04.09.2020 - Studies

![[Translate to English:]](https://www.flossbachvonstorch-researchinstitute.com//fileadmin/_processed_/6/9/csm_Europasterne_250x215_6fc1119e97.jpg)

*In cooperation with Dr. Jörg König (Stiftung Marktwirtschaft, Head of Europe, energy, competition, growth and development policy, support of the Kronberger Kreises) and Prof. Dr. Renate Ohr (Professor (emeritus) of Economics, esp. Economic Policy at the University of Göttingen)

The European debt crisis halted the economic integration within the European Union and – even more so – within the euro area.

Given the deep structural differences across the EU, the COVID-19 pandemic is likely to reinforce this disintegration tendency. This makes the union more and more vulnerable to shocks, with the costs of keeping the union together increasingly burdensome for the taxpayers in the creditor countries, casting doubts about the future of the block.

The European Union (EU) aims to create an integrated economic community where national borders do not impede trade or the movement of production factors. A functioning single market may contribute to economic growth and prosperity by stimulating competition, improving efficiency, raising quality, and lowering prices. Integrated markets can also enhance the shock absorption capacity of the union, i.e. through better access to international capital and credit markets.

Moreover, economic integration is a vital precondition for a union with fixed exchange rates and common monetary policy. This is what the standard theory of the Optimum Currency Area (OCA) implies: a currency area is optimal, if a sufficient degree of real economic integration between regions – in terms of integrated goods, services and factor markets – is achieved.1 Otherwise the loss of economic stability weighs more than the gain in monetary efficiency from participating in the fixed exchange rate system.2

In fact, the European Monetary Union (EMU) is far from fulfilling the initial economic expectations of many member states. Productivity growth has slowed down, leaving members like Italy with a GDP per capita as low as in 1999. The expected process of real economic convergence turned to economic divergence, and particularly the performance of Southern Europe has not met expectations.3 Also, EMU is far from being the promised “stability union”, with excessive public debt accumulation in many (Southern) member states.

In what follows, this paper shows a data-based evidence of the ongoing real disintegration within the E(M)U. It then describes the mainstream strategies to “complete” the union and discusses the underlying drawbacks.

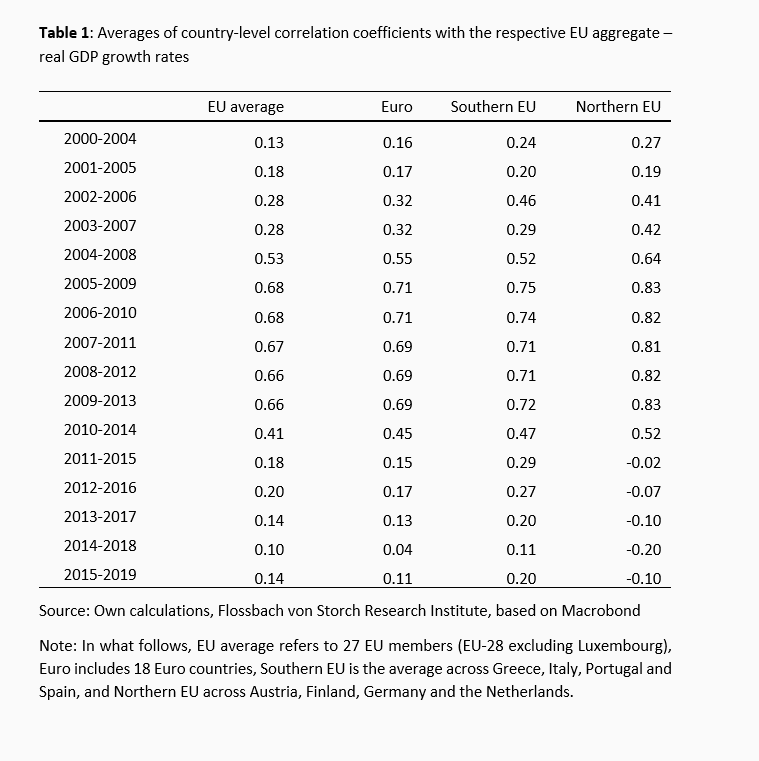

Our measurement of the degree of economic integration refers to the “EU symmetry” dimension of broader EU integration, as measured in the EU-Index by König and Ohr (2013). Following their approach, we calculate pairwise correlations between the country’s value of each indicator (as explained below) and its population weighted average value of the remaining EU members. The pairwise correlations are calculated on a yearly basis as a moving average over a period of 20 quarters.4 The current data availability permits us to analyse the correlation coefficients between 2004 and 2019 (with raw data starting in the first quarter of 2000).

We calculate pairwise correlations for a set of nine indicators. Among them, the headline and core inflation, as well as the 10-year government bond yield are used to assess nominal integration. The remaining indicators, i.e. real GDP growth, change in (youth) unemployment rate, in labor productivity, in industrial production, and the balance of government budget as a percentage of GDP, are aimed at measuring the real integration process.5

In the tables below, we show averages of country-level correlation coefficients calculated for important country’s aggregates, namely, EU, Euro, Southern EU and Northern EU. Where suitable we comment on remarkable single country developments.6

In interpreting the numbers, beyond looking at the absolute values of the correlation coefficients, it is also important to focus on the underlying tendency of the coefficients over time. Regarding the levels, the comparison of the coefficients between country groups or single countries should be insightful to detect differences in the advancement of economic integration. In general terms, a country is integrated with the rest of the union for sufficiently high values of correlation coefficients. For low or negative coefficients, disintegration is the case. The analysis of the tendency of coefficients over time is useful in tracking the direction of the process. We speak about an ongoing integration process, provided that the correlation coefficients tend to increase, as this implies that the underlying developments between the country and the corresponding EU average are becoming more symmetric. The more symmetric the co-movement of business cycles, the more suitable the common monetary policy for all member states. To the contrary, disintegration takes place if correlation coefficients fall over time.

In terms of real GDP growth, EU countries became more symmetric in the decade before the 2008 crisis, but in terms of levels the process has never reached a meaningful degree of integration. Moreover, after the European sovereign debt crisis the process has reversed or at least has not deepened compared with the pre-crisis levels (Tab. 1). These dynamics were widespread, with real disintegration taking place both especially in Southern and – even more – in Northern EU members.

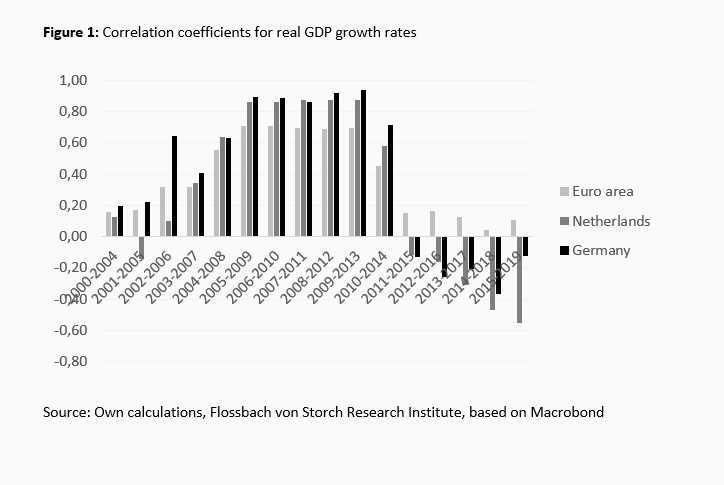

At the single-country level, the most drastic developments occurred in the Netherlands and in Germany. Their above-average alignment with the euro area average in the period before the European sovereign debt crisis turned into a strong above-average divergence thereafter, with increasingly negative correlation coefficients (Fig. 1).

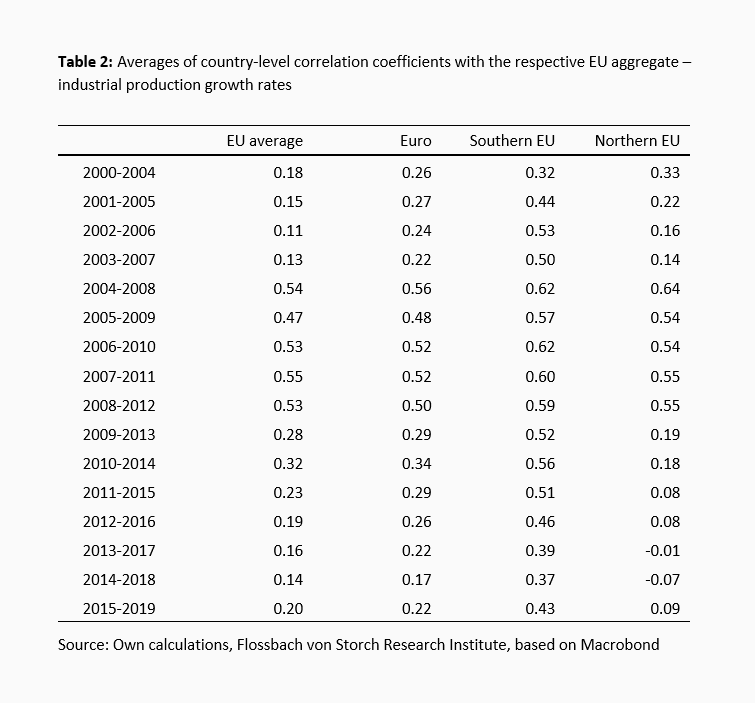

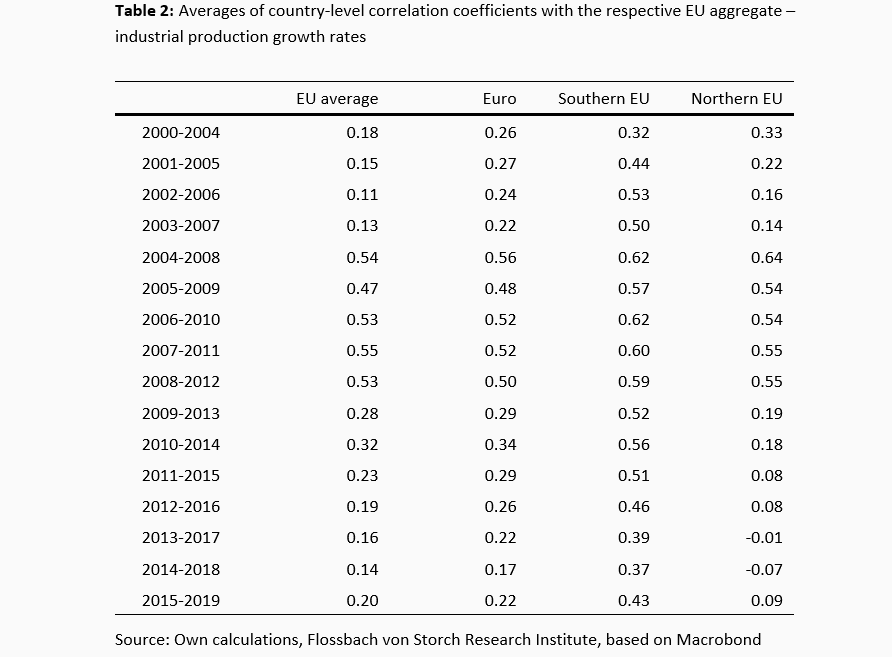

A similar disintegration took place in the field of industrial production (Tab. 2), with the difference that industrial production dynamics across the EU have never reached the degree of alignment observed for real GDP growth. This finding is insofar meaningful that it provides evidence of the impracticability of the endogeneity hypothesis of the integration process, according to which the progressive alignment of the internal market and of productive structures would allow the union to generate internal forces making it increasingly integrated.

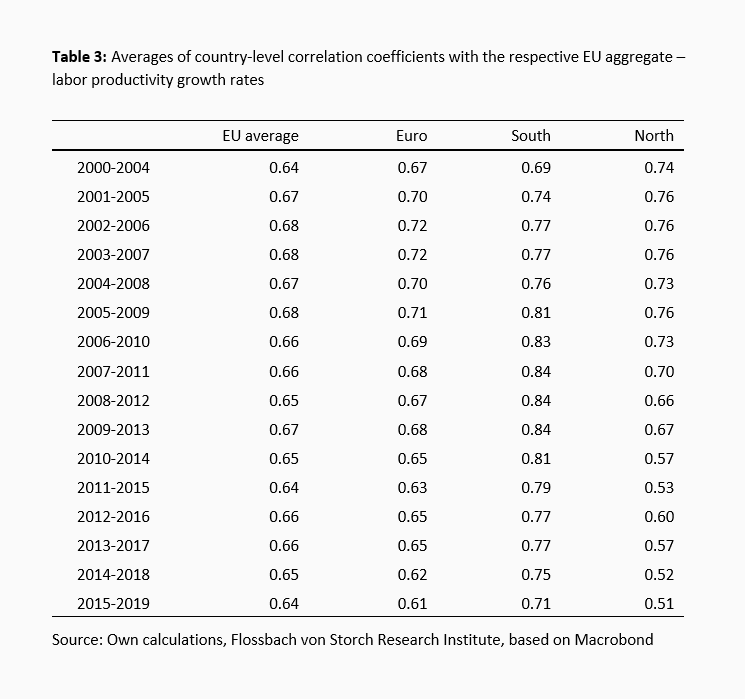

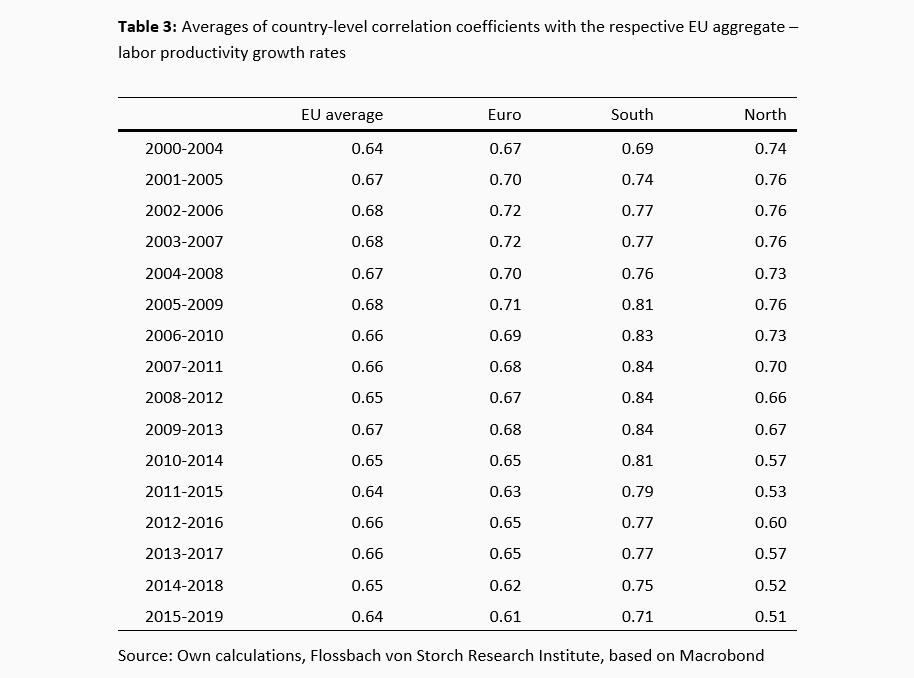

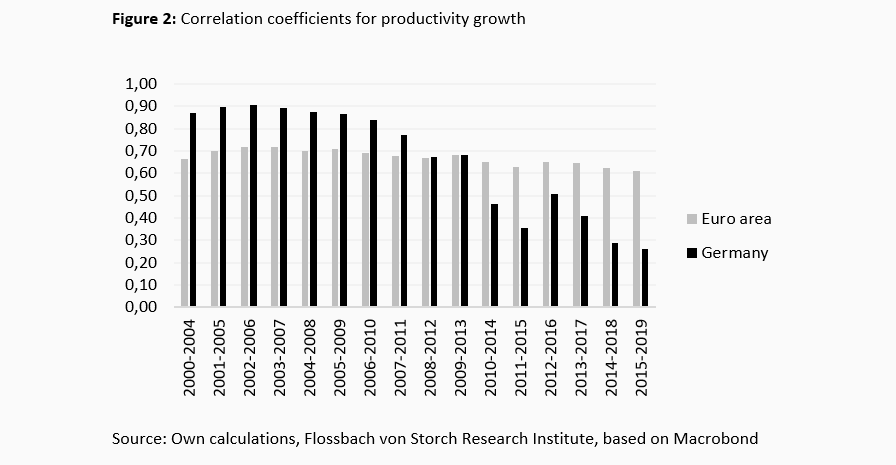

The developments described so far are at least partly reflected in the stagnating or even progressively weakening integration of labor productivity growth (Tab.3). Germany offers again a negative example here: the country’s correlation coefficient with the EU average was the highest (0.91) in 2006 and has declined since to a low of 0.26 in 2019 (Fig. 2).7

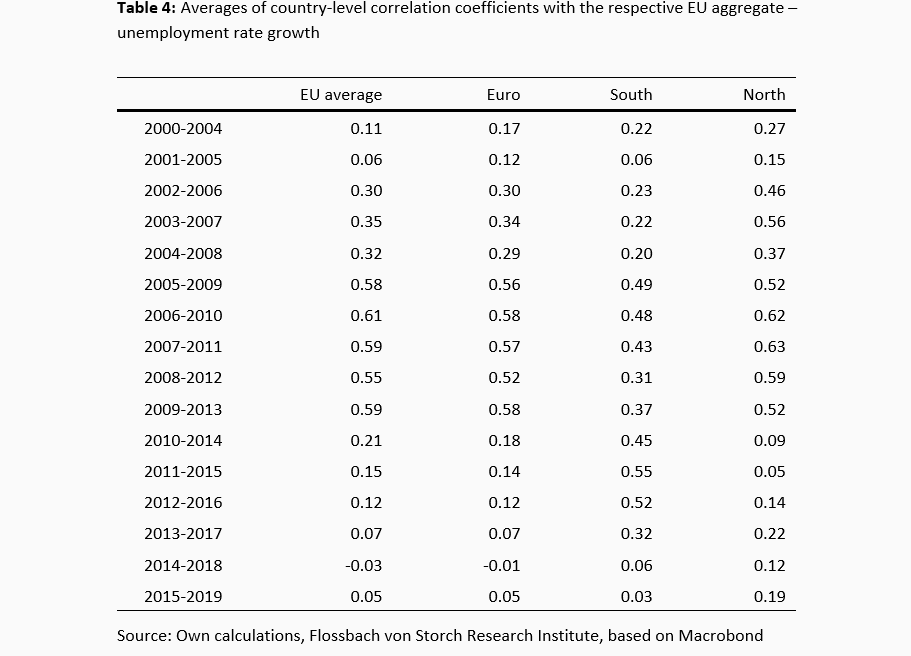

Real disintegration took also place in the labor markets (Tab. 4 and 5). The levels of correlation coefficients prove that the labor markets were barely integrated with acute disintegration taking place especially within the euro area. These developments could be seen as a direct consequence of the previously described phenomena. Behind the diverging growth fortunes, there was a weak economic performance of Southern EU members relative to the rest of the EU. This in turn contributed to the deterioration in structural and technological characteristics in the South, which eventually led to a substantial increase in unemployment rates in the wake of the Great Financial Crisis and later in the events of the European sovereign debt crisis.8

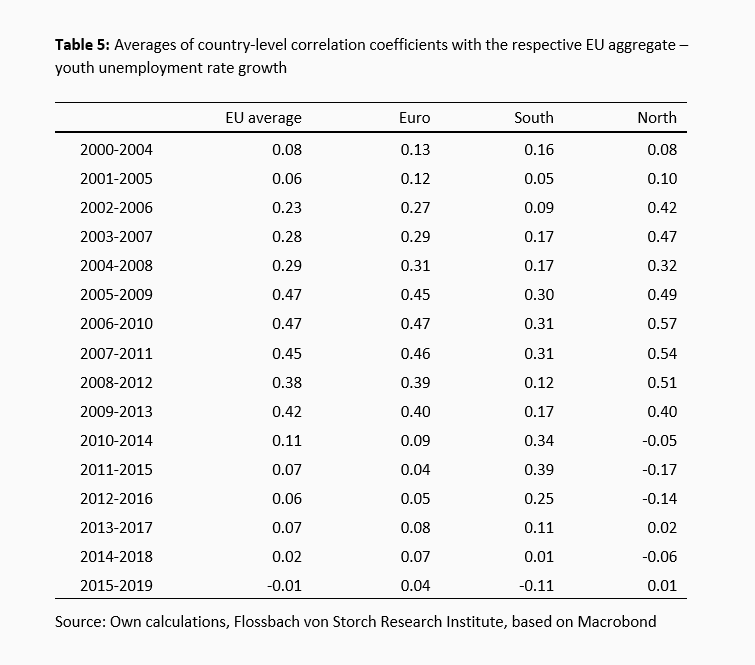

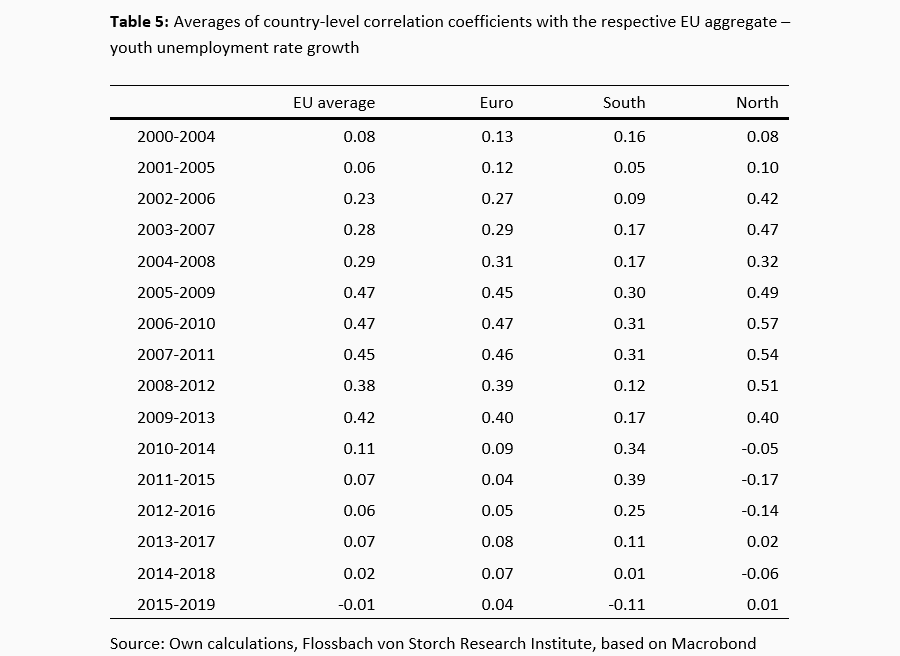

The labor-market disconnect between EU members is reflected with particular severity in youth unemployment rate dynamics (Tab. 5). Correlation coefficients declined remarkably after the 2008 crisis and are extremely low or even negative (Euro).

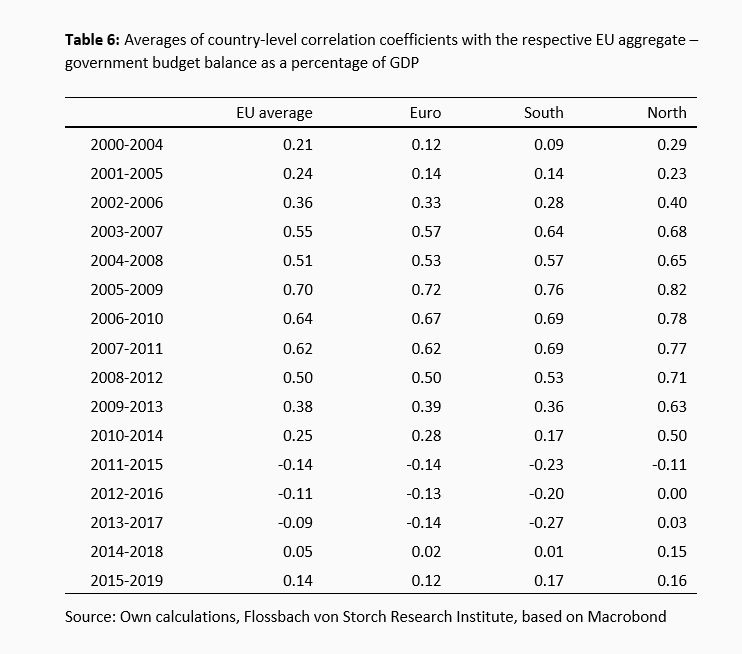

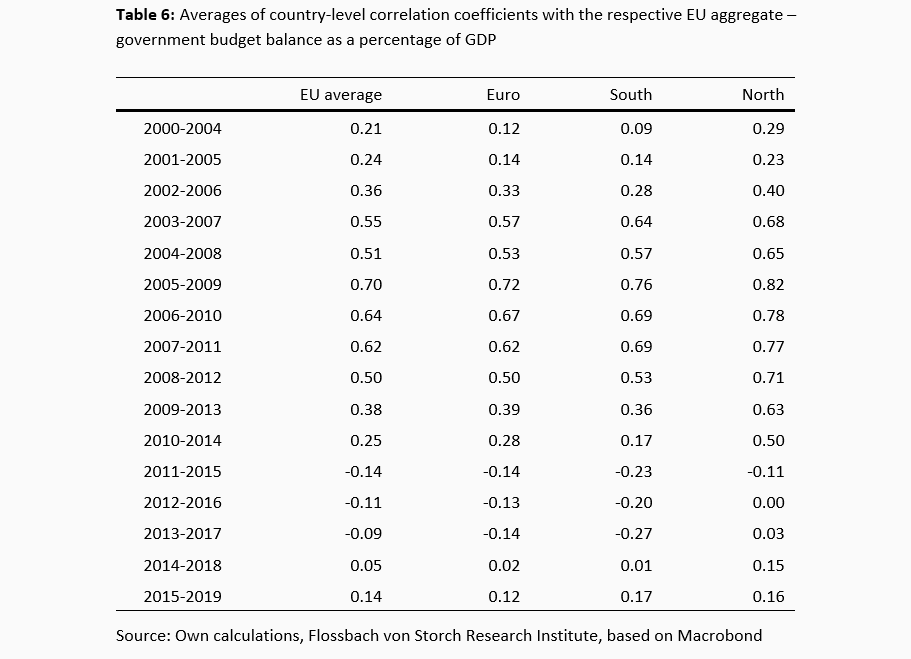

The growing real disintegration observed in the post-debt-crisis era eventually led to differing developments in government finances within the union, with permanently high deficits in the South and improving government balances in the North. This divergence is reflected in the falling correlation coefficients for the government budget balances over that period (Tab. 6).

Based on this last piece of evidence, a valuable prediction with important implications for the future can be made. Given the accumulated real asymmetries so far and a non-negligible likelihood that the shock brought about with the COVID-19 pandemic could magnify centrifugal forces set in motion within the E(M)U, the exigence of fiscal support in more vulnerable economies is most likely to increase in the years to come. Without more help through fiscal transfers, the rising disintegration could unleash political forces bringing the union to a collapse.

There is some evidence that nominal developments became increasingly synchronized within the EU. However, given that the union disintegrated in real terms, it follows that such nominal integration was not driven by purely economic forces, but most likely by monetary policy efforts by the ECB to counteract centrifugal real economic forces.

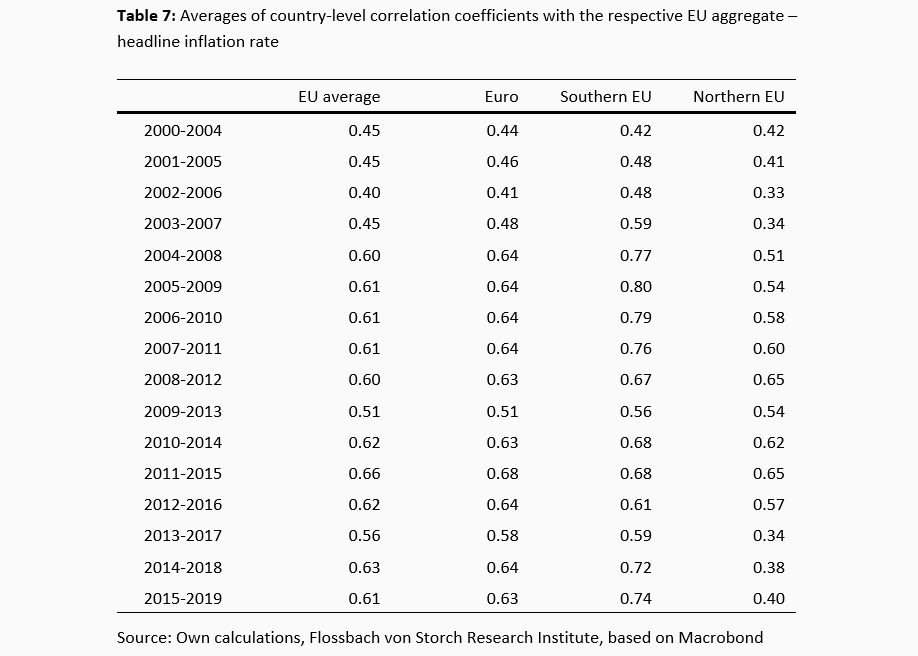

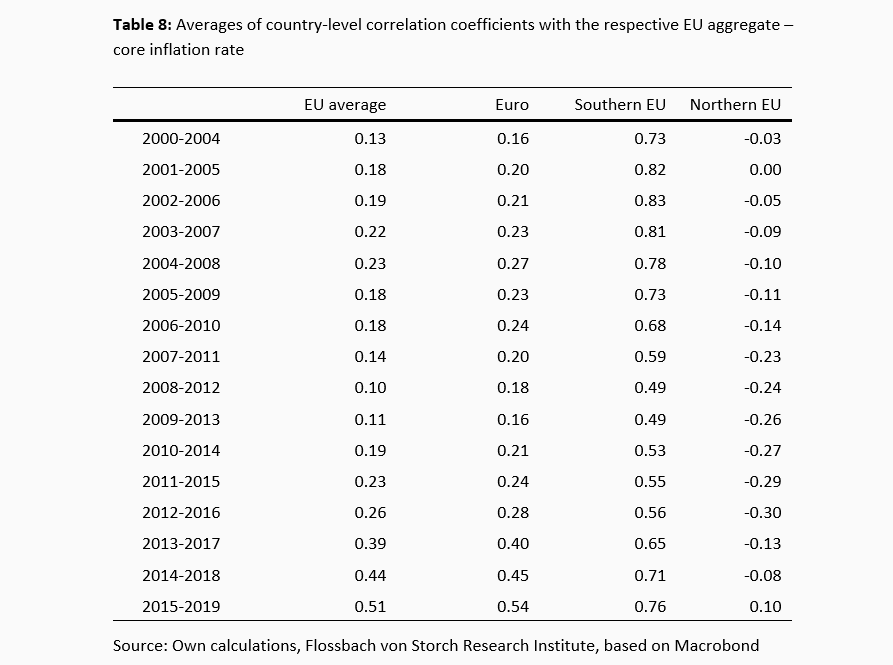

Between 2004 and 2019, the correlation coefficients of both headline and especially core inflation (excluding thus energy and food prices, characterized by volatile price developments) increased for the EU as a whole and the euro area (Tab. 7 and 8). Also Southern EU countries moved closer to the rest of the EU. Instead, Northern EU countries are a remarkable exception here – although the moderate alignment of their headline inflation with the EU average increased initially, it declined again after the break-out of the European sovereign debt crisis. The general disconnection tendency in the core inflation observed in Northern EU countries was further reinforced over the years.

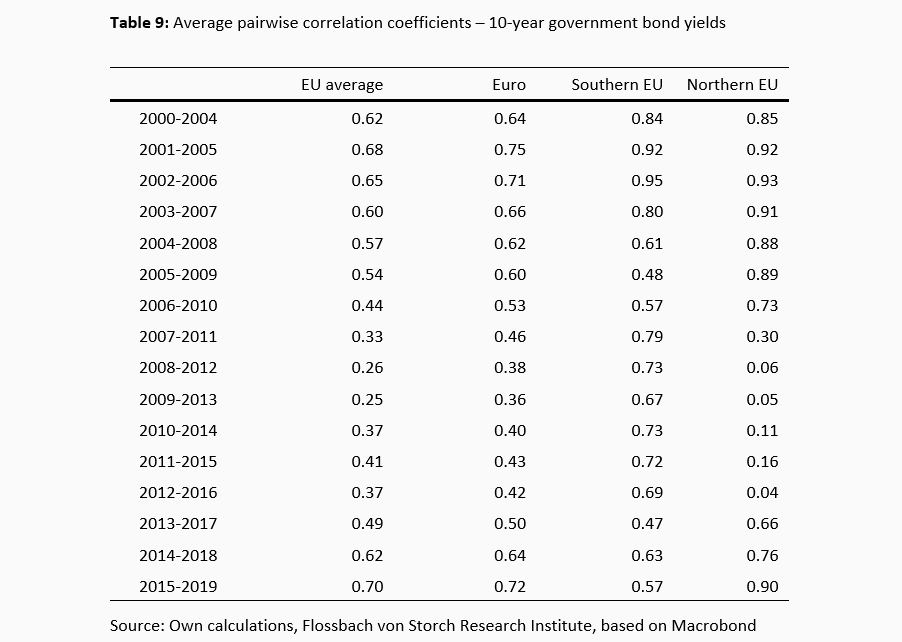

The political commitment of the ECB to save the euro – and implicitly also the EU – at any price is reflected in the rising correlation coefficients for 10-year government bond yields (Tab. 9). Although the ECB’s extensive interventions – especially since the European sovereign debt crisis – might have reduced the financial volatility within the system, they have not removed the fundamental weaknesses in real economic conditions. Moreover, due to the strong moral hazard incentives indigenous in most of its unconventional instruments, it might have even aggravated such weaknesses. The rapidly increasing indebtedness across the euro area is a strong indication of this phenomenon, especially in Southern EU.

As the proponents of an ever-deeper integration are conscious of the unpleasant consequence that economic disintegration within E(M)U could unleash political forces destroying the union, efforts have been increased over the recent years to prevent this. Three strategies are being pursued in parallel:

Within the first strategy, different instruments have been promoted so far to support national governments in pursuing the necessary structural adjustments. Among them, the so-called European semester is aimed at coordinating single member’s economic policies, by preventing excessive macroeconomic imbalances across the EU, by ensuring that structural reforms are implemented and by boosting investment. While this first strategy could be viewed as the economically most meaningful way to achieve a lasting cohesion of the union, the results discussed above show that it is not particularly helpful in implementation. Consequently, the political will to push the integration project forward at all costs has shifted the focus to the other two strategies.

The second strategy is regarded as particularly vital for members of the euro area, which so far issue debt in a currency, over which they do not have any direct control. It is often argued that if the ECB were obliged to provide unlimited liquidity not only to banks but also to governments, this would provide bondholders an implicit insurance against the default of sovereign debtors, thereby reducing the fragility of an incomplete monetary union. Indeed, extensive monetary financing of insolvent or illiquid states, banks, companies or private households can – at least temporary – neutralize the destructive power of financial markets that became evident during the euro crisis of 2010-12.

Following up on ECB President Draghi’s famous promise to do “whatever it takes” to protect the euro, the ECB in September 2012 assumed eventually the role of lender of last resort to governments. It formally committed itself to purchase unlimited amounts of selected government bonds in crisis situations under the conditions of the so-called Outright Monetary Transactions (OMT) programme.

A crucial condition of this strategy to work is that the central bank’s commitment to act is never questioned by investors. However, there are several ways in which a loss of credibility of action might occur. It might come from outside due to deteriorating fundamentals or unsustainable fiscal stances of governments. Or it might be sparked by excessive inflationary pressures upon a substantial increase in liquidity in the system. The current strong expansion of money supply due to massive asset purchases by the ECB under the new Pandemic Emergency Purchase Program (PEPP), combined with limited practical options to withdraw liquidity at will, makes this scenario in the long-run increasingly likely.

Whereas the second strategy could be implemented almost unilaterally by the ECB, the last one is more cumbersome, as it requires reaching consensus on political matters, on which there is still insufficient agreement. Indeed, given that establishing a fiscal union would imply permanent transfers of financial resources from stronger to weaker members, opposition in the former countries still prevents the break-through to a full “transfer union”. For that reason, the proponents of this strategy have opted for a step-by-step introduction of elements of a transfer union by stealth. The two main elements include the instrument of common bond issuance (also known as Eurobonds) and the establishment of a banking union.10

Both instruments have faced fierce resistance in most of the economically stronger EU countries, although a substantial step towards Eurobonds was made with the common €750 billion debt issuance under the recent EU post-pandemic recovery fund (“Next Generation EU”). This resistance is justifiable on the ground of the aforementioned moral hazard risk, deriving from the incentive for countries and banks to rely on the implicit insurance offered at the union’s level. Against all official assurance, it is hard to believe that the new debt issuance of the EU will remain a temporary emergency tool and will not become a permanent measure once it is backed by European taxation.

The European Economic and Monetary Union is very far from being an optimal currency area. Since the previous integration efforts have not brought meaningful improvement in this matter, massive political interference is now in place to correct for the many imperfections. Without this strong political support, the union would most likely already have fallen apart. Indeed, in 2010-12, EMU was almost destroyed by centrifugal financial forces. The repositioning of the European Central Bank as a monetary financier of all entities in danger of bankruptcy has reduced the risks of EMU to collapse and neutralized the disciplinary role of financial markets. Now, the stepwise creation of a fully-fledged transfer union is supposed to neutralize the political discontent emanating from growing real economic disintegration. Through these measures, the life of EMU can be prolonged, but not saved. However, three forces could eventually kill EMU: First, high and persistent inflation unleashed by monetary financing of bankrupt entities, which could debase the euro and eventually induce people to substitute it by alternative means for the store of value and transactions; second, failure of recipient countries to use transfers wisely with a view to reduce real economic disparities; and third, political rebellion of taxpayers in paying countries against the waste of their taxes in recipient countries. Each of these forces is on its own powerful enough to cause a lasting damage on EMU. But taken together, they can be overwhelming.

1 Nominal integration in terms of prices and interest rates is less vital as a precondition for a well-functioning currency union and should rather be the consequence of real integration.

2 See, for instance, Krugman et al. [“International Economics: Theory and Policy, Pearson Education Limited, UK, 2018].

3 See, for instance, del Hoyo et al. (2017), Real convergence in the euro area: a long-term perspective, ECB Occasional Paper Series No. 203.

4 For more methodological details, see König and Ohr (2013) “Different efforts in European economic integration: Implications of the EU Index”, Journal of Common Market Studies, 51(6): 1074-1090. In developing their EU-Index, König and Ohr consider four different dimensions of integration, namely EU single market, EU homogeneity (convergence), EU symmetry and EU (legal and institutional) conformity. Among them, EU symmetry is a crucial economic precondition for an area forming a monetary union.

5 The distinction between indicators measuring nominal and real integration is not strict, as some indicators, like government finances, could be considered under nominal integration as well. However, given that government expenditures and revenues are likely to reflect the underlying real developments in a country, we classify it among the real-integration indicators.

6 All single-country correlation coefficients are available upon request.

7 This decline in correlation was due to Germany’s productivity performing increasingly worse than the EU average.

8 See Bolea et al. (2018) „From convergence to divergence? Some new insights into the evolution of the European Union“, Structural Change and Economic Dynamics, 47: 82-95.

9 For a textbook elaboration of these strategies, see Chapter 6 in De Grauwe, P. (2018) “Economics of Monetary Union”, 10th edition, Oxford University Press.

10 Some elements of the banking union, however, are worth pursuing. This is especially the case of the so-called liability cascade in the bank resolution, with clearly defined sequence applying for the liability of bank owners and creditors.

26.03.2020 - Macroeconomics

18.03.2020 - Macroeconomics

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch SE. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch SE remains solely with Flossbach von Storch SE. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch SE.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch SE.

© 2024 Flossbach von Storch. All rights reserved.

Agnieszka Gehringer

Senior Research Analyst

Agnieszka Gehringer joined the institute in 2015. She studied economics at the University of Rome “La Sapienza” and later earned a PhD in economics of complexity at the University of Turin. Since November 2019 she has been a professor of Economics at the Cologne University of Applied Sciences and since July 2016 a lecturer at the University of Göttingen. She has published several articles in academic journals and is an advisor to the EU.

All articles by Agnieszka Gehringer