02.06.2021 - Comments

When Keynes, inspired by the Great Depression of the 1930s, developed his theory, it was perhaps forgivable that he completely ignored money creation by banks. Today, however, ignoring the role of banks leads to blatant misconceptions.

Paul Krugman is a Nobel laureate and very influential economics columnist for the New York Times. When he writes about monetary policy, his readers expect him to understand what he is talking about. Unfortunately, his column of 21 May suggests that this may not be the case (https://www.nytimes.com/2021/05/21/opinion/money-federal-reserve-deficit.html). One wonders how many other high-profile economists of the Keynesian school, which currently dominates thinking in universities and central banks, also do not know what they are talking about.

Mr. Krugman, in his column, dismisses the criticism that the Fed is printing money to finance the federal government's budget deficit. He reasons, “At a fundamental level, households are financing the deficit: the funds being borrowed by the government are coming out of the huge savings undertaken by families saving much of their income in an environment where much of their usual consumption hasn’t felt safe.”

He admits that US households cannot hand over their savings directly to the government but have to go through the banks: “Families are stashing their savings in banks. Banks, in turn, have been accumulating reserves — that is, lending to the Fed, which these days pays interest on bank reserves. And the Fed has been buying government bonds.” If one of my students had presented these sentences in a seminar paper, I would have taken him aside and suggested that we recapitulate what is really going on here.

When a central bank buys a government bond, it gives an order to a commercial bank. The latter buys the bond from a market participant and passes it on to the central bank. To settle the transaction, the central bank pays reserve money into the central bank account of the commercial bank. In return, the commercial bank creates bank money and credits it to the bond seller. At the end, the central bank has a new asset in the form of the government bond and a liability in the form of central bank money on the commercial bank's account. The latter has central bank money as an asset and bank money as a liability. The bond seller has exchanged his government bond for bank money. This increases the money supply.

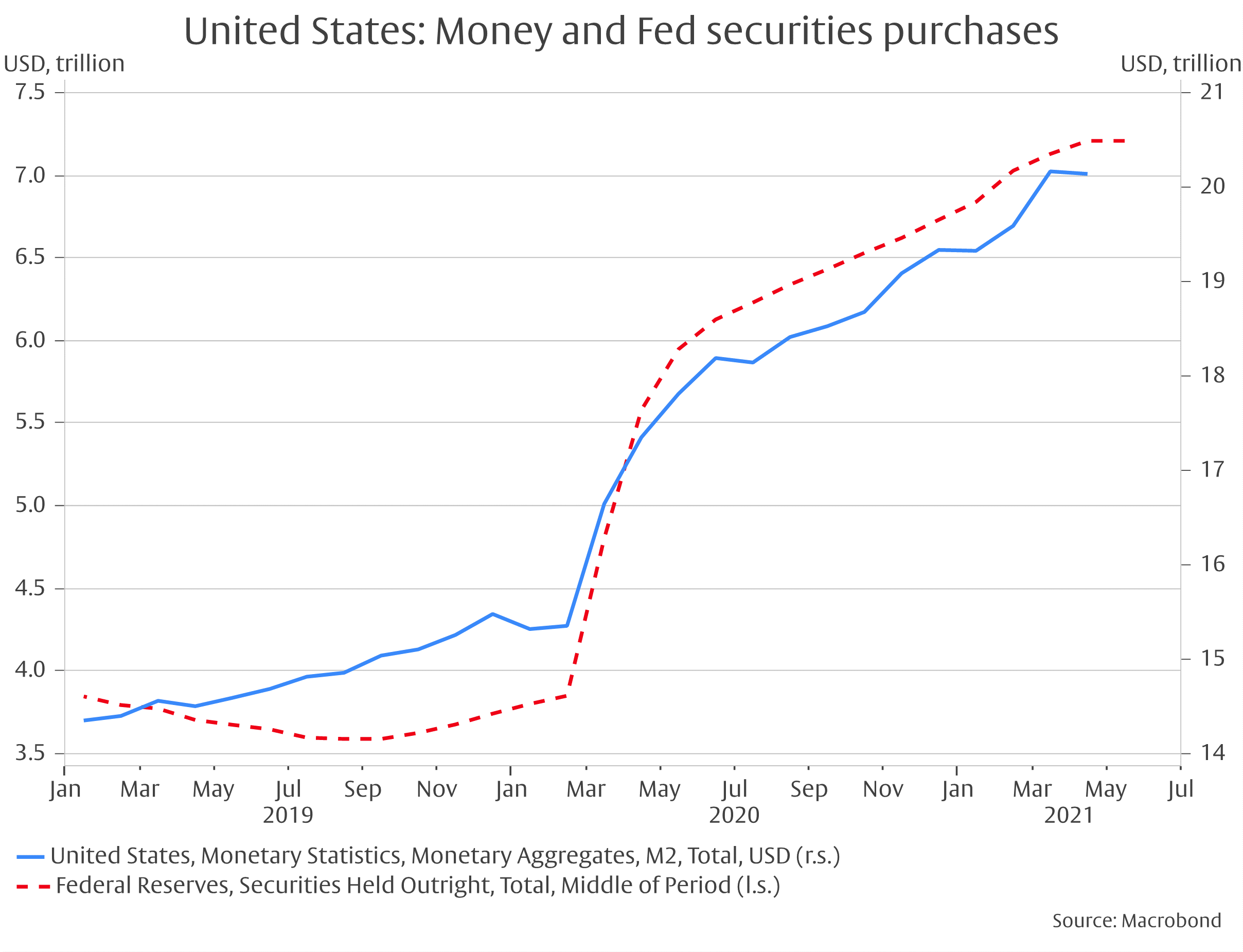

The facts support the reasoning: Between January 2019 and February 2020, the Federal Reserve's securities holdings remained unchanged, and the money supply (M2) increased by only one trillion US dollars. Between February 2020 and April 2021, securities holdings increased by 3.5 and the money supply by a whopping $4.8 trillion.

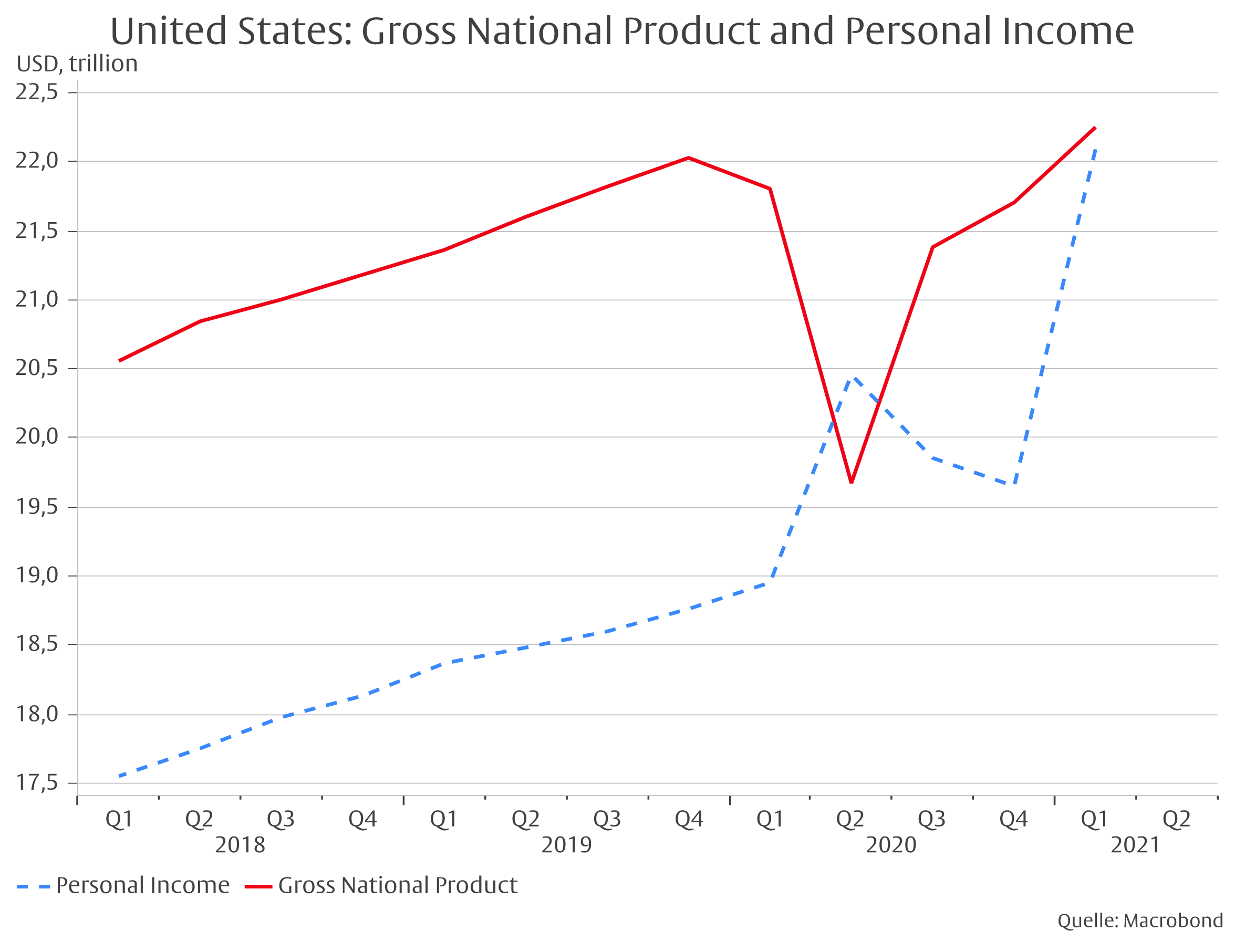

Let us assume that the government now exchanges a new bond issue for bank money with the seller of the first bond and transfers this bank money to private households. Now personal disposable income rises. Thanks to the transfer, this can happen even when the gross national product falls. For example, between the fourth quarter of 2019 and the second quarter of 2020, nominal gross national product fell by $2.4 trillion, while personal disposable income rose by $1.7 trillion.

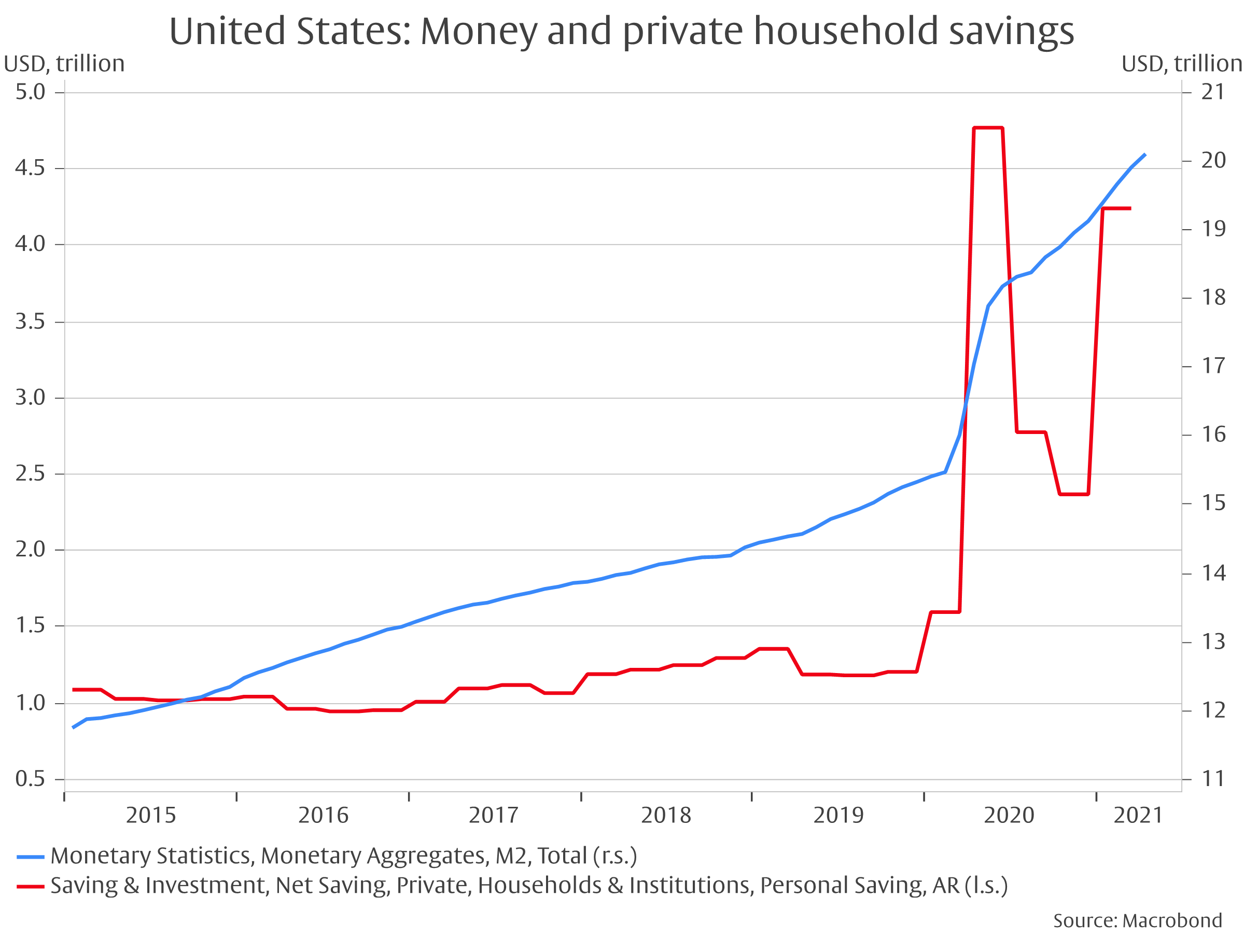

Let us now further assume that households have no way to spend the increase in personal disposable income. As a result, their money savings increase. Between January 2020 and June 2020, household savings increased by $3.2 trillion, while the money supply increased by $2.8 trillion. So, the bottom line is that money savings have been increased by government transfers of money created by the central bank for the government.

Mr. Krugman, on the other hand, concludes in his column: “The Fed isn’t the Venezuelan government printing bolívars to pay its soldiers; it’s basically acting as a financial intermediary for investors who want to park their money somewhere safe. And while there are plenty of reasons to worry about what’s going on in the U.S. economy, Fed purchases of bonds and rising M2 aren’t on the list. Chill out.”

He is right that the Fed is not the Venezuelan government, but it prints dollars for the US government. You don't have to be a monetarist to expect nominal GDP to rise as households reduce their cash savings when the pandemic subsides. This will boost output and employment. But given the scale of money creation, it would be very surprising if prices did not rise as well.

Mr. Krugman is not alone in his misjudgment about the effects of monetary policy. On 23 February, Federal Reserve Chairman Jerome Powell told a Congressional hearing: “Well, when you and I studied economics a million years ago, that M2 and monetary aggregates generally seem to have a relationship to economic growth. Right now, I would say the growth of M2, which is quite substantial, doesn’t really have important implications for the economic outlook. M2 was removed some years ago from the standard list of leading indicators, and just that classic relationship between monetary aggregates and economic growth in the size of the economy, it just no longer holds. We’ve had big growth of monetary aggregates at various times without inflation, so something we have to unlearn, I guess.”

Why can leading economists and central bankers come to such conclusions? The answer is that Keynesian theory completely ignores the money creation by banks. When Keynes, inspired by the Great Depression of the 1930s, developed his theory, this was perhaps forgivable. Today, however, ignoring the role of banks leads to blatant misconceptions.

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.