21.02.2023 - Studies

Higher market interest rates are putting pressure on the premiums companies once paid for acquisitions. Write-downs are imminent.

For many years, all was well at Svenskt Stål AB (SSAB). The Swedish group grew, also through acquisitions. In 2007 and 2014, the steel specialist bought its competitors Ipsco and Rautaruukki. In return, SSAB dropped a few crowns.

This can be seen in the so-called goodwill, an item on the assets side of a company's balance sheet. It shows the premiums that companies once paid on the net assets of the new subsidiaries when they were taken over. In the case of SSAB, this was goodwill of 33.6 billion Swedish kronor last year.

But at the end of the year, only 349 million kroner, or a good one per cent, were still reflected in the balance sheet. The reason: the steel group had written off almost all of these hopeful assets by the end of the year.

Hopeful values, because goodwill is supposed to reflect future synergies and cash flows after acquisitions. However, as stock market experts know, these can only be estimated. And estimates are subject to errors - everyone knows that.

Despite great uncertainty as to whether acquisitions will pay off, companies are allowed to report the full purchase price (net, after deduction of assumed debts) after acquisitions, as permitted by the balance sheet rules. This is the case even if the managers pay high premiums on the net assets of the acquired company. This is a regular occurrence: when Microsoft once acquired Nokia's mobile phone division, with the German Bayer after the takeover of the seed producer Monsanto or with the merger of the industrial gas giants Linde and Praxair.

Goodwill remains on the balance sheet until the book values can no longer be maintained. This would be the case, for example, if a presumed sales price of business units on which the goodwill has been recognised is no longer close to its book value. Or if business prospects deteriorate to such an extent that plans for the expected cash flows have to be more or less significantly scaled back.

However, both occur almost only in theory. Corporate leaders of acquisition-friendly companies regularly avoid admitting that they have bought subsidiaries at too high a price.

There are a few tricks for this. Planning horizons can be extended. And the business units to which the goodwill is allocated can be re-tailored.

These business units are often designed in such a way that no comparable market transaction can be found - where there is no transaction, there is no market price. Exceptions confirm the rule. The fact that business in Russia, for example, is likely to be worth much less in the long term than was assumed a few years ago can hardly be hidden.

But why did SSAB devalue? This is where a third component comes into play, which finance managers should not ignore and gloss over: the current level of market interest rates.

SSAB stated that the "background to the impairment was higher interest rates and a more cautious method of impairment testing". After the massive goodwill impairment, the steel group slipped into the red.

Just like SSAB, AT&T, for example, recently reported losses. Also "due to higher interest rates", the traditional US telephony company wrote off 24.8 billion dollars on its goodwill at the end of the year. In the fourth quarter, AT&T therefore posted an operating loss of 21.1 billion dollars.

But what effect does the current interest rate level have on goodwill? Unlike other assets such as the vehicle fleet or real estate, goodwill is only depreciated irregularly by companies. Although there were plans to reintroduce a regulation on proportional depreciation that was in force until just under 20 years ago,1 these have since disappeared into the drawer again.

Therefore, it is still up to the companies to determine the value of the goodwill. In this context, the managers benefited from the fact that market interest rates had fallen over many years. Cash flows expected in the future were therefore regularly worth more when discounted to the current balance sheet date. This inhibited depreciation.

Now, costs are rising in many cases and customer demand is often declining, which in itself should lead to a weakening of cash flow expectations - at least in individual cases.

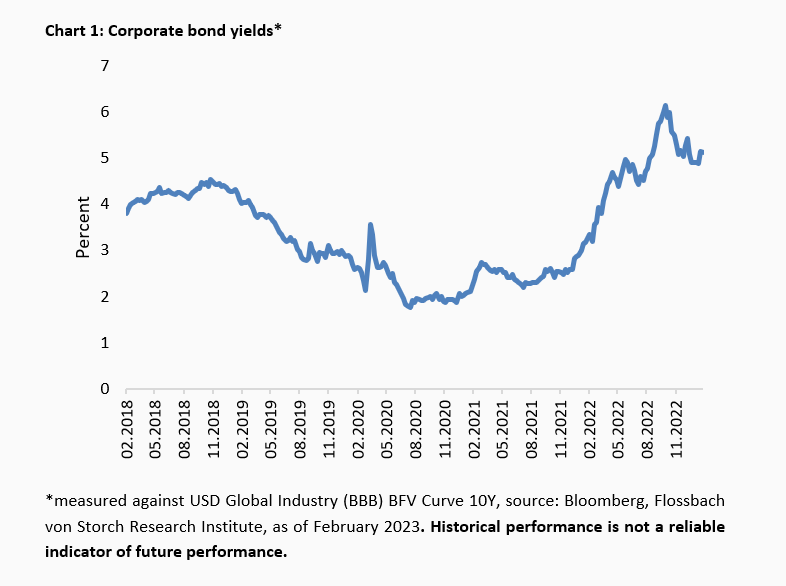

However, the so-called cash value of the cash flow is certainly decreasing in view of the noticeable rise in interest rates. Measured in terms of yields on ten-year, medium-quality corporate bonds, interest rates have more than tripled from their low and have recently remained at a significantly higher plateau (chart 1).

For financial statements prepared in accordance with the International Financial Reporting Standards (IFRS) or US Generally Accepted Accounting Principles (US GAAP) applicable to capital market-oriented groups, this has a significant impact on the level of discount rates.

For example, a cash flow of 100 million euros or dollars expected over five years and flowing for the first time in one year and then once a year thereafter is currently worth a good 485 million at a discount rate of one percent. At an interest rate of five per cent, this current value is reduced to just under 433 million.

The value in use determined from such a cash flow is compared with the book value of a business unit. If the value in use falls below the book value, the goodwill of the business unit must first be written down.

The cash flow expected in the company's planning, discounted at market interest rates, is therefore central to determining the recoverability of the goodwill reported in the balance sheet.

If the book value in the example is 475 million, there is no need for impairment at a discount rate of one per cent, as the value in use is ten million higher. At a discount rate of five per cent, however, the company would have to devalue by 52 million (book value of 485 million minus value in use of 433 million).

The closer the expected cash flows and the value in use based on them have been to the book value in the past, the more the risk of having to write down the value in the event of a higher market interest rate increases. Many companies are likely to pay this price of time now or soon, and could possibly catch one or two inattentive observers on the wrong foot.

Investors are keeping an eye on goodwill, which is often referred to as a "shaky position" - at least for a number of companies. This can be seen in the stock market value. If this is close to or even below the goodwill reported in the balance sheet, the market expects a devaluation. In these cases, investors already distrust the valuation of the company.

It is important to know: When groups write off their businesses, goodwill (if any) always comes first in a cascade of write-offs. Goodwill is therefore a very "soft" item in the long-term assets on the balance sheet.

If the market has already anticipated such a write-down, as indicated by a low stock market value compared to goodwill, then write-downs are no more than a confirmation of the then regularly preceding decline in the share price of the company in question.

But it is also common for investors to be unaware of the risk of goodwill impairment.

For example, on 13 February this year, the American financial services provider Fidelity National Information (FIS) wrote off 17.6 billion dollars in goodwill on its Merchant Solutions division. Apparently this caught investors on the wrong foot: at any rate, the 15 per cent drop in the FIS share price that immediately followed this news speaks for itself.

Especially in the case of high devaluations of goodwill, the CFOs like to argue that these are not cash-effective. This was also the case with FIS in its communication to investors.

This is formally correct. However, the write-offs reduce the shareholders' equity, and thus their proportionate asset value (book value) in their company. Moreover, with a goodwill impairment, companies admit that they have not been careful with their shareholders' money in the past. This is because the former acquisition that led to the goodwill was cash-effective.

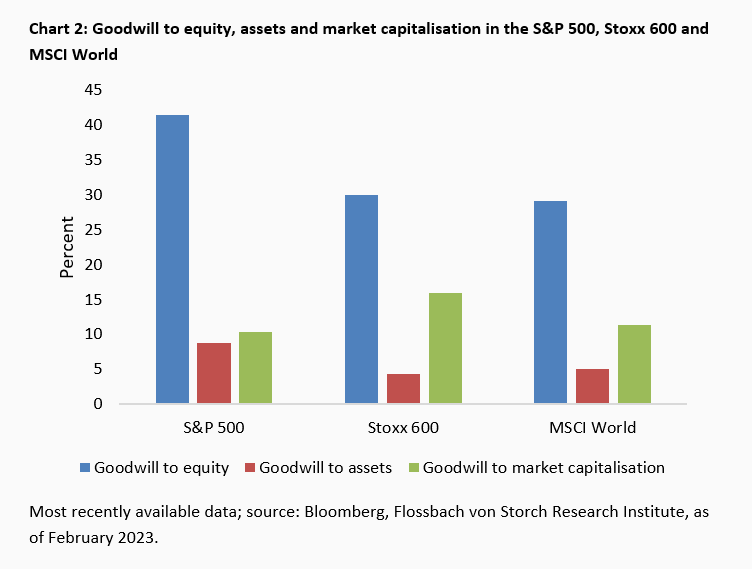

But what role does goodwill play in corporate balance sheets? Measured in terms of all assets, this position does not play an outstanding role on average, but it is not a subordinate one either. In the S&P 500, 8.8 percent of all assets, in the Stoxx 600 4.3 percent and in the MSCI World 5.0 percent were goodwill.

It should be noted that the ratios would be higher if financial service providers such as banks, with their consistently very high assets, were not taken into account. For example, the ratio of goodwill to assets in the S&P 500 would rise to 10.2 percent if the six largest financial groups in the index were excluded.

Overall, goodwill represents 10.3 per cent (S&P 500), 16 per cent (Stoxx 600) and 11.3 per cent (MSCI World) of the market capitalisation of the three indices.

However, it is primarily the relationship to equity that is worth noting, as depreciation has the greatest impact on equity in relative terms.

In the S&P 500, the ratio of goodwill to equity was recently a good 41 percent, in the Stoxx 600 around 30 percent and in the MSCI World a good 29 percent (chart 2).

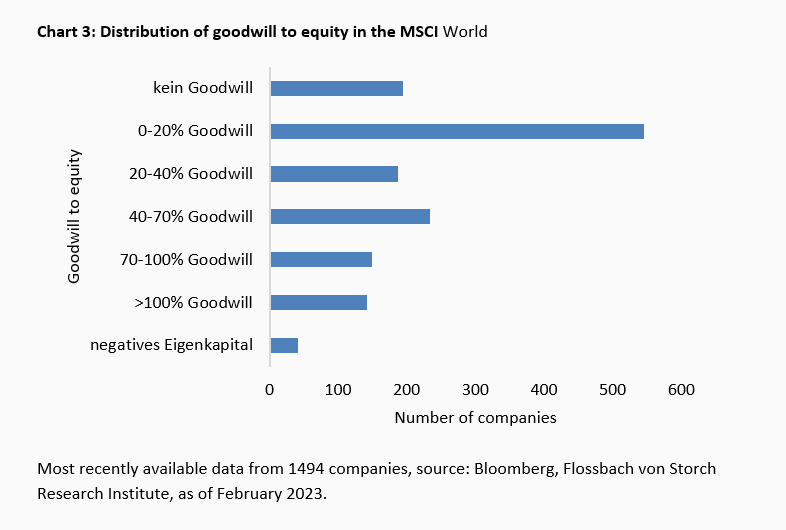

On average, therefore, the ratios to equity are already remarkably high. However, this is not relevant for all companies. For example, almost 200 companies in the MSCI World do not report any goodwill at all.

Goodwill plays a large to very large role in more than one-third of the companies in the World Index, with equity ratios of more than 40 percent to well over 100 percent in some cases (chart 3).

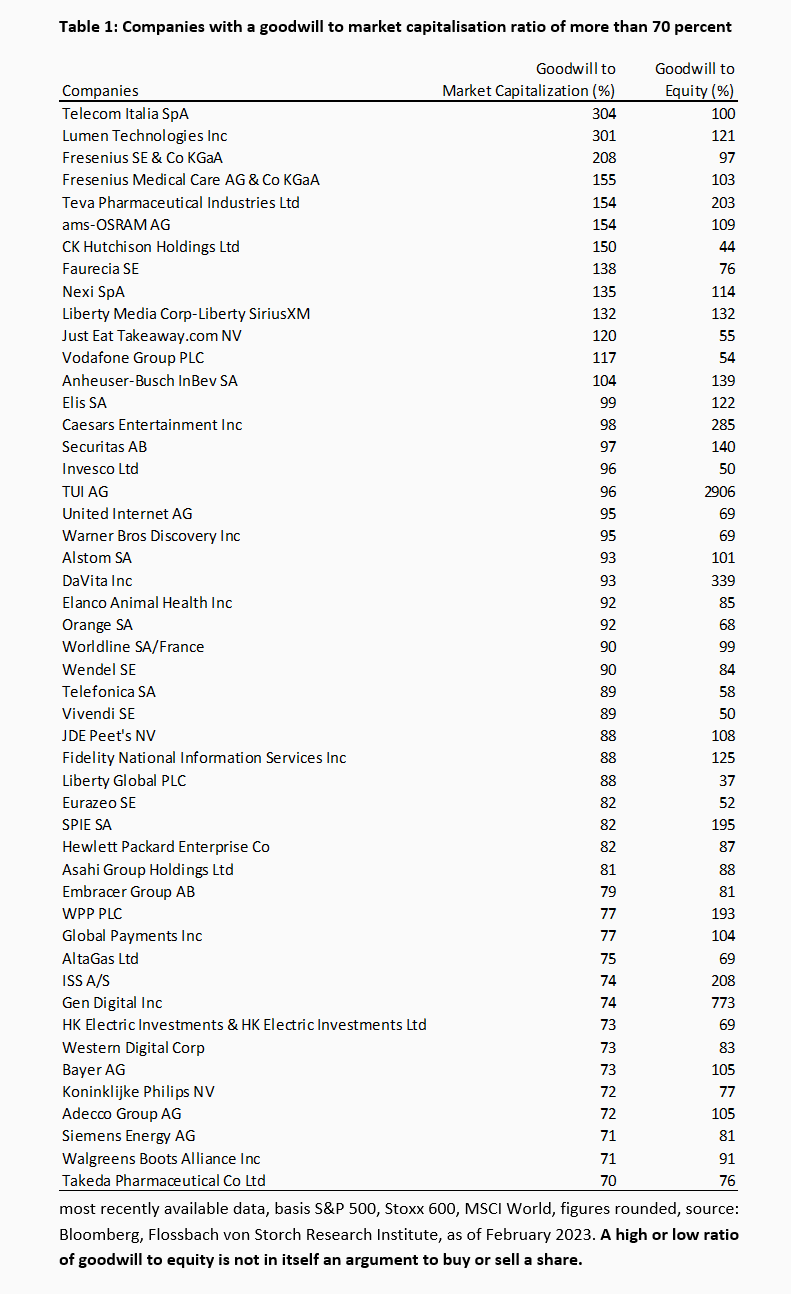

From all three indices, 49 companies can currently be identified that have a goodwill of more than 70 percent measured by their market capitalisation (Table 1).

So investors are sceptical here. A goodwill impairment would therefore not be surprising and the impact on the share price would probably be limited.

The increased interest rate level may have a negative impact on profits and balance sheets of companies reporting goodwill from acquisitions.

In particular, the share price performance of companies for which the market does not yet expect any or only minor devaluations could be negatively affected. Identifying these requires individual analysis.

1 Goodwill - the genie is still in the bottle

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.

Christof Schürmann

Senior Research Analyst

At the Institute since 2022. The graduate in business administration (FH), previously worked as a journalist and deputy head of "Money" at WirtschaftsWoche. The trained banker and book author ("Die Bilanztrickser") taught balance sheet research part-time at the private university BiTS in Iserlohn.

All articles by Christof Schürmann