28.11.2022 - Comments

If Germany had won the international match against Spain yesterday, would the DAX rise today? If you want to believe the sports sentiment theory, the performance of the stock market also depends on the matches in the World Cup. We have tested the hypothesis.

Germany's 2006 World Cup is fondly remembered as the “Sommermärchen” (summer fairy tale): Philipp Lahm's wonderful opening goal against Costa Rica, the euphoria after the late goal in the preliminary round match against Poland and the penalty thriller in the quarterfinals against Argentina, including Jens Lehmann's legendary goal. The streets were filled with celebrations, joy and euphoria.

Major social events that are not directly related to the stock market but enjoy high media attention can have an impact on how individuals feel and ultimately act. The FIFA World Cup is such an event. The victory of a national team in decisive matches can lead to an illusory feeling of success and security as well as overconfidence among the population.1 Investors - institutional or private - can also be drawn into the spell of euphoria and unconsciously let it steer their decisions. This can lead to a short-term, fundamentally unfounded shift in supply and demand on the stock markets, which in turn influences prices and returns.

Not only euphoria but frustration is also conceivable. A defeat in a decisive match can have an impact on the state of mind of a society. The term "sete a um" (Portuguese for 7 to 1) is still a metaphor for a catastrophic event in Brazil today. The lost semifinal at home against the German national team, from the Brazilian point of view, even had political consequences.2

And how did the stock market react to the games? The DAX rose by two percent the following day after the win against Poland and by half a percent after the win against Argentina. So far so good, but after the sporting success against Costa Rica, the DAX fell by one percent and the Brazilian stock index (Bovespa) rose against expectations on the trading day after the sete a. In some cases the theory is true, but in others it is not.

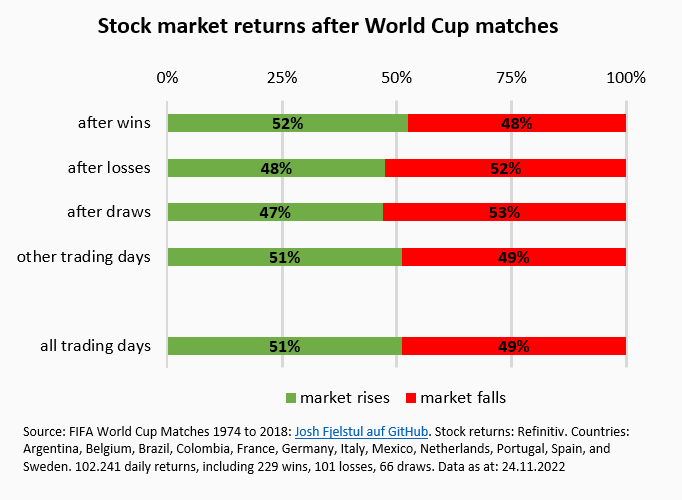

To see if there is any truth behind the theory, we took a close look at the stock markets of 13 soccer-loving countries during the FIFA World Cups from 1974 to 2018.3 Indeed, local stock markets rise somewhat more frequently after national team victories at World Cups than on other trading days. However, the difference in frequency is very small. While local stock markets rose on 52% of days following victories, they also rose on 51% of other trading days.

Price declines after defeats are also found more frequently than on the other trading days. Here, the difference in frequency is 52% to 49%. The result is somewhat more pronounced but not particularly clear.

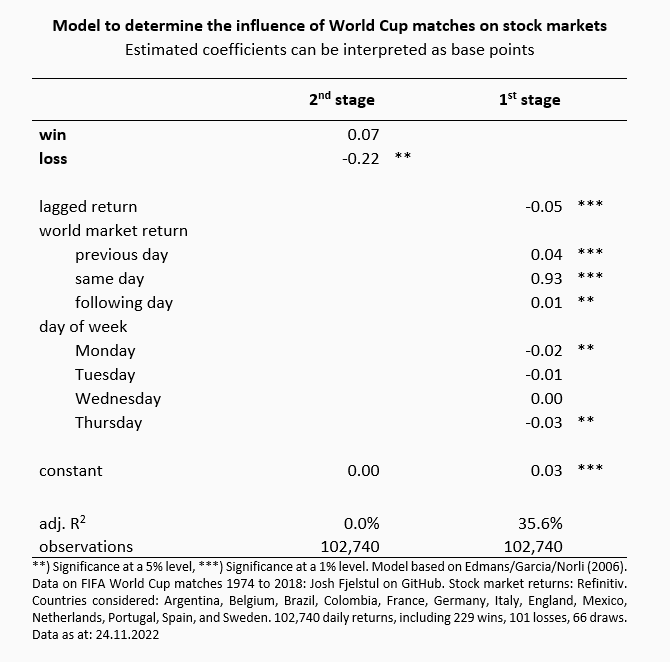

Since capital market returns are subject to various influencing factors that are not accounted for in the above descriptive analysis, we reconstructed the econometric sports sentiment model of Edmans, Garcia, and Norli (2006), which was published in the most prestigious journal in the field of finance (The Journal of Finance).4

In a two-stage estimation model, first the daily returns of the country-specific stock market indices are modeled with various factors. For this purpose, the return of the previous day (due to possible serial autocorrelation), the return of a world market index (of the previous day, the day itself and the following day, as country-specific stock markets may follow or lead the world market) and indicator variables for weekdays (to capture weekday effects, such as the Monday effect5) are used. In a second step, we compare the unexplained portion of daily returns (the so-called residual of a linear regression) on days with World Cup matches with the residual returns on other trading days.

According to the model, the stock market return is higher on the day after a win than on other trading days. However, the estimated difference in returns (7 basis points) is neither statistically nor economically significant. However, the relationship is more pronounced in the case of defeats. Stock market returns in countries that lost World Cup matches are 22 basis points below the other average. The estimated effect is both statistically significant and economically significant in its magnitude.

Although the econometric model strikes on a broad data set, if it is applied only to individual national teams or to individual World Cup tournaments, the evidence is quite thin. For example, if we reduce the data set to the DAX and the World Cup matches of the German national team, no correlation can be found. Even during the summer fairy tale, there is a lack of significance. Distinguishing group games from knockout games also makes no difference. If one focuses on Brazil in the belief that the emotions of society there are more strongly linked to the successes or failures of the Seleção, one is also disappointed by the development of the stock market.

There are many events that coincidentally follow days with rising or falling markets. This is the breeding ground for creative theories, which are found thanks to the wide availability of data and technical analysis tools - even if there is no causal relationship. Currently, there is more discussion about FIFA and Qatar than about the sporting performance of the national teams. Therefore, it is even more unlikely that the stock market will react to the sporting results at this tournament. The substitution of Niclas Füllkrug therefore has nothing to do with today's performance of the DAX.

1 I.e. Barberis/Shleifer/Vishny (1998): „A Model of Investor Sentiment“, in Journal of Financial Economics 49/3, Daniel/Hirshleifer/Subrahmanyman (1998): „Investor Psychology and Security Market Under- and Overreactions“, in The Journal of Finance 53/6, Baker/Wurgler (2006): „Investor Sentiment in the Stock Market“, in The Journal of Economic Perspectives 21/2.

2 Cp.: Fallay (2014): „Saved by the Goalkeeper: Soccer and Elections“ in Harvard International Review 36/1.

3 Source of data for FIFA World Cup matches: Josh Fjelstul on GitHub. Source of data for stock market returns: Refinitiv. Countries: Argentina, Belgium, Brazil, Colombia, France, Germany, Italy, Mexico, Netherlands, Portugal, Spain, and Sweden.

4 Edmans/Garcia/Norli (2006): „Sports Sentiment and Stock Returns“ in The Journal of Finance 62/4.

5 C.p. Wang/Yuming/Erickson (1997): „A New Look at the Monday Effect“ in The Journal of Finance 52/5.

22.11.2022 - Society & Finance

by Sven Ebert

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.