25.05.2022 - Studies

Warren Buffett knows the ketchup-bottle effect all too well. Not only because as a burger fan he likes to reach for the sugared tomato mixture himself, but also as an investor. After one of the stock market veteran's core holdings announced billion-dollar write-downs in February 2019, the share price plummeted: Kraft Heinz, in which Buffett's holding company Berkshire Hathaway owns 26.7 per cent, fell to a record low at the time.

The US company, known worldwide for its ketchup, announced write-downs of 15.4 billion dollars. This included a good seven billion dollars on the goodwill reported in the balance sheet.

This is an item on the assets side of the balance sheet that always appears after takeovers when the acquirer pays more for a subsidiary than can be found there in assets on the books. This goodwill can be popularly described as a takeover premium.

A premium with shaky value, as the example of Kraft Heinz has shown in the past. Recently, at the end of April this year, Teladoc Health, one of the leading US telemedicine companies, surprised its investors with a 6.6 billion dollar write-down on its goodwill. The news was met with heavy markdowns. Teladoc's share price fell to a four-year low.

Two things can be seen from this: Goodwill, which can be found on the assets side of a balance sheet, has great relevance, but it is obviously difficult for outsiders to grasp. That is why devaluations surprise investors time and again.

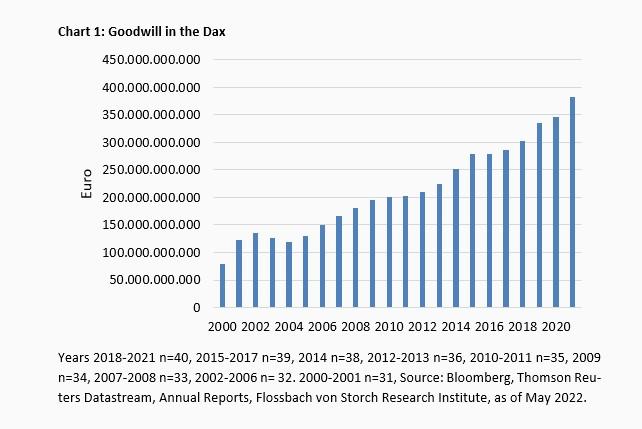

An analysis of the 40 Dax companies is worthwhile as an example of the importance of goodwill. With a good 381 billion euros at the end of the 2021 financial year, they accounted for around 4.6 percent of the global goodwill of around 9,400 billion dollars (Figure 1). Both are record figures. At the same time, the Dax accounted for only 1.6 percent of the global market capitalisation of all shares at the end of 2021. The importance of goodwill for Dax companies is therefore outstanding in relative terms.

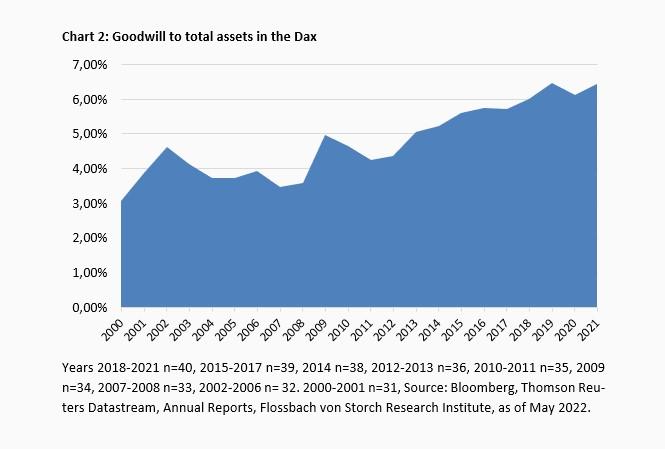

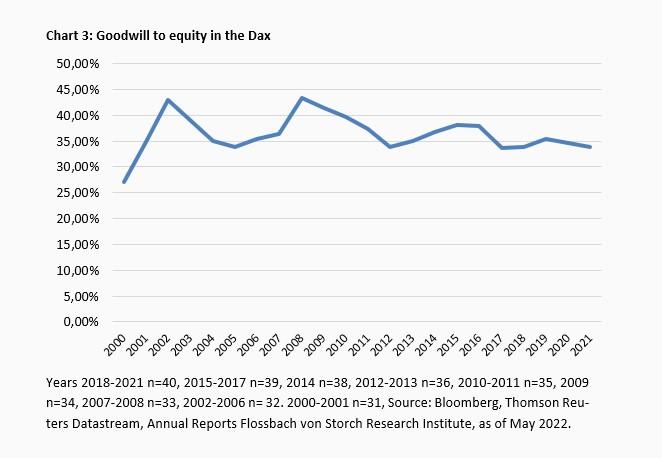

Dax companies are also top in terms of ratios within the balance sheet. According to a study by Capital IQ, the ratio of goodwill to equity is around 18 percent for all listed companies worldwide and three percent of total assets. At Dax companies, on the other hand, goodwill recently accounted for a good 6.4 percent of all assets, more than double the global average, and almost 34 percent of equity (charts 2 and 3).

In terms of goodwill, Dax companies are therefore in a leading position in terms of relevance for corporate analysis. In principle, the question of the recoverability of the respective goodwill has been pressing for a long time.1

But how exactly does this come about?

When a company such as the German Bayer buys the weedkiller manufacturer Monsanto or Microsoft acquires the professional network LinkedIn, the accountants have to account for the new acquisition using the so-called purchase method. All assets and liabilities of the acquired company must first be revalued.

The result is the revalued net assets, calculated from the difference between assets and liabilities. This is then compared with the purchase price (technical jargon: fair value of the consideration transferred). If the purchase price exceeds the net assets, this difference is posted as goodwill on the assets side of the balance sheet. In rare cases of badwill (assets higher than purchase price), this is included in the acquirer's income statement as a profit contribution.

Goodwill is supposed to correspond to the value of supposedly unidentifiable net assets of the acquired company. The capitalised goodwill is in turn to be allocated to so-called cash generating units (CGUs), which are to benefit from the synergies of a business combination.

Until the beginning of the century, companies were obliged to amortise goodwill ratably, just like other tangible assets. This method regularly reduced profits and therefore lowered the increase in equity capital or, in the case of losses, depressed it more than without goodwill amortisation.

In the course of the technology stock crash after the turn of the millennium, this would have led to an accelerated erosion of corporate balance sheets well filled with takeover premiums. However, this prevented successful lobbying by US companies.

Since 2001, companies reporting according to US standards have been allowed to forego the uniform devaluation of goodwill. Since then, they have - as before - reviewed the value of their goodwill on an ad hoc basis, but in any case now once a year on the basis of the management's assumptions. The procedure for this is called an impairment test. 2

What is right for the US Generally Accepted Accounting Principles (GAAP) is right for its younger brother, the International Financial Reporting Standards (IFRS). The accounting rules, which were born out of Europe and are applied in more than 150 countries, introduced impairment-only for financial years beginning on or after 31 March 2004.

The established management approach, the valuation of goodwill on the basis of assumptions made by the company itself, was justified by the rule-makers on both sides of the Atlantic on the grounds that the management boards would be best able to assess the economic situation of their respective new subsidiaries. The expectation was that there would not be lower write-downs on goodwill in total, but only at more irregular intervals.

But the assumption that the "good guy" would already fix his balance sheets has proven to be wrong. As a result, the S&P 500 companies alone now have $3.7 trillion in goodwill on their balance sheets. For all listed US companies together, the value is about two trillion dollars higher. And in the European Stoxx 600, the goodwill of all companies is just under 2.9 trillion euros.

The trend of low depreciation and sharply rising goodwill positions in the course of takeovers, which has now lasted for 20 years, is viewed critically, especially by parts of academia. For one thing, organically growing companies are disadvantaged on the balance sheet.3 On the other hand, goodwill should actually be a residual item that eventually evaporates from the balance sheet.

However, since there are numerous possibilities to change the assumptions for the impairment test in a way that is favourable to the company, there is a danger that goodwill will degenerate into a residual ramp. This is then regularly only emptied in the course of a manifest crisis. Until then, management can adjust interest rates or planning horizons, or re-calibrate CGUs in order to postpone or at least minimise devaluations.

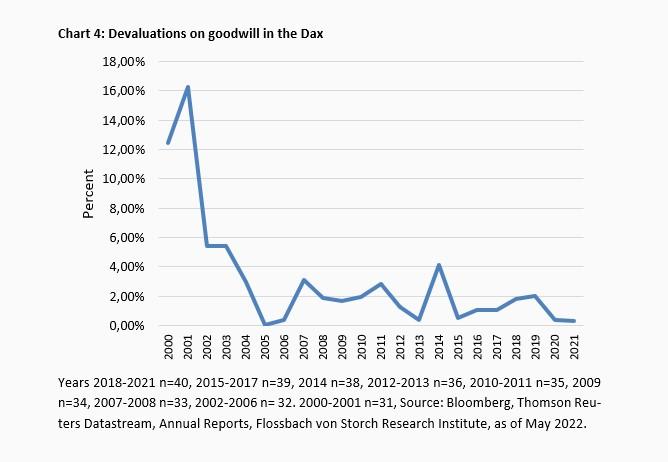

In any case, the introduction of impairment-only,also according to the IFRS rules applicable in Germany for stock exchange-oriented companies, immediately had the effect that write-downs on goodwill at the (current) Dax companies fell to almost zero. Apart from individual outliers, write-downs of takeover premiums have remained at a very low level since the method was introduced (chart 4).

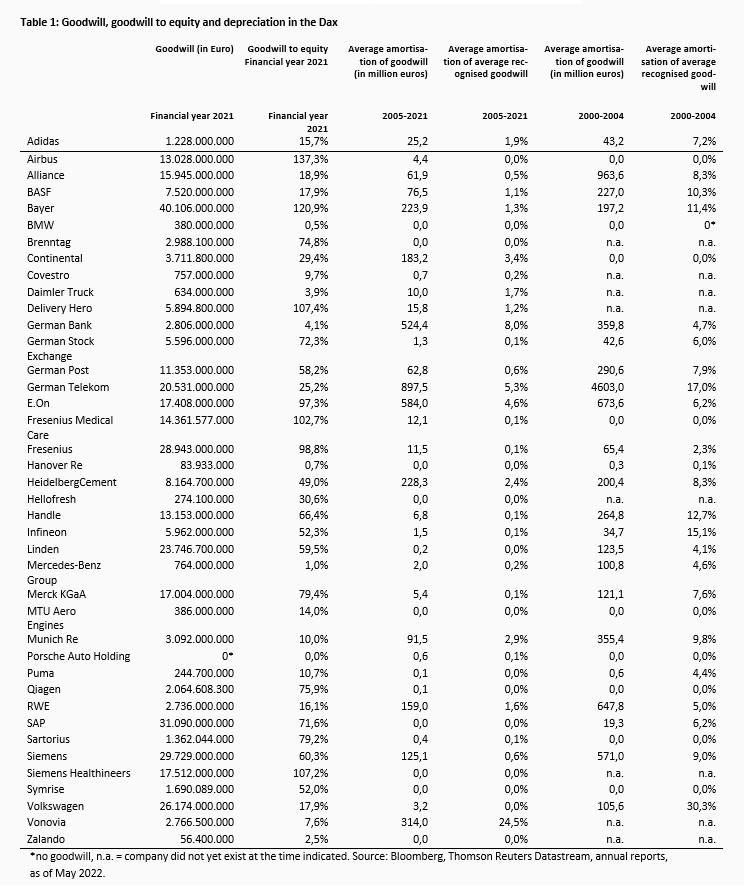

So it is hardly surprising that a large part of the write-offs that the current Dax companies have made at all stem from the years 2000 to 2004. In this five-year period alone, the corporate leaders wrote off about 49 billion of the total of almost 110 billion euros in write-offs since 2000.

At that time, only 31 (until 2001) and 32 (from 2002 onwards) of the current Dax-40 companies existed, which makes the lower devaluations in recent times seem even more critical. Finally, the volume of goodwill is currently significantly higher than 20 years ago - by a factor of three.

In the years 2000 to 2004, the devaluation averaged 8.5 per cent of the previously recognised goodwill. In the 17 business years thereafter, it was only 1.4 per cent or one sixth of that.

High devaluations are exceptions. One of these was delivered by the Dax corporation Continental, known primarily for its tyre division, and justified this in its 2019 balance sheet as follows: "As part of the annual planning process, global production of passenger cars and light commercial vehicles was not expected to improve significantly in the coming years (2020-2024). Due to this triggering event and the other key assumptions made in the context of determining the value in use of a cash-generating unit, such as free cash flows, the discount rate, its parameters and the sustainable growth rate, there was an impairment of goodwill in the amount of €2,293.5 million."4

So three years ago Continental was looking ahead to 2024 - five years is a usual, manageable horizon for goodwill.

How people in 1700 would have imagined an unmanageable horizon up to the year 2022, assuming interest in such a question, is something no one today can guess exactly. In any case, the incumbent board members of the companies have great visions in 2022, because judging by the most recent annual amortisation of goodwill, the Dax managers assume that their acquired subsidiaries will still have a residual benefit in 2344.

That would be as if the first steam engines, tested more or less successfully at the beginning of the 18th century, were still playing a leading role in the economic context today.

Since goodwill, like practically all assets, is not an eternal item on the balance sheet, investors should be aware of the more or less high risks of devaluations. Companies rightly emphasise that goodwill write-offs, which are often unexpected by the market, are not cash-effective. However, they are an admission that acquisitions do not make the hoped-for contributions after all and that too high a purchase price was paid for them in the past. Since goodwill impairments depress profits or lead to losses, they threaten equity.

How strong is, of course, an individual matter. For example, the current goodwill-to-equity ratios of Dax companies range from 0 to a good 137 percent. It can also be seen that the average devaluations on average goodwill have regularly decreased significantly since the introduction of impairment-only (Table 1).

A loss of equity is not trivial: leverage factors increase; agreements prescribing certain ratios, for example on gearing (net debt to equity), could be called into question after a goodwill write-off.

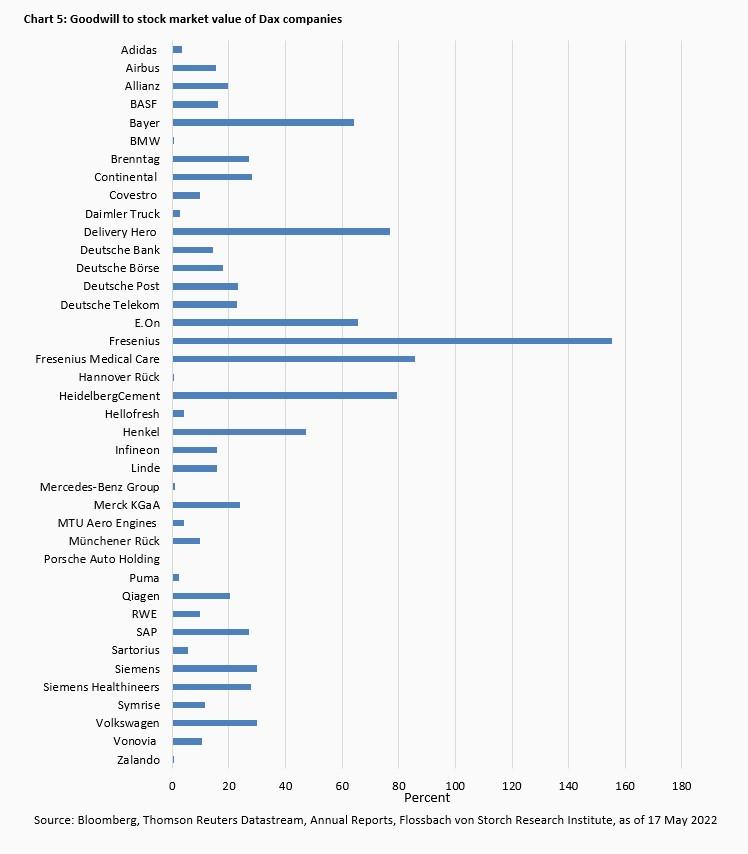

The stock market always gives a vote of no confidence, at least superficially, when the stock market value of a company is close to or even below its reported goodwill. Since goodwill is the most vulnerable item in fixed assets to devaluation, a high ratio of goodwill to market capitalisation expresses a sceptical attitude towards its intrinsic value. Here, too, the ratios in the Dax are far apart (chart 5).

High goodwill is also a strong indication that the company in question pursues a business model characterised by acquisitions. Low goodwill either indicates that it has been or had to be devalued at least irregularly. Or the low value indicates that the company does not operate in a takeover-driven manner, or only to a limited extent.

Goodwill can be shaken by, among other things, a currently expected shortfall in previously hoped-for target figures, a change in the internally assumed and external interest rate levels or rule changes.

Airbus, for example, recently calculated internal rates of return (weighted average cost of capital, WACC) of 8.3, 9.3 and 11.0 percent, before tax, for its various divisions. This was significantly lower than in the previous year.5 The chemicals trader Brenntag reduced the risk-free interest rate in the WACC used to discount the cash flows from 0.2 to 0.1 per cent. The Dax group left the additional market risk premium at 7.75 per cent.6

However, now that a general upward turn in interest rates is more than indicated for the first time in a long time, both in the dollar area, the euro area and worldwide, goodwill positions could come under pressure. This is because the higher the discount rate of future cash inflows, the lower their current value, which is a measure of goodwill's recoverability. At the very least, it would be questionable if companies' assumptions decoupled from the market.

It is possible, however, that such considerations will play less of a role in the future - should forces prevail that call for a return to ratable amortisation of goodwill.

It is true that there has been discussion for years about changing the balance sheet rules again in this regard. However, this has not yet materialised. For example, the International Accounting Standards Board (IASB), which is responsible for IFRS, recently examined whether the impairment test for goodwill could be made more effective and less complex. According to this, the IASB is "provisionally of the opinion that there is no alternative test that can address goodwill better and at a reasonable cost". And with regard to a gradual amortisation of goodwill over a time axis, the IASB - also "provisionally" - is of the opinion that the existing approach should be retained. This is the "best way" to be able to "hold a company's management accountable for its acquisition decisions".

The situation is quite different in the USA. The Financial Accounting Standards Board (FASB), which is responsible for US GAAP, has at least concrete plans to regularly amortise or write off goodwill in parts. If this regulation is to come, then a standard period of ten years is in the offing. According to the FASB, it will be several months before decisions on this can be published. After that, a phase of renewed consultations would follow in order to finalise the guidelines. The FASB also plans an extensive transition period of at least one year to allow companies to implement the guidance. In short, the new guidance would not take effect for several years, the FASB said in response to a request from the Research Institute.

The IASB would then hardly be able to avoid this. Such a divergence in accounting would make the IFRS, which are mainly applied outside the USA, appear almost superfluous. Especially since the auditing firms, as important stakeholders of the IASB, are in favour of abolishing impairment-only anyway, there is likely to be pressure from this weighty side to follow America's guidelines once again in case of doubt.

Investors should also prepare for a turnaround with regard to goodwill. For too long, this balance sheet item has weathered all storms - on paper. The current sharp upward corrections in interest rates, and in market valuations, should be reflected in balance sheets sooner or later. On the asset side, goodwill is there in the first place. It would be unsurprising to see more high goodwill impairments in the future.

The FASB could change the game completely. If companies had to regularly devalue their goodwill again and a ten-year period was introduced for this purpose, net corporate profits worldwide would be reduced by more than 900 billion dollars per year. This would correspondingly reduce the equity base of companies or severely curb growth.

In the Dax, measured against the current 40 members, a good 38 billion euros in net profits would be wiped out annually - this corresponds to an estimated one-third of the net earnings in a record profit year for the Dax companies or roughly half of an average year.

1https://www.flossbachvonstorch-researchinstitute.com/de/studien/mit-viel-gutem-willen/

2 Goodwill arising from acquisitions must be tested for impairment at least once a year and at any time when there are indications of impairment. However, this is not done as a single sum, as the goodwill must be allocated to assets of several business units and thus has separable cash flows. The impairment test is therefore carried out at the level of these business units (cash generating units, CGU). The book value of the CGU is compared with its recoverable amount, which corresponds to the higher of value in use and fair value less costs to sell. If the carrying amount exceeds the recoverable amount, it is written down to the latter.

4 Continental Annual Report 2019, page 61

5 Airbus Annual Report 2021, page 280 (Financial Statements 2021, page 35)

6 Brenntag Annual Report 2021, page 182

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.

Christof Schürmann

Senior Research Analyst

At the Institute since 2022. The graduate in business administration (FH), previously worked as a journalist and deputy head of "Money" at WirtschaftsWoche. The trained banker and book author ("Die Bilanztrickser") taught balance sheet research part-time at the private university BiTS in Iserlohn.

All articles by Christof Schürmann