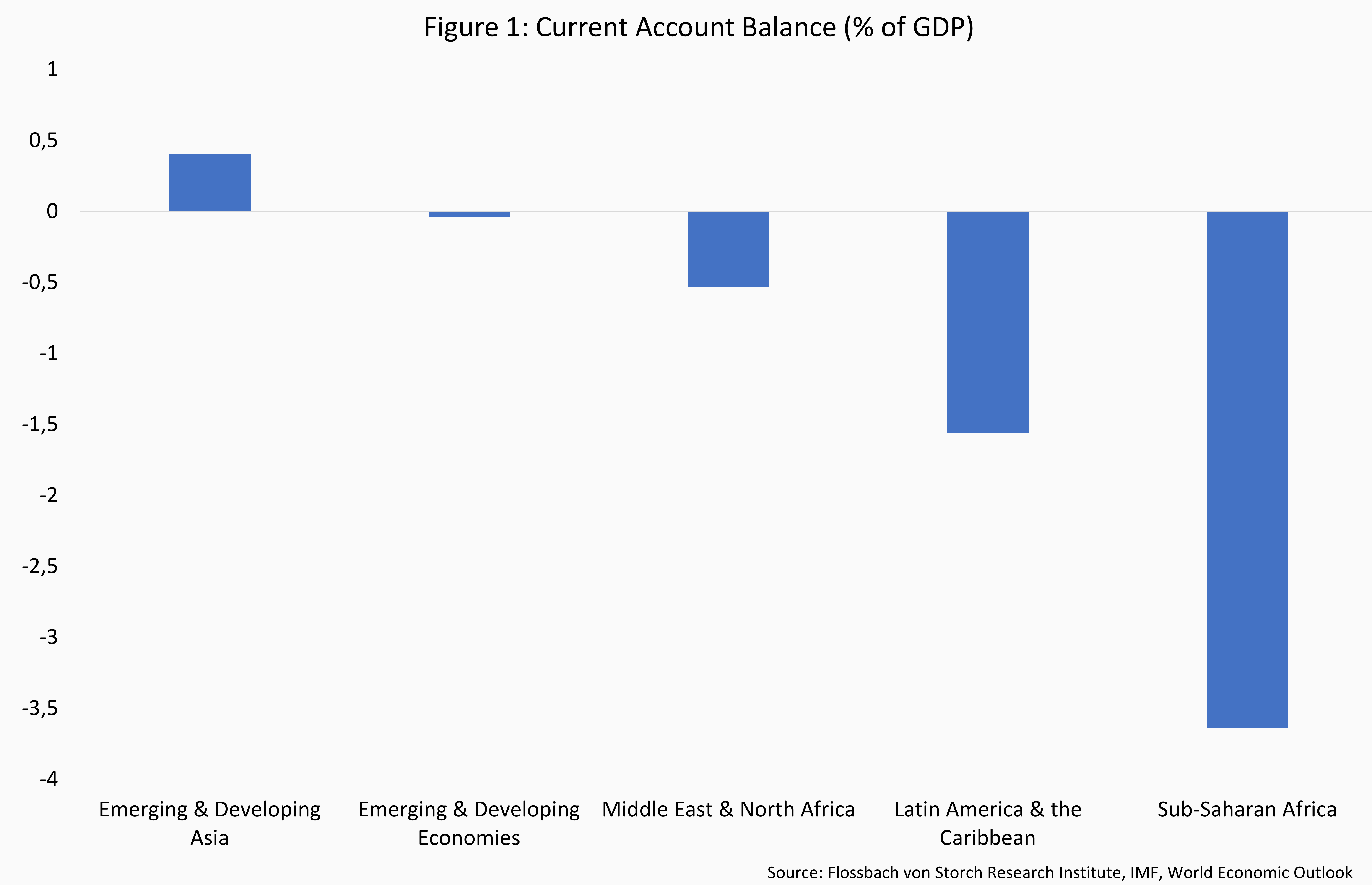

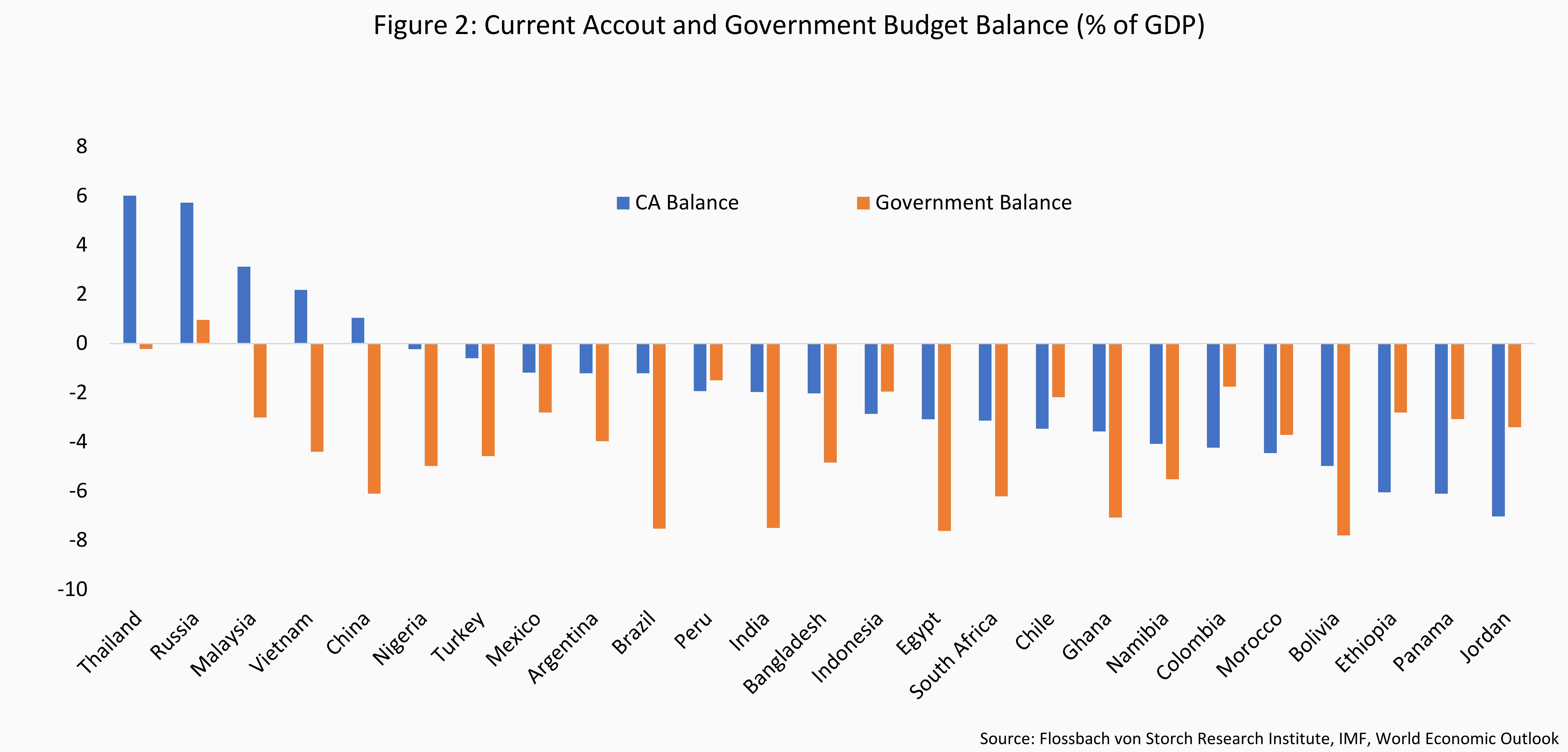

A first relevant macroeconomic condition is the current account balance. Before a sudden stop, current account deficits are financed with foreign capital. Without capital inflows, large current account deficits become unsustainable. Figure 1 shows the current account deficit as percent of GDP for different regions by the third quarter of 2019. The strongest deficits were in Sub-Saharan Africa and Latin America. Emerging and Developing Asia had a current account surplus mainly driven by Thailand, China and Vietnam (Figure 2). India, Indonesia and Bangladesh, however, had strong current account deficits.

But, is a flexible currency not an equilibrating device for current account imbalances as exports become cheaper and imports more expensive as the local currency depreciates? In the current situation of contracted global demand and supply, exports are not likely to meet a sufficiently high demand in international markets even with the strong appreciation of the dollar seen in the past weeks. Moreover, the academic literature shows that in the recent past, flexible exchange rates have only partially helped to readjust global imbalances. Fiscal and monetary policy stances have been more relevant.1

The second macroeconomic condition is the level of (dollar-denominated) external debt. As the sudden stop leads to a depreciation of the local currencies with respect to the US Dollar, dollar-denominated debt explodes making repayments harder and refinancing in the currently distressed international financial markets almost impossible. In October 2019, the IMF warned in its Global and Financial Stability Report of an increase in public and private debt thanks to low global interest rates as it could increase the risk of debt distress due to the countries’ increasing reliance in external finance. As Figure 2 shows, apart from the current account deficit many countries also had a worrying government budget deficit (twin deficit) in 2019.

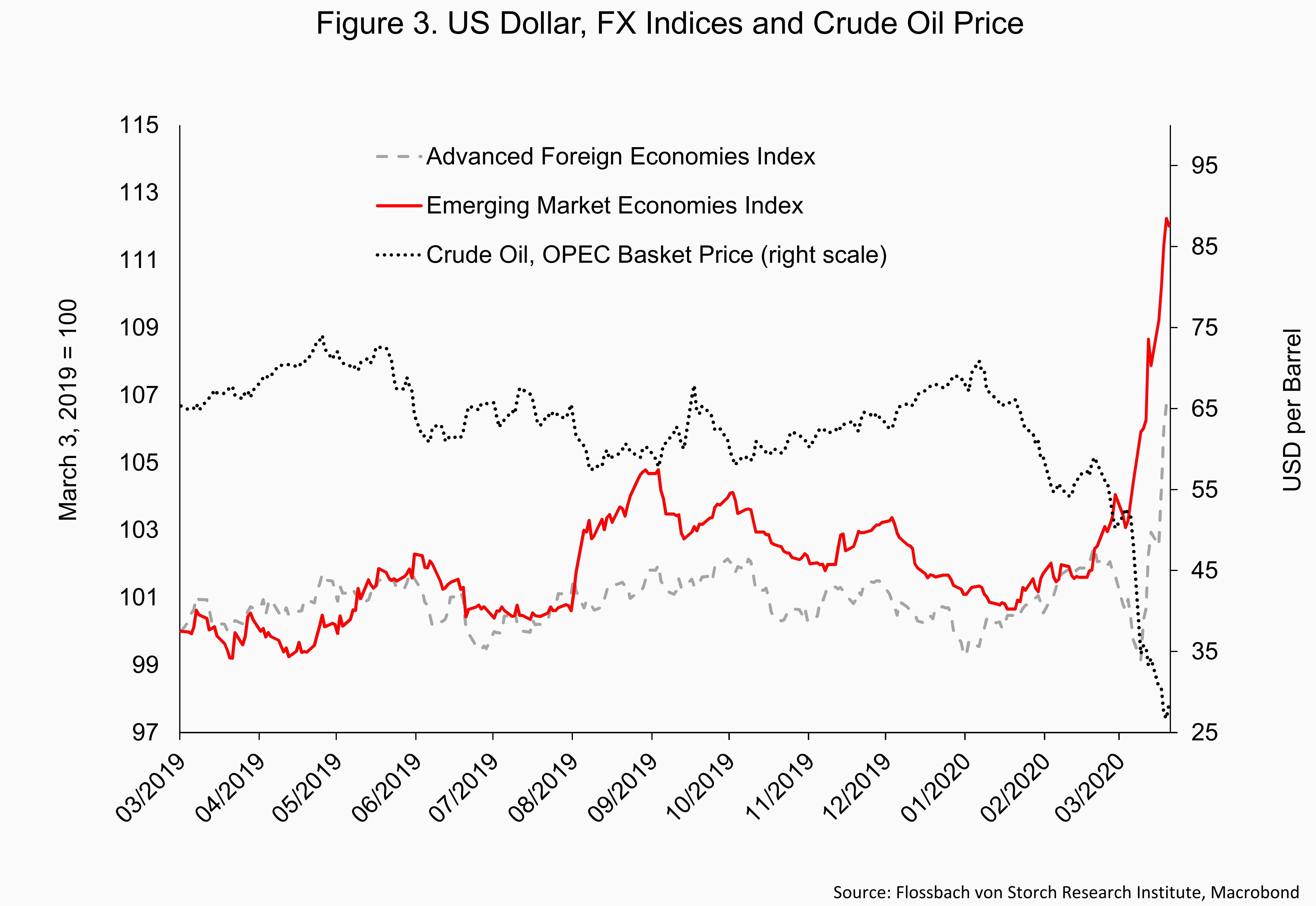

On top of the COVID-19 sudden stop, the US Dollar has suffered further appreciation pressure thanks to the Saudi-Russian oil war: On March 9th oil prices dropped from 50 to 35 dollars per barrel in one day (Figure 3). In reaction to the higher international demand for US Dollars, the Federal Reserve temporarily extended its dollar swap lines to 9 central banks to allow them to provide US dollar funding in their own countries. The new swap lines were approved for the central banks of Australia, Brazil, Denmark, Korea, Mexico, New Zealand, Norway, Singapore and Sweden. Countries with some of the most distressed currencies such as Russia, South Africa and Indonesia were not included.

Without a dollar swap line, with considerable current account deficits, high levels of external debt, low commodity prices (which also means lower revenues for commodity exporters, governments and state-owned enterprises) and distressed global demand, there is little that traditional economic policy measures can do to contain the risks. The space for fiscal policy is reduced by the already high levels of debt and the need for dealing with the public health challenges of the COVID-19 pandemic. Numerous governments have implementing lockdowns in big cities making government spending even more important to alleviate the life-threatening decline in the incomes of the poorest citizens. Central banks face the dilemma of increasing interest rates to support their currencies and prevent inflation or lowering them to support growth. The central banks in South Africa and Colombia, for example, have chosen the latter and have even started asset purchase programs to provide additional liquidity. Fearing that reserves can be quickly depleted, capital controls for capital outflows could make a comeback.

Emerging market economies are not facing a cloudy horizon. They are in front of a hurricane of serious financial distress despite the ease in the pressure on the dollar due to the latest cash injections by the Federal Reserve and measures local governments can take. Without a rapid recovery of global demand in sight (Europe and the US are still in quarantine), the IMF and the World Bank should be ready to step in with enough funding to help emerging market economies in financial distress. Even if the multilateral institutions would announce to do “whatever it takes”, by for example a major issuance of special drawing rights (SDR) as recently suggested by some economists, the next round of financial turmoil will likely come from the emerging markets.

18.05.2018 - Economics, Politics & Philosophy

by Thomas Mayer

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.

Pablo Duarte

Senior Research Analyst

Pablo Duarte joined the institute in 2020. He earned a PhD in economics from Leipzig University and was a visiting researcher at New York University. He studied economics at Leipzig University and Universidad del Rosario (Colombia). Pablo Duarte’s research interests include international macroeconomics and economic policy.

All articles by Pablo Duarte