08.04.2024 - Comments

The Bank of Japan has announced a change in interest rate policy. It raised the key interest rate from -0.1 per cent to a range between 0 and 0.1 per cent. This made it the last major central bank to abandon the negative interest rate policy it had pursued since 2016. It has also abandoned its yield curve control. It is thus reacting to the significant rise in prices and wages, which has averted the risk of deflation. In January, the inflation rate was 2.2 per cent, and the trade unions negotiated extraordinary wage increases of over 5.28 per cent in the latest spring offensive.

The German newspaper Handelsblatt saw a new era in Japanese monetary policy. "Wow, she did it," commented the chief economist at VP Bank. Euphoria has also been evident on the Japanese stock market for some time, which reached a new historic high following the announcement of the interest rate hike. Does this mean that the three lost decades since the bubble economy burst are finally a thing of the past? And what role does the renewed weakness of the Japanese yen play, which occurred despite the interest rate increase? A look back can provide more clarity.

The crisis, which continues to this day, can be traced back to the Japanese bubble economy. In September 1985, the USA had urged Japan into revaluing the yen against the dollar in the so-called Plaza Agreement, to correct the large trade imbalance between the two countries. The appreciation of the yen plunged the export-dependent Japan into a deep crisis, which the Bank of Japan attempted to cure by cutting interest rates. The cheap money made it easier for companies to carry out urgently needed restructuring. However, it also triggered a speculative bubble on the stock and property markets, the bursting of which dragged many property companies and banks, and ultimately the entire economy, into crisis. Figure 1 shows the sharp rise and fall of the Nikkei 225 share index between 1985 and 1992.

The Bank of Japan tried to deal with the crisis with the medicine that was the cause of the fatal exuberance. It pushed short-term interest rates up to and even slightly below zero and bought government, bank and corporate bonds on a large scale. This enabled Nippon's state to implement large debt-financed spending programmes, which repeatedly supported the weakening economy. By subsidising many products such as food, energy and local transport, the government not only kept inflation in check, but also justified the persistently loose monetary policy.

Companies became increasingly dependent on government spending, low financing costs and wage restraint on the part of trade unions. Inertia became so widespread that many now regard the Japanese economy as zombified. As productivity gains became depressed, real wages have fallen since 1998. Government debt has risen to 260 per cent of gross domestic product and more than half of the government bonds issued are on the balance sheet of the Bank of Japan.

This leads to the question of what can explain the recent boom in Japanese share prices. Under the headline "Japanese equities - a force awakens", the investment bank Franklin Templeton states that corporate reforms have reached a tipping point, signalling fundamental change. Indeed, rising interest rates and wages could finally force companies to undertake radical restructuring and efficiency gains. In addition, the Bank of Japan intends to reduce its purchases of corporate bonds and equities in the form of ETFs from now on.

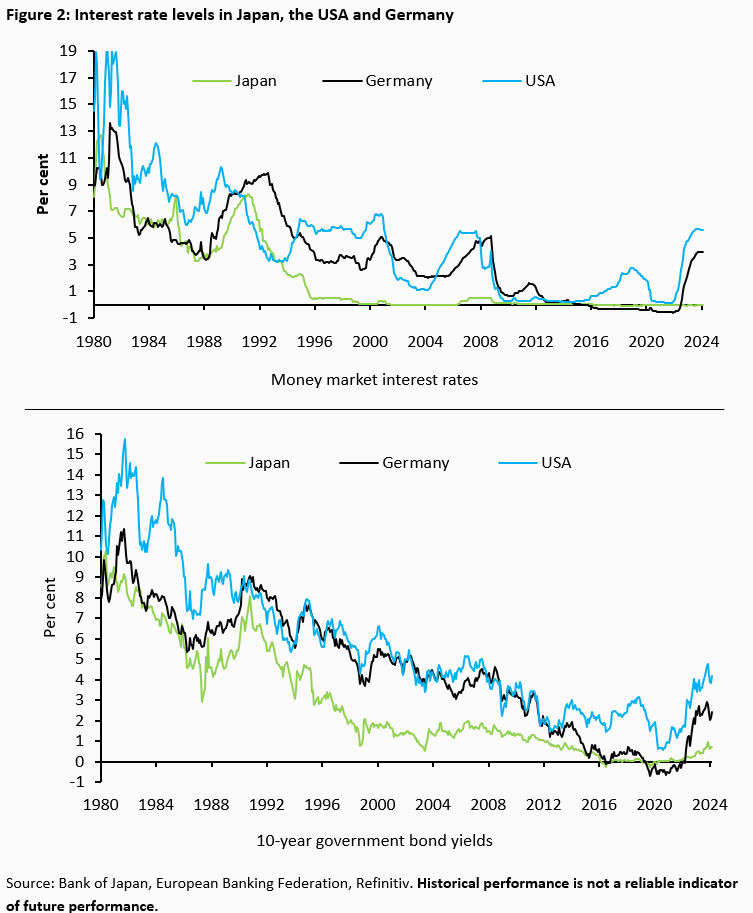

On the other hand, the Japanese yen has depreciated sharply against the dollar since January 2021. Whereas around 103 yen had to be paid for one dollar at the beginning of January 2001, it was over 151 at the beginning of April 2024, which corresponds to an increase of over 46%. The depreciation has boosted the profits of export companies, which are strongly represented in the Nikkei 225, enabling them to finance share buybacks. In addition, the depreciation of the yen has made Japanese shares cheaper for foreign investors. US star investor Warren Buffet, among others, has made a highly publicised purchase. The apparent success of Japanese companies could therefore be driven primarily by the fact that the Bank of Japan, unlike the Federal Reserve System and the European Central Bank, has largely refrained from raising interest rates at both the short and long end of the yield curve since 2022, as Figure 2 shows.

The negative aspects of the devaluation, i.e. the rise in import prices and the associated price increases, which have led to higher wage demands, are currently still regarded as a "virtuous circle" by the Bank of Japan. However, the price-wage spiral could already be the precursor to a new damper on growth because it can keep up inflation. The Bank of Japan's homeopathic interest rate hike, which has now been announced as a sensation, will hardly force companies into far-reaching restructuring programmes.

And unlike the US and the euro area, the Bank of Japan is not talking about reducing the amount of corporate bonds and ETFs on its balance sheet - so-called quantitative tightening. The number of corporate insolvencies remains low despite a slight increase since the historic low in 2022. Finally, trade unions could become cautious again with their wage demands as soon as companies' liquidity reserves are depleted and unemployment threatens.

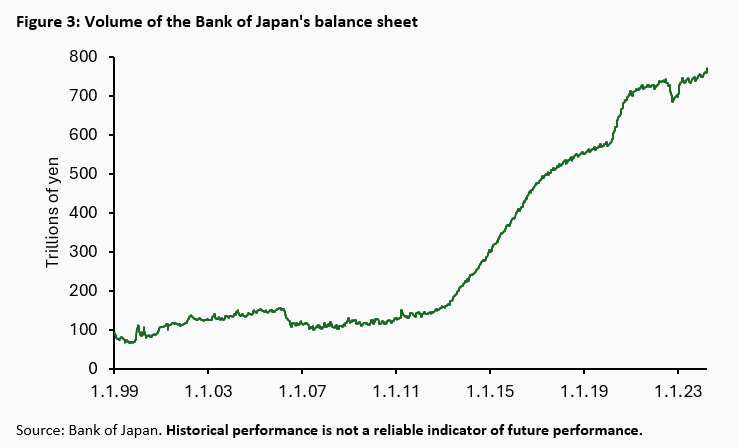

On the contrary, the Bank of Japan intends to continue buying government bonds to the equivalent of 40 billion euros per month, meaning that the balance sheet volume has not only continued to grow in contrast to the Fed and the European Central Bank (see Figure 3), but is also likely to continue to grow. In the event of a rapid rise in long-term interest rates, the Bank of Japan has announced that it could quickly increase the volume of purchases. This indicates that the immense national debt in Japan leaves it little room for manoeuvre.

The minimal increase in interest rates therefore appears to be more an expression of monetary policy dispair than a signal for a decisive tightening of monetary policy. A sustainable economic recovery would require much stronger interest rate hikes at both ends of the yield curve, which would require significant cuts in government spending and resolute corporate restructuring. Both the 67-year-old Prime Minister Fumio Kishida and the 73-year-old Central Bank President Kazuo Ueda still seem to be a long way from the necessary samurai spirit.

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.

Gunther Schnabl

Senior Advisor

Prof. Dr. Gunther Schnabl is Senior Advisor of the Flossbach von Storch Research Institute based in Cologne. Since April 2006, Prof. Schnabl has been the Chair of Economic Policy and International Economic Relations at the University of Leipzig, where he heads the Institute for Economic Policy. As a Senior Fellow, Prof. Schnabl primarily supports the Flossbach von Storch Research Institute in the areas of monetary and economic policy.

All articles by Gunther Schnabl