18.03.2020 - Studies

As an answer to the looming economic crisis amid the coronavirus pandemic, several governments in the euro area announced very substantial rescue packages.

Moreover, on March 16 the European Commission announced to apply full flexibility provided for in the EU fiscal framework. All this will lead to strongly increasing public debt within the euro area. For a number of countries the debt will not be sustainable without ECB support.

Corona-driven fiscal expansion

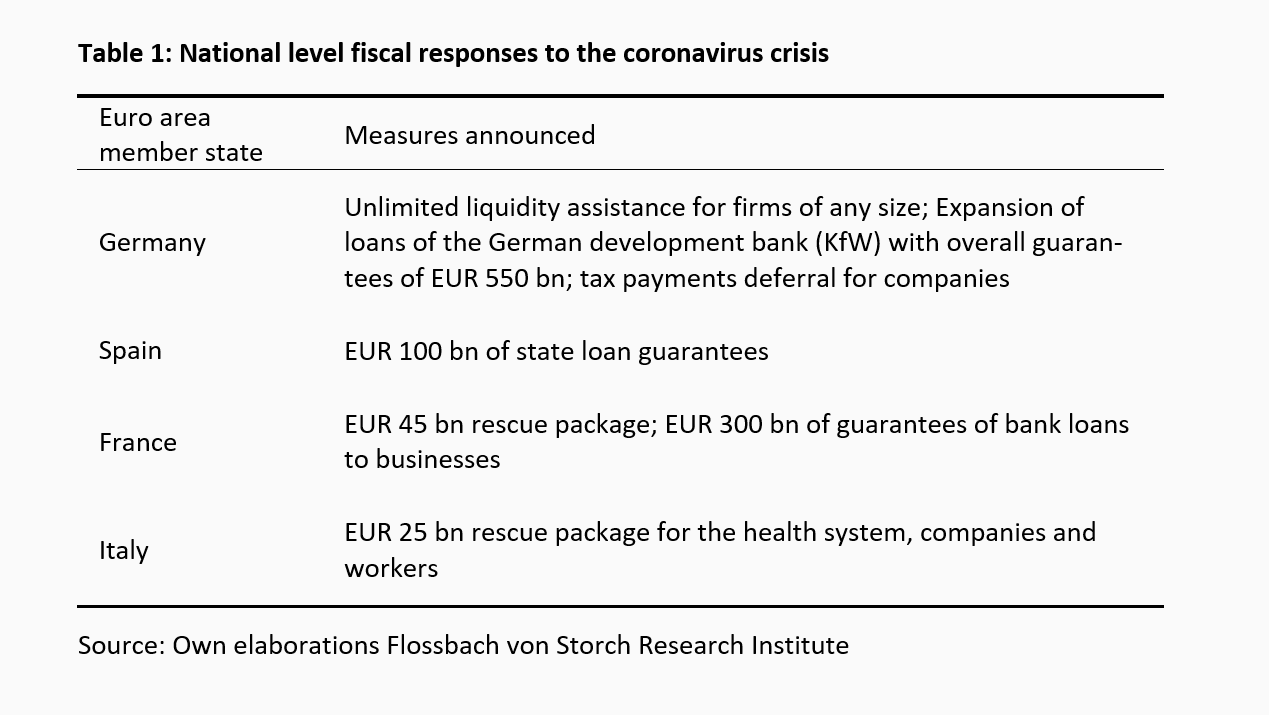

So far, all major euro area member states have reacted with very decisive fiscal responses to the Coronavirus. Table 1 shows a summary of the announced packages. Further measures can follow.

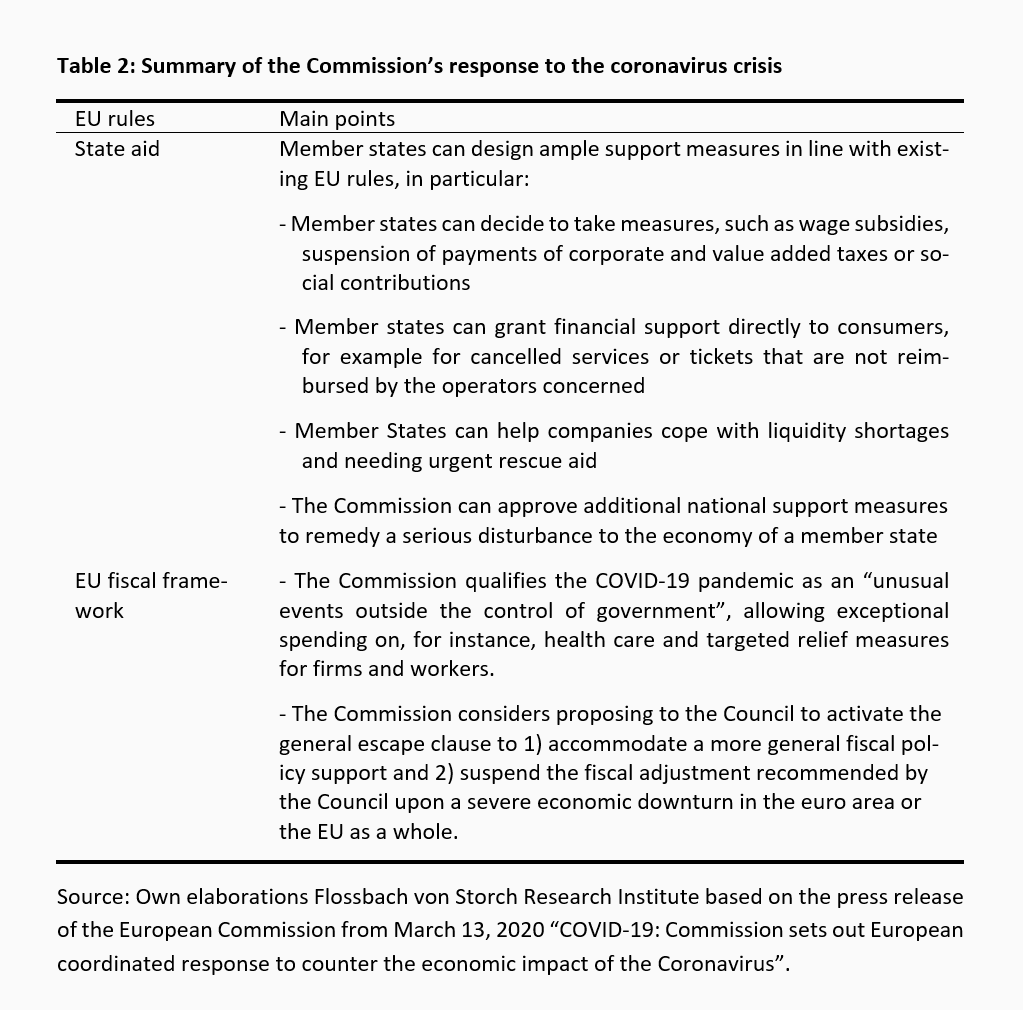

Among the main measures taken upon the “European coordinated response to counter the economic impact of the Coronavirus”, the Commission decided that the member states are allowed to exploit the maximum flexibility and leeway in EU debt, deficit and state aid EU rules for companies. Table 2 summarizes the main points.

However, due the strong rise of public debt across the euro area over the last decade, the fiscal space to widen government finances is very limited for several of the euro area member states. The most acute situation regards Italy: due to the corona crisis, the debt to GDP ratio in Italy could reach almost 150% in 2021.1 The use of flexibility of the EU rules postpones but it does not cancel the need of the fiscal adjustment. Consequently, doubts over the survival of the euro might soon rise, calling the ECB to assume its role as a lender of last resort.

ECB options

To this end, the ECB could use two options:

Option 1: OMT

The ECB can eventually activate the so-called Outright Monetary Transactions (OMT) program.

The program is subject to conditionality in terms of strict and effective fiscal conditions. In particular, a pre-condition for OMT is the attachment to an appropriate ESM program, being either a macroeconomic adjustment program or a precautionary program.2 This would require the governments to sign up to a reform program likely to include austerity measures. The aim here is to reduce the moral hazard problem.

Although the conditionality has been defined as strict, there are no a priori strict numerical rules for conditionality. It could be set to a vague minimum, requiring the country to wind down crisis-related debt once it is over.

However, the activation of OMT could take time. In order to speed up the process, the ECB could use the second option.

Option 2: Adjustment of the APP

The ECB could interpret the existing rules under the asset purchase program very flexibly. The current asset purchases by the ECB are subject to two main criteria3 1) the capital key, which reflects the respective country’s share in the total population and GDP of the EU 2) and the issuer limit of 33 percent on ECB holdings of debt of a particular country.4 The ECB could defer adherence to these rules to a future date and buy assets with a view to reducing market pressures.

1 For details regarding this scenario, see: https://www.flossbachvonstorch-researchinstitute.com/en/studies/corona-crisis-italys-government-finances-under-pressure/.

2 Loans under macroeconomic adjustment aims to assist ESM members in significant need of financing, facing liquidity problems. Loans are conditional upon the implementation of macroeconomic reform programs, as set by the European Commission. Precautionary credit line is aimed at supporting sound policies and prevent crisis situations in ESM members with sound economic conditions. Further information on the ESM programs are available at: https://www.esm.europa.eu/assistance/lending-toolkit.

3 There are also other eligibility criteria, like the 1 to 30-year maturity restriction, meaning that securities have to have a minimum remaining maturity of 1 year and a maximum remaining maturity of less than 31 years at the time of purchase.

4 For the currently applied capital keys, see www.ecb.europa.eu/ecb/orga/capital/html/index.en.html. Regarding the 33 percent issuer limit, this is applied to safeguard the operating of market forces and to prevent that the ECB would become a dominant creditor of euro area governments. The 33 percent limit is applied to the universe of eligible assets in the 1 to 30-year range of residual maturity.

16.04.2019 - Macroeconomics

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.

Agnieszka Gehringer

Senior Research Analyst

Agnieszka Gehringer joined the institute in 2015. She studied economics at the University of Rome “La Sapienza” and later earned a PhD in economics of complexity at the University of Turin. Since November 2019 she has been a professor of Economics at the Cologne University of Applied Sciences and since July 2016 a lecturer at the University of Göttingen. She has published several articles in academic journals and is an advisor to the EU.

All articles by Agnieszka Gehringer