04.06.2020 - Comments

The corona crisis has caused new distress in the European Monetary Union. Italy and other southern European countries are struggling desperately for financial assistance from the north, in particular from Germany. But this will not address the main problem of the euro area: Real economic divergence, which will be aggravated further by the measures to fight the Corona crisis. A new approach is needed to avert a chaotic collapse of EMU and to protect the European Union.

Lessons from the German monetary union

The Germans have their experience with a much less than optimal monetary union. On 18 May 1990 the West and East German finance ministers signed a treaty establishing the German Monetary, Economic and Social Union, which entered into force on 1 July 1990 and established the Deutsche Mark as official legal tender in the German Democratic Republic. This sounds like a story from the world before yesterday, but it provides important lessons for the European Monetary Union.

In 1990, the east German economy was expected to adjust rapidly and to catch up quickly with its west German counterpart. Chancellor Helmut Kohl had promised “blooming landscapes” within four years. This proved to be wishful thinking. Uncompetitive and unable to devalue its exchange rate, the east German economy tanked and unemployment spiked. Until today, productivity, income and wealth levels have not caught up by far (Schnabl and Sepp 2019).

Only nine years later, eleven European countries with different economic structures entered the European Monetary Union, with rapid convergence expected. Again, this proved to be wishful thinking. After a consumption boom in the south of the European Monetary Union (EMU) from 2001 to 2007, the southern European economies, among them especially Italy have been suffering from a persistent lack of competitiveness since 2008 (Schnabl 2019). Now, the pandemic aggravates the problem. As the southern economies rely more heavily on tourism and have a larger share of small and medium-sized enterprises than their northern neighbors, they are likely to be hit harder, with their competitiveness declining even further.

When instead of blooming landscapes an economic desert emerged in eastern Germany, the government applied huge volumes of fertilizer. To prop up the economy and people’s incomes they transferred approximately 1.5 billion euros of taxpayer money in the course of twenty-three years after unification to the East. This amounted to more than twelve times the GDP of the East German economy in 1991. Nevertheless, unemployment kept rising, reaching a peak of 20.6 percent in 2005. Until today, 1.5 million mostly young and educated people, equivalent to 10 percent of the total population, left the territory of the former German Democratic Republic. This eventually reduced unemployment, but it left the economy in Eastern Germany emaciated.

Similarly, since the euro crisis southern European economies were propped up with large credits from newly created euro rescue funds and have received continuous funding support from the European Central Bank. But they have failed to grow. At the end of 2019, real GDP was down 5 percent in Italy and 23 percent in Greece from its level of the first quarter of 2008. Many young people have left southern Europe and will continue to do so. Now, European politicians are designing new gigantic rescue packages. But as the experience of eastern Germany over the last thirty years and that of southern Europe of the last decade shows, these packages will most likely fail to induce growth and create employment.

Relative price changes needed

As every IMF economist with a little experience can tell, income support alone will not restore economic growth when economic structures are not adapted to new circumstances. What is required are relative price changes, either via nominal exchange rate adjustment or adjustment of wages and prices (Mundell 1961). For European Monetary Union to persist the southern euro area economies need a reduction of their relative prices, which would require wage repression in the south and/or wage increases in north.1

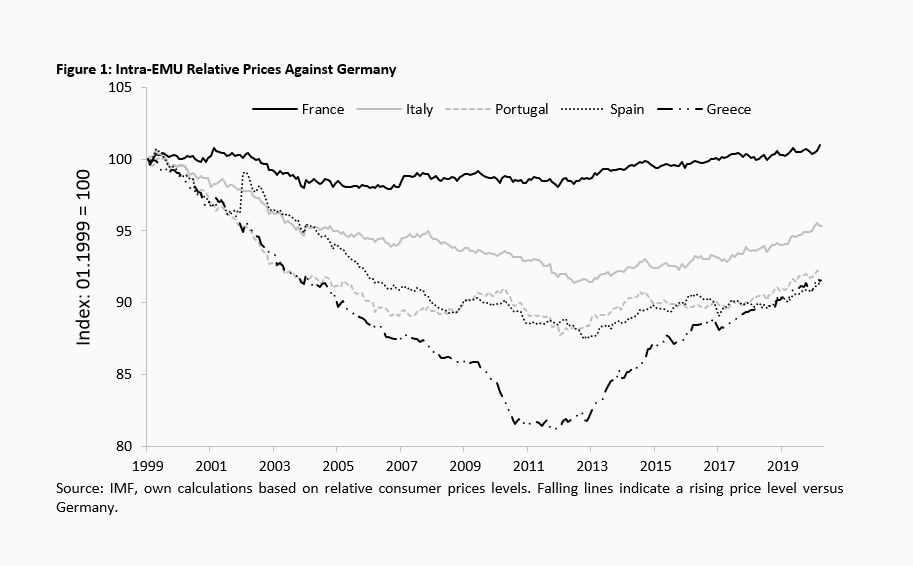

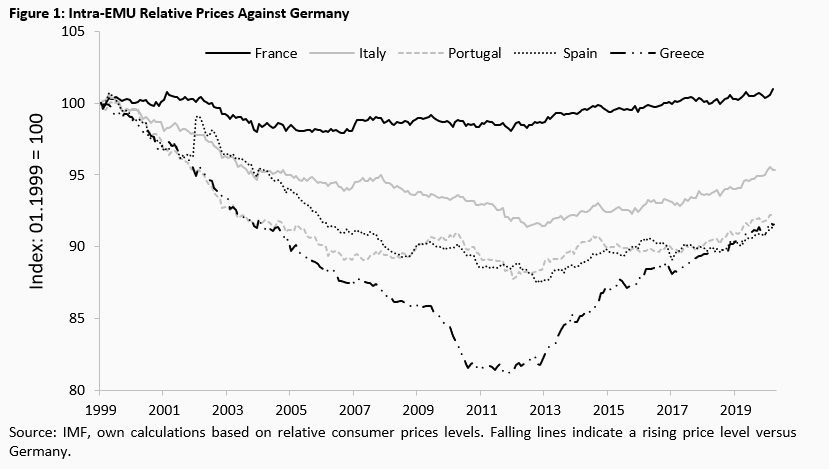

Since euro introduction the relative prices of the southern euro area countries have increased against Germany instead of decreased (Figure 1). As a result, the southern euro area countries have lost competitiveness. The resulting external deficits could be easily financed with large debt capital inflows. Even more credit and transfers in the wake of the Corona crisis may soften the pain in the short run, but they will only postpone the necessary economic adjustment and increase the adjustment need further. Dissolution of EMU would be a remedy to achieve a quick adjustment of relative prices. But an outright exit of the southern European countries from the Union would cause substantial turmoil in financial markets and cause a big political crisis. Hence, unconventional measures to avoid the breakup of the euro are needed.

Parallel currencies in the south

The relative price could be reduced by launching parallel currencies in the southern euro area countries, which could take the form of nonredeemable government bonds without interest and in small denominations. In Italy, such instruments have been proposed and dubbed “Mini-Bots” (derived from “Buoni del Tresoro”, the name for Italian government bonds, Mayer 2019a). When the government funds part of its expenditures by issuing these Mini Bots and accepts them as payment for a part of tax liabilities - based on the share they have in taxpayers’ incomes - these instruments could become a parallel currency for domestic use. Mini Bots could be issued electronically, like normal government bonds (“Buoni del Tesoro Poliennale” or “BTPs”), or they could be issued as paper money.

Since the parallel currency most likely would be deemed a less attractive store of value, the Mini Bots would depreciate against the euro, inducing a decline in euro prices and a reduction of Italy’s relative prices vis-à-vis its euro area trading partners. To follow this argument, assume that the government pays a part of social transfers and salaries to its employees in Mini Bots. As sellers of goods and services to these groups would now receive part of their sales revenue in Mini Bots as well, they would also pay part of the wages to their employees and of the costs of their inputs in this currency. Profit margins of recipients of euros from sales abroad could increase when costs for domestic inputs have declined, but many of them would probably opt for cutting their euro prices to raise their market share. Thus, a decline of the prices of Italian goods relative to those of its euro area trading partners would follow.

As long as there is slack in the economy, inflation of goods priced in the parallel currency for domestic use would remain low, allowing the nominal depreciation of the Mini Bots to induce a real depreciation and to exert downward pressure on goods priced in euro for exports. Foreign demand for Italian goods would rise, in particular for services in the tourism sector, which constitutes a substantial share of economic activity in the Italian economy.

While economic growth and employment would benefit, the Italian government would receive less taxes in euros and may no longer be able to service its euro denominated debt. Hence, the introduction of the parallel currency would need to go along with debt reduction. Restructuring would be painful. But a policy combining debt reduction along the lines of the 1933 Chicago Plan with turning the euro into a digital central bank currency could achieve the same effect at much lower costs.2

Parallel currencies in the north

Alternatively, the German Bundesbank could begin to withdraw from the ECB’s asset purchasing programs. The path to gradual withdrawal was opened by a ruling of the German Constitutional Court on May 5, 2020. The Court found good reasons for a breach of mandate by the ECB’s purchases of public sector bonds, and it gave the ECB three months to explain itself. Should the explanation be unsatisfactory, the Bundesbank would be banned from participating in the public sector purchase program PSPP. The ban could well be extended to the ECB’s Pandemic Emergency Purchase Program PEPP, which by the Court’s standards is even closer to monetary financing of government debt than PSPP.

The withdrawal of the Bundesbank from these programs could lead to capital flight to Germany in anticipation of a break-up of the euro. To fend off a bank run from southern Europe into Germany, the Bundesbank would have to close the existing Target2 interbank payment system and accept euro payments from other member countries only if backed by gold or foreign exchange as collateral. If southern European central banks would lack the collateral needed to make transfers, euro payments could no longer be made from southern Europe to Germany.

Target2 eliminates the restrictions set in the Exchange Rate Mechanism of the European Monetary System (ERM), which preceded European Monetary Union (1979-1998).3 In the ERM, currencies were tied together with fixed exchange rates, around which they could fluctuate within a limited band. Credit facilities were strictly limited in size and time so that countries experiencing balance of payment deficits had eventually to devalue their currencies against the Deutsche Mark, which served as an anchor for the other currencies. Target2 now allows the unlimited funding of balance of payments deficits, presently at zero costs, since the interest rate on liabilities within the system is set at the marginal refinancing rate of the ECB (which is zero) (Sinn and Wollmershäuser 2012).

Balance of payment imbalances have already increased substantially since the euro crisis of 2010-12, with Italy’s liabilities within the Target-system reaching € 513 billion and Germany’s claims € 919 billion (April 2020). If Germany ties the funding of balance of payments imbalances in the future to collateral, which southern European countries do not have, payments can only continue via the foreign exchange market, where exchange rates are allowed to adjust freely. To this end, Germany would have to introduce a new, freely floating currency. Let’s call it the New Mark. The New Mark could appreciate against the euro, allowing a change in the relative prices between the two different regions.

If Germany would remain in the EMU and use the New Mark as a parallel currency, a financially disruptive and politically divisive breakup of the euro area could be avoided. Payments in euros could still be made between southern Europe and Germany. If inflows would match outflows, there would be no additional demand for the New Mark. The exchange rate between the euro and the New Mark would remain unchanged. But if payment flows from southern Europe to Germany were larger than from Germany to southern Europe, the difference would have to be made by exchanging euros against New Marks. The New Mark would appreciate against the euro.4

Given persistent appreciation expectations, the New Mark would probably replace the euro as a store of value in Germany, but payments within Germany and abroad could still be made in euros. The appreciation of the New Mark would boost German demand for foreign products priced in euros, the competitiveness of southern Europe would increase, and payment flows from Germany to southern Europe would be generated. Southern European countries would have an incentive to increase the competitiveness of their economies to avoid a too large loss of income. Thus, the pressure for structural adjustment, which existed before EMU but was reduced in EMU by the ability to cheaply finance internal and external deficits, would be restored. If southern euro area countries managed to run balance of payments surpluses, they could even eliminate the need for New Marks and allow Germany to run down its big Target2 surpluses.

As before, the entire group of EMU member countries could reduce their large government debt by placing part of their government bonds permanently on the ECB’s balance sheet as a 100% cover for the euro. They could establish safeguards for a further monetization of debt in order to support confidence in the euro.

All this may sound utopian. But if policy makers continue their present course, southern European economies will shrink further, until populist politicians will eventually take these countries out of monetary union, destroying the euro and with it the European Union. To avert this, politicians will need to think out of the box.

References:

Albers, Willi et al. (ed.) (1980): Handwörterbuch der Wirtschaftswissenschaft, Gustav Fischer et al., Stuttgart.

Kenen, Peter (1969): The Theory of Optimum Currency Areas: An Eclectic View, in Mundell, Robert / Swoboda, Alexander (eds), Monetary Problems of the International Economy, Chicago University Press, Chicago, 41-60.

Kenen, Peter (2003): Five years of the ECB, CentrePiece Summer 2003, 31-36.

Mayer, Thomas (2019a): Italiens Mini Bots, Frankfurter Allgemeine Zeitung, 15.6.2019.

Mayer, Thomas (2019b): A Digital Euro to Save EMU. VOX CEPR Policy Portal, 6.11.2019.

Mundell, Robert(1961): Optimum Currency Areas. American Economic Review 51, 657-665.

Schnabl, Gunther 2019: The Failure of ECB Monetary Policy from a Mises/Hayek Perspective. In Godart-van der Kroon, Annette / Vonlanthen, Patrik (eds.): Banking and Monetary Policy from the Perspective of Austrian Economics, Springer, Berlin 2018, 127-152.

Schnabl, Gunther / Sepp, Tim (2019): 30 Jahre nach dem Mauerfall: Ursachen für Konvergenz und Divergenz zwischen Ost- und Westdeutschland. Universität Leipzig Wirtschaftswissenschaftliche Fakultät Working Paper 162.

Sinn, Hans-Werner / Wollmerhäuser, Timo (2012): Target Loans, Current Account Balances and Capital Flows: the ECB’s Rescue Facility. International Tax and Public Finance, 19, 468-508.

Ungerer, Horst / Hauvonen, Jouko / Lopez-Claros, Augusto / Mayer, Thomas (1990): The European Monetary System: Developments and Perspectives. IMF Occasional Paper No. 73, November 1990.

1 Kenen (1969, 2003) suggested that a common fiscal policy could compensate for the imperfect fit of a one-size-fits-all monetary policy in a currency union as far as stabilization policy is concerned. But historical experience from Germany and Italy suggests that fiscal policy cannot compensate for lasting structural differences.

2 See Mayer (2019b). A large part of euro area government debt could be taken out of the market by placing it permanently on the balance sheet of the European Central Bank as a cover pool for existing paper money and a new central bank digital currency. Following the conversion of existing bank money into central bank money through purchases of outstanding government bonds by the ECB, the initial central bank money stock could be increased over time according to a fixed rule. Both the creation of the digital euro money stock and the rule for its increase could be enshrined in a smart contract that is embodied in the digital euro.

3 Ungerer at al. (1990).

4 A similar system of matching payments among European countries existed in 1950-1958 in the form of the so-called European Payments Union (Albers et al., 1980). When payment imbalances exceeded certain thresholds and the embedded credit system reached its limits, they had to be made in US Dollars or in Gold.

18.05.2020 - Macroeconomics

by Thomas Mayer

17.04.2020 - Macroeconomics

by Thomas Mayer

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch SE. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch SE remains solely with Flossbach von Storch SE. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch SE.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch SE.

© 2024 Flossbach von Storch. All rights reserved.