13.04.2022 - Comments

For more than two years the contagion dynamics of the coronavirus and the lockdown measures imposed by governments determined the global economy. Barely had the long-sought goal of mitigating the pandemic in the West become tangible as the next stagflationary shocks hit the global economy. Russian troops invaded Ukraine and China imposed renewed lockdowns to combat the omicron variant of the coronavirus. Commodity prices continued to rise and supply shortages worsened.

Stagflation and deglobalization burden the global economy to different extents. The U.S. is likely to be the least affected, the euro area the most. The development of the Chinese economy depends on whether the government sticks to its counterproductive zero-covid strategy, gets a grip on the financial risks in the real estate sector, and avoids being pulled into the whirlpool of Western sanctions on Russia.

Following the decline in global GDP in 2020, among the largest economies only the euro area failed to return to its previously trend growth. After a slump of -6.5% in 2020, euro area GDP at the end of 2021 was still 3% below the trend value projected from 2009-19. In the U.S., real GDP fell by 2.3% year-on-year in 2020, but thanks to a rapid recovery, first of industry and later of retail, it returned to the trend value in 2021. In China, GDP rose by 2.3% in 2020, less than the 6% to 7% of previous years, and in 2021 it was slightly above trend (figures 1 - 3).

Europe versus U.S.

Due to the lockdowns in 2020, demand fell, especially for services such as travel, tourism, and restaurants. Due to the imposed demand shortage, suppliers initially lowered prices, although they failed to attract demand back by doing so. Central banks mistakenly interpreted the price decline as deflation caused by voluntary demand cuts and increased the money supply by creating new money for governments to compensate earnings losses forced by the lockdowns (Figure 4).

Once the lockdowns were gradually lifted, it became clear that damaged supply chains continued to constrain potential supply, while demand, fueled by monetary and fiscal policy, was rapidly rising. The structural demand overhang pushed inflation to heights not seen in decades. Central banks held to their erroneous analysis until the end of 2021, admitting only since the turn of the year that inflation had not just "temporarily" returned.1

Consumer price inflation had already reached record highs by the beginning of 2022 due to sharply rising energy prices in the U.S. and Europe (Fig. 5). But core inflation excluding energy and food prices also climbed to 6.4% in the U.S. in March and to 2.7% in the euro area in February, well above the central banks' 2% target. The sharp rise in commodity prices following the Russian invasion of Ukraine is now pouring more fuel on the inflation fire. In March, the harmonized consumer price index rose by 7.3% year-on-year in Germany and by an expected 7.5% in the euro area.

Due to their misjudgment of the effects of the pandemic and the additional price shock caused by the Ukraine war, central banks now find themselves in a dilemma. To fight inflation, they would have to eliminate excess demand through a restrictive monetary policy. But this can only succeed if nominal interest rates rise above inflation. Positive real interest rates, however, would cause trouble for euro area member states and weigh on the stock market, which in turn would cause trouble for policymakers in the United States. Of course, this could be avoided if fiscal policy became restrictive. But there is probably little or no political will to do so.

Central banks, however, cannot remain completely dormant in the face of record high inflation. The Fed raised its key interest rate and announced further steps. The ECB decided to phase out its bond-buying program more quickly than originally intended and opened the door for an increase in its policy rates before the end of the year. This sparked fears of recession on the markets.

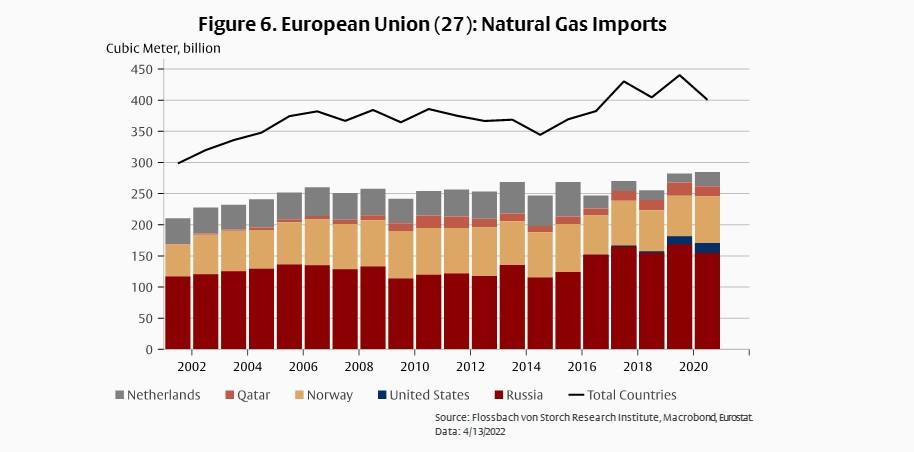

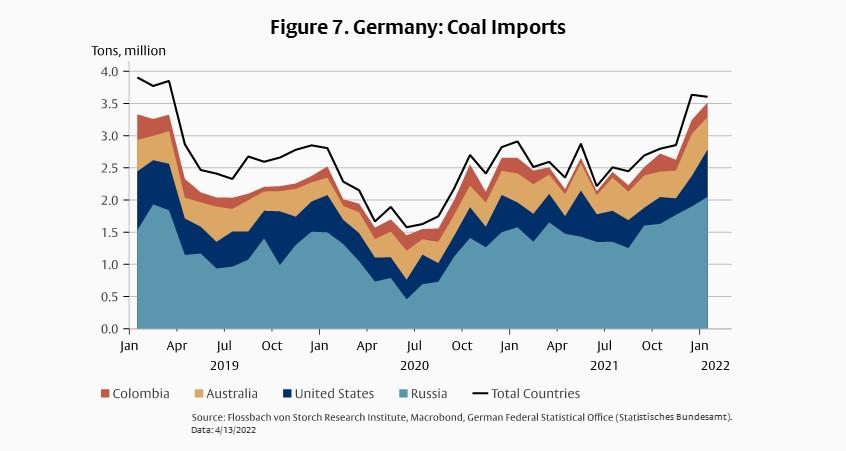

The risk of recession is increasing, particularly in the euro area, due to the sanctions imposed on Russia because of the war in Ukraine. The massive increase in the prices of raw materials such as oil, coal and natural gas is putting a strain on industrial production. As the European Union meets a large part of its raw material requirements through imports from Russia, a boycott of Russian energy imports would curb production. Without a corresponding simultaneous curbing of demand through restrictive monetary and fiscal policy, the stagflationary impulse would be enormously reinforced (figures 6 and 7).

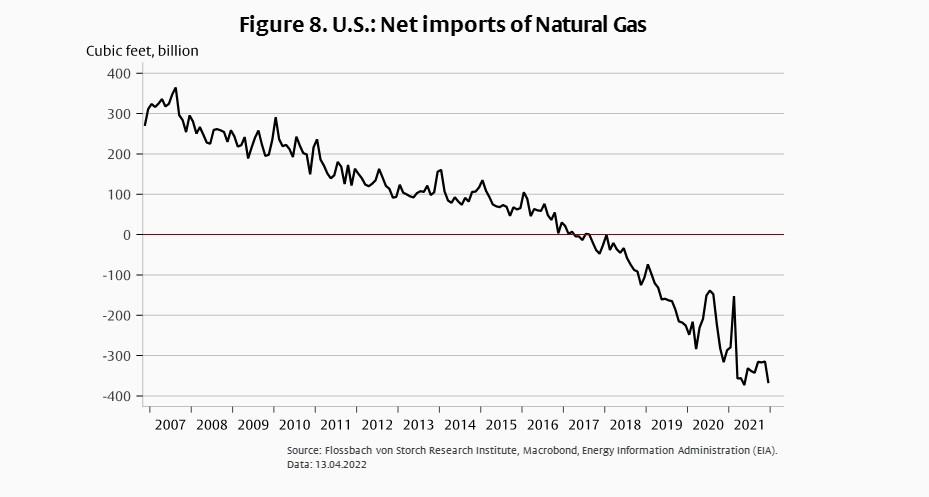

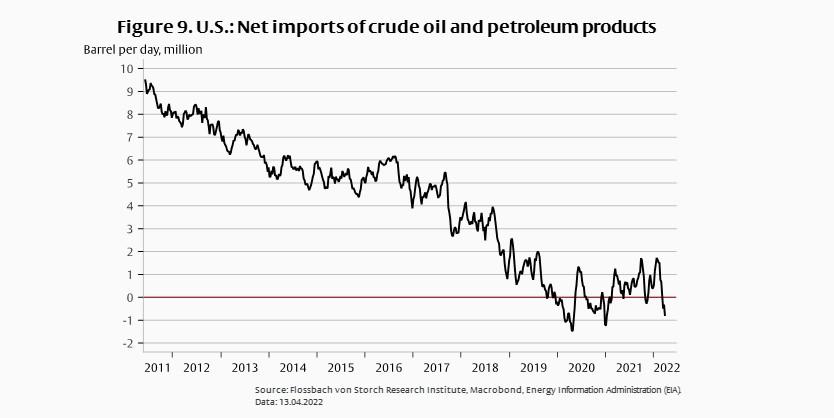

The U.S., on the other hand, benefits as a net exporter of raw materials from rising commodity prices in world markets (Figures 8 & 9). At the same time, higher prices provide incentives for increasing production. The relative price changes, however, are also likely to drive inflation in the U.S., as rapid reallocation of resources to the commodity sector is difficult and wages and prices in other sectors are often rigid to the downside. Instead of classic stagflation, the U.S. could potentially experience "growthflation" if monetary and fiscal policies do not forcefully address this.

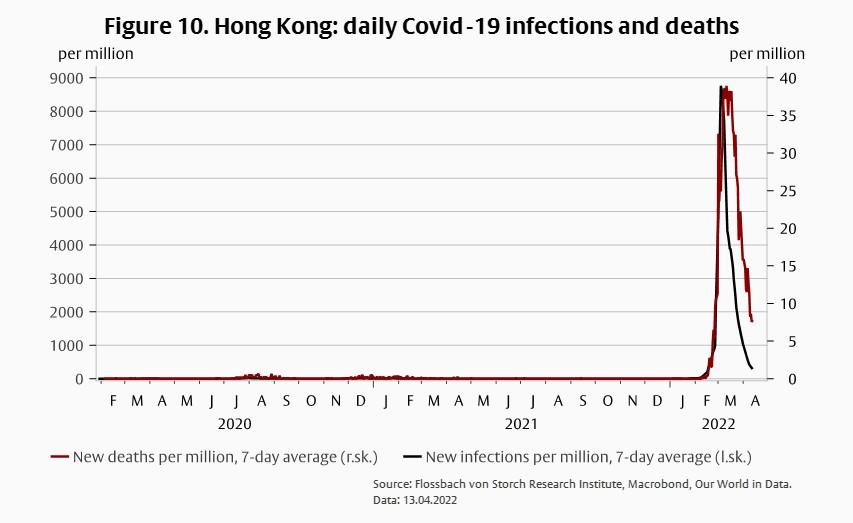

After two years of the government's successful zero-covid strategy to prevent the spread of the coronavirus and a rapid recovery of the real economy after the initial shock, the highly contagious Omicron variant can hardly be controlled with lockdowns. The spread of the virus in a population without extensive immunity through surviving disease or vaccination could lead to a wave of deaths like the recent one in Hong Kong (Figure 10).

In both Hong Kong and China, the vaccination rate among the elderly was just around 60% until a few weeks ago, and those who were vaccinated were given a less efficient locally produced vaccine. A rapidly rising Omicron wave in Hong Kong led to an overwhelmed health care system and high death rates. Holding on to the zero-covid strategy, however, limits economic activity and prolongs supply chain bottlenecks that have persisted for more than a year. The fight against coronavirus in China is proving to be a significant drag on growth.

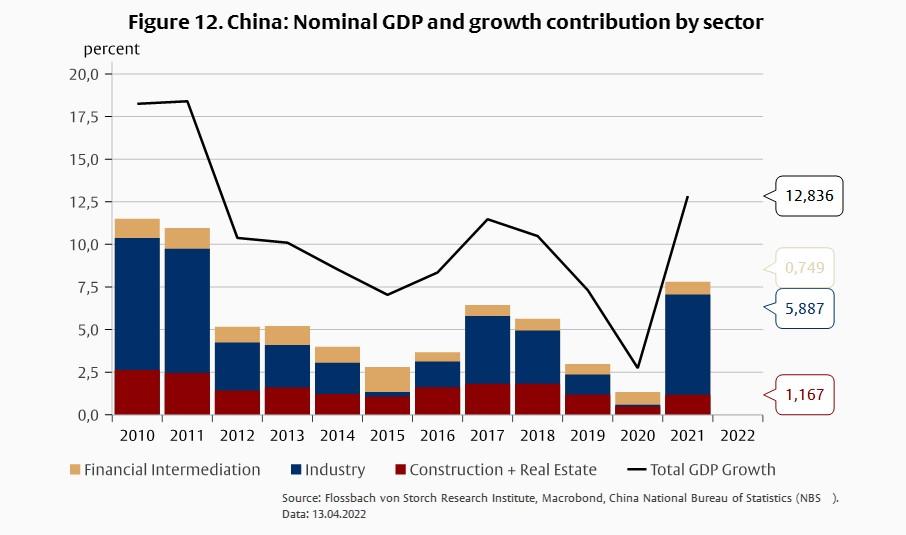

At the same time, risks in the real estate sector are increasing. Over the past 20 years, large Chinese cities have experienced a real estate boom. According to calculations by Rogoff and Yang (2021), the World Bank and the OECD, the share of production and services in GDP associated with the real estate sector is between 25% and 30%. Seeing in the credit-fueled boom a stability risk, the government decided in 2021 to restrict credit availability through more restrictive regulations to cool the real estate market. Insolvencies of over-indebted companies followed, and in February residential property prices fell by 10% (Fig. 11).

With a direct and indirect share of 25% of gross value added, a collapse of the real estate sector could plunge the economy into recession. To prevent this, the state could support the sector. Instead of a recession, the zombification of banks and companies would then weaken growth in the long term.2

Before the 20th Party Congress in the last quarter of this year, political and economic stability are likely to be particularly important for state leader Xi Jinping. Therefore, the government can be expected to suppress turbulence in the real estate and financial sectors. Against the backdrop of problems in the real estate sector and the pandemic policy, China can be expected to keep its distance from Russia in the Ukraine war to avoid financial and economic sanctions.3

While the euro area has not yet entirely recovered after two years of the pandemic and is being hit hard by the boycott against Russia, the U.S. has left the pandemic behind and can benefit from the commodity price boom. The overheating of the U.S. economy, however, could lead to a monetary tightening that triggers a recession.

The outlook for China depends on how long the government sticks to the zero-covid strategy and whether the decline in property prices will have far-reaching consequences for the financial sector. While the Chinese government will fight any crisis strongly, if longer-term growth prospects deteriorate, the Chinese leadership's political acceptance could dwindle.

1 See our Newsletter „Good-bye Transitory“ from 04.02.2022 (only in German) www.flossbachvonstorch-researchinstitute.com/fileadmin/user_upload/RI/E-Mails-Archiv/220204-inflation-update-goodbye-transitory.pdf.

2 See Siehe Schnabl, G. (2019). China's overinvestment and international trade conflicts. China & World Economy, 27(5), 37-62.

3 Regarding the relationship between Russia and China, Tofall (2022) argues, "China is therefore likely to behave in the current Ukraine conflict in such a way that Russia ultimately becomes China's junior partner. From China's point of view, however, this junior partner should not be weakened in such a way that China can no longer benefit economically and politically from Russia." See “China and Putins war in Ukraine”, Comment, Flossbach von Storch Research Institute, 11.03.2022.

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.