12.09.2023 - Studies

Like many other central banks, the European Central Bank is contemplating the introduction of a digital central bank currency (CBDC). In principle, CBDCs can replace electronic bank transfers and initiate a comprehensive reform of the fiat-credit-money system.1 This system has facilitated the enormous increase in private and public indebtedness and been the source of many monetary and financial crises over the last half century. If the introduction of CBDCs were used to end this system, we could not only expect more monetary stability, but also make a leap towards public debt reduction. This paper proposes a monetary reform in the euro area by combining the introduction of the digital euro with the Chicago Plan of 1933.2 Yet, because of political resistance – fueled by special interests - it is unlikely that the introduction of a digital euro will be used as an opportunity for the strengthening of the architecture of the euro and for a reduction of public debt.

The history of cryptocurrencies can be traced back to the 1980s, when David Chaum, a computer scientist, developed the idea of digital cash and created the first digital currency, called eCash. However, it was not until the emergence of Bitcoin in 2009 that cryptocurrencies gained widespread attention.

The orange pill

Bitcoin was created by an anonymous person or group of people using the pseudonym Satoshi Nakamoto. The idea behind Bitcoin was to develop a decentralized digital currency that would not be subject to the control of any government or financial institution and cheap to use. Moreover, Nakamoto blamed the fiat credit money system for the long series of financial crises that culminated in the bankruptcy of Lehman Brothers in September 2008. Therefore, he called for the change to a system where money would not be “lent into existence”. The technology that made this possible was called blockchain, which is a cryptographic computer technology that allows for secure and transparent transactions without the need for central ledgers.

By its fans, Bitcoin has been called the "orange pill" because of the resemblance between the color of Bitcoin's logo and the color of the popular prescription drug, Adderall, which is often referred to as the "orange pill". The term "orange pill" has been used to describe the process of becoming fully aware of and committed to the principles and potential of Bitcoin, similar to how taking the "red pill" in the movie "The Matrix" represents the awakening to a new reality. The success of Bitcoin led to the creation of many other cryptocurrencies, including Litecoin, Ripple, and Ethereum. Each of the alternative cryptocurrencies has its own unique features and uses, but they all share the underlying technology of a distributed ledger (for which the blockchain is the most famous example).

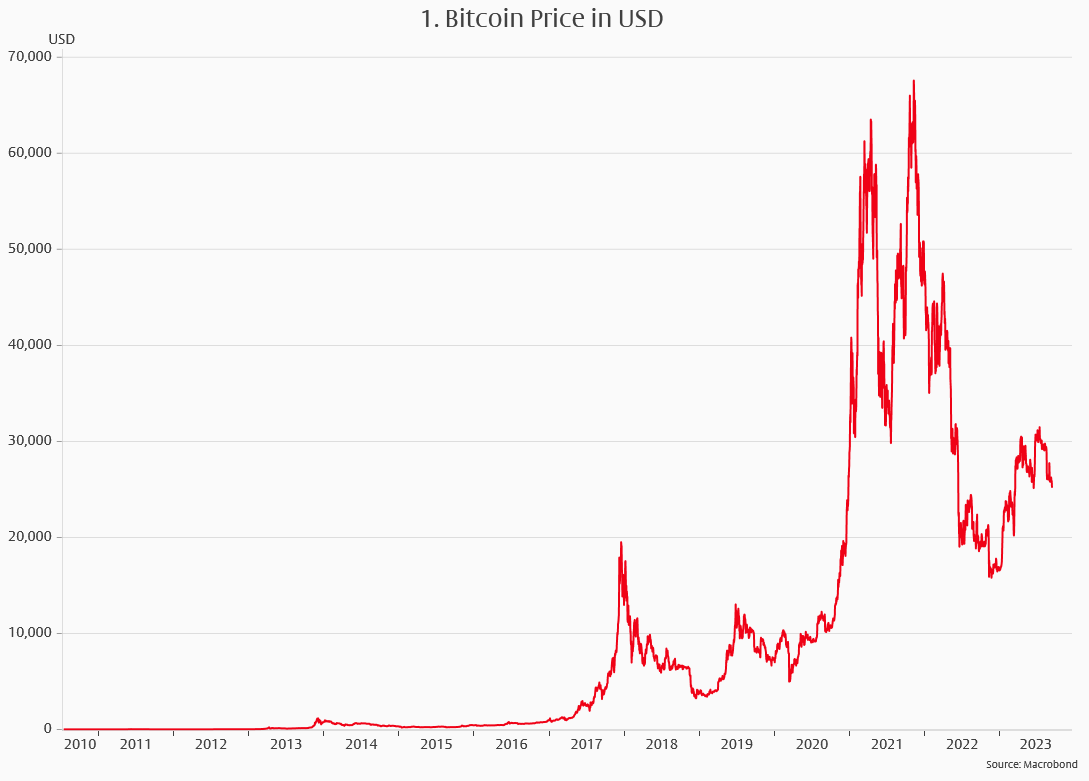

Cryptocurrencies have had a tumultuous history, with their value fluctuating wildly over the years. In 2017, Bitcoin reached a first high of nearly USD 20,000 before crashing down to around USD3,000 in 2018 and recovering again to another high of almost USD 70.000 in November 2021 (Chart 1). Only to crash again in 2022. Despite these ups and downs, cryptocurrencies continue to attract a lot of attention from investors, entrepreneurs, and governments around the world.

Today, cryptocurrencies are used for a variety of purposes, from online payments to investments, albeit on a small scale. Several businesses accept cryptocurrencies as a form of payment, and they have become parallel currencies to the national currencies in some countries, where confidence in the national currency is low. However, cryptocurrencies remain a controversial topic, with concerns around their security, volatility, and potential use in criminal activities. China has banned Bitcoin while many authorities of western countries try to shift public opinion against cryptocurrencies. Perhaps, because they fear competition to their sovereign currencies.

From Stable Coins to CBDCs

Stablecoins are a type of cryptocurrency that is designed to maintain a stable value, usually pegged to a fiat currency. Unlike other cryptocurrencies, which can be highly volatile and subject to price fluctuations, stablecoins are supposed to offer a more predictable value that is intended to be immune to the wild fluctuations of crypto currency markets. They promise lower transaction costs for electronic money transfers than is charged by payment services providers for transactions in state currencies.

There are several types of stablecoins, including fiat-currency-backed, cryptocurrency-backed, and algorithmic stablecoins. Fiat-backed stablecoins are collateralized by a reserve of sovereign currency, typically held in a bank account, while cryptocurrency-backed stablecoins are collateralized by another cryptocurrency, such as Bitcoin or Ethereum. These coins resemble a Currency Board used for pegging a sovereign currency to a major foreign sovereign currency. Algorithmic stablecoins, on the other hand, use complex algorithms to automatically adjust the supply of the stablecoin based on market demand, in order to maintain a stable exchange rate to some reference value.

Stablecoins are intended for a variety of purposes, including facilitating international trade, providing a more stable medium of exchange for daily transactions, and as a store of value. One of the main advertised benefits of stablecoins is that they offer the advantages of cryptocurrencies, such as fast and low-cost transactions, while also providing the stability of traditional currencies.

Facebook's (now Meta) proposed stablecoin, Libra, plaid a role in triggering the development of central bank digital currencies (CBDCs). When Libra was announced in June 2019, regulators and policymakers feared that it would develop into a popular substitute for sovereign currencies. They were concerned about the potential impact of a privately issued digital currency on financial stability. And they feared that governments would lose the ability to use money for policy purposes, ranging from the stabilization of business cycles to the use of money creation for government funding. Last but not least, they were frightened by the prospect of losing their “seigniorage” income from issuing paper money.3

In response to these concerns, central banks around the world began to explore the potential development of their own CBDCs, as a means for maintaining control over monetary policy. This led to a flurry of research and development activities in the field of CBDCs, with many countries launching pilot projects and conducting feasibility studies. There are two main types of CBDCs: retail and wholesale. Retail CBDCs are designed for use by the public to make payments and purchases, just like traditional fiat currencies. Wholesale CBDCs, on the other hand, are designed for use by financial institutions, and can be used for interbank settlements and other large-scale transactions. Attention has recently mostly focused on retail CBDCs.

For example, China's central bank, the People's Bank of China (PBOC), was one of the first major central banks working on its own digital currency for general use, known as the digital yuan or digital renminbi. The PBOC's digital currency is being tested in several Chinese cities and is to be rolled out nationwide when the tests are finished. Similarly, the European Central Bank (ECB) launched a public consultation on the potential development of a digital euro, citing concerns about the potential impact of Libra on the eurozone's monetary sovereignty and financial stability. While Libra may not have been the sole catalyst for the development of CBDCs, it certainly played a role in raising awareness about the potential benefits and risks of digital currencies, and in spurring central banks to take action to protect their respective monetary systems.

Central bank digital currencies are digital alternatives to traditional fiat currencies, issued and backed by central banks. They are designed to provide a secure, efficient, and cost-effective means of payment and settlement, and have the potential to transform the way we use money. CBDCs are typically based on distributed ledger technology (DLT), such as blockchain, which allows for secure and transparent transactions without the need for intermediaries. Unlike private cryptocurrencies, which are decentralized and not backed by any central authority, CBDCs are backed by the central bank and are subject to government regulation.

CBDCs are said to offer several potential benefits, including increased financial inclusion, lower transaction costs, and greater efficiency and security in payment systems. They can also provide a means of combating financial crime and reducing the use of cash, which can be expensive to produce and distribute, and can facilitate illegal activities. However, there are also some potential risks associated with CBDCs, including the possibility of cyberattacks, data privacy concerns, and the potential for CBDCs to destabilize the financial system if not implemented properly. Some people fear that the replacement of paper money by a CBDC would offer the possibility to levy negative interest rates on central bank money in general, as it was imposed by several central banks in the 2010s on reserve money.

Central banks have designed their prospective digital currencies as an add-on to the fiat credit money system. To avoid the crowding out of bank money by their CBDCs, ECB officials have contemplated containing wallet sizes to relatively small amounts.4 In the euro area, holdings of paper banknotes amount to about €5,330 per person older than 14 years. Against this, bank deposits amount to about €52,830 per (adult) head. Thus, with a contemplated wallet size of up to €3,000, the CBDC is designed not to become a threat to bank deposits and to be at most a partial substitute for banknotes.

To our knowledge, central banks have not engaged in a more comprehensive debate on the merits of the fiat credit money system. Hence, their intention to protect it from the introduction of CBDCs is unclear. The only cohesive argument we have come across is that they fear banking crises because of sudden flights of bank account holders into CBDCs. Such flights, so the argument, could occur when large credit failures undermined confidence in bank money and induced bank runs. As long as accountholders had only paper banknotes as a substitute to bank money, bank runs could be contained more easily.

However, this argument is unconvincing for two reasons: First, those who subscribe to it assume that the option to trap people in an accident-prone money system is better than to reform the system to make it more robust. Second, they assume that banknotes are the only safe alternative to bank money. However, as the run on Silicon Valley Bank in the US in March 2023 has shown, bank runs can today occur by electronic transfer of bank money to safer assets, be they deposits at banks with government protection because they are too big to fail, private money such as bitcoin, or money market funds investing in short-term government paper.

In our view it would be a benefit for money users if CBDCs were established as alternatives to both paper banknotes and bank sight deposits. This would increase the freedom of choice for users and relief governments from the burden of insuring against the systemic risk of bank runs. The banking business would of course change if debtors preferred to borrow CBDCs instead of bank money created for them through credit extension. But banks have no natural right to profit from money creation and will find other profitable business when customer preferences change.

While these considerations apply to CBDCs in general, we see a particularly strong use case in creating a digital euro. Calling the euro area a “monetary union” is an unsubstantiated overstatement. In reality, it is only a cash union. The paper banknotes issued by the European Central Bank are of the same credit quality in all euro area member countries. But the credit quality of bank money is different. Without a common deposit insurance funded jointly by the governments of member states, the credit quality of bank money depends on national governments’ financial capability to back the bank money in case of systemic bank runs. As Greek residents found out in 2015, euro bank money cannot be exchanged against paper banknotes or transferred abroad when a government is broke.

Financially weaker countries and EU institutions have lobbied for the establishment of a common deposit insurance scheme (EDIS). But the financially stronger countries have resisted the risk transfer to them associated with such a scheme. Even if these countries yielded to the pressure, it is unclear whether the scheme would work under stress. To stop bank runs in the wake of the failure of Silicon Valley Bank in March 2023, US authorities announced an unlimited guarantee for bank sight deposits. But would euro area governments really be willing to guarantee 1.5 trillion Euro held in Italian sight deposits, if a bank run developed, perhaps because of fears of bankruptcy of the Italian state? The question would not arise if a digital euro existed as 100%-money.

Moreover, several euro area countries are highly indebted and need the European Central Bank as a lender of last resort to remain credit-worthy in the markets. A monetary funding backstop is not only contrary to the European Treaty but also a serious handicap for the ECB in fighting inflation. Introduction of a digital euro could reduce government debt outstanding in the market and hence bolster the perception of the euro as a hard currency. It would also materially change the work of the ECB – we think to the better. In the following we explain how the digital euro as 100%-money could be introduced, and what would be the consequences and benefits.

Introducing the secure deposit

The first step towards the euro as 100%-digital central bank money would be to create a euro bank deposit fully backed by central bank money. In turn, the central bank money necessary for collateralizing the deposit would be covered by government bonds (as proposed in the Chicago Plan of 19335). Between 2015 and 2022 the ECB bought large amounts of public and private bonds to increase the money supply. By contrast, the secure deposit would replace existing deposits without increasing the money supply.

When owners of existing deposits transfer their money to a secure deposit the sum of deposits and hence money supply remain unchanged. To create the reserve cover, banks could use the large amount of excess reserves they already acquired by transacting the asset purchases for the ECB. They could obtain additional reserves needed to back secure deposits by selling government bonds they hold on their balance sheets to the ECB, or, if they have no government bonds, they could buy these in the market against other assets they hold. When necessary, the ECB could accept also other bank credit than government bonds from banks in exchange for reserve money and replace these claims with government bonds when they are redeemed. Thus, a secure deposit and asset as safe as banknotes would be created without the need for any form of deposit insurance by the states.

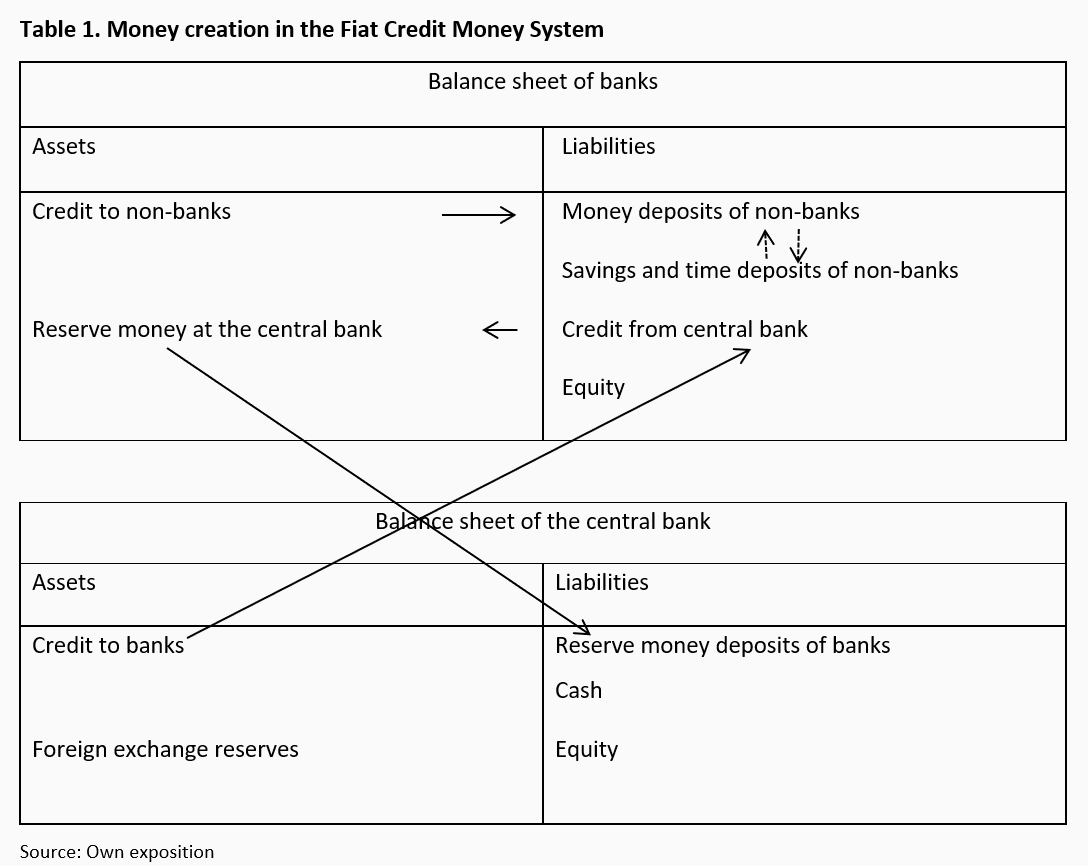

In the following we first compare the difference between the credit money system and the 100%-money system, and then illustrate the move from one to the other, with the help of simple balance sheets. Table 1 gives stylized balance sheets for the commercial banking sector and the central bank. In this example the banks extend credit to non-banks and create sight deposits in return (as demonstrated by the arrow going from credit to deposits). Some of these deposits move into savings and time deposits (arrow downwards) and will move backwards on maturity (arrow upwards), depending on the premium banks were willing to pay to tie up some of the money deposits for some time. The banks borrowed from the central bank (with credit to the non-bank sector as collateral) (arrow for central bank credit going from central bank to banks), and now hold the reserve money in the form of deposits with the central bank (arrow for reserve money going from banks to central bank). The credit extended by the central bank matches its liabilities in the form of reserve money deposits by the banks (while in this simple example cash and equity of the central bank fund the foreign exchange reserves).

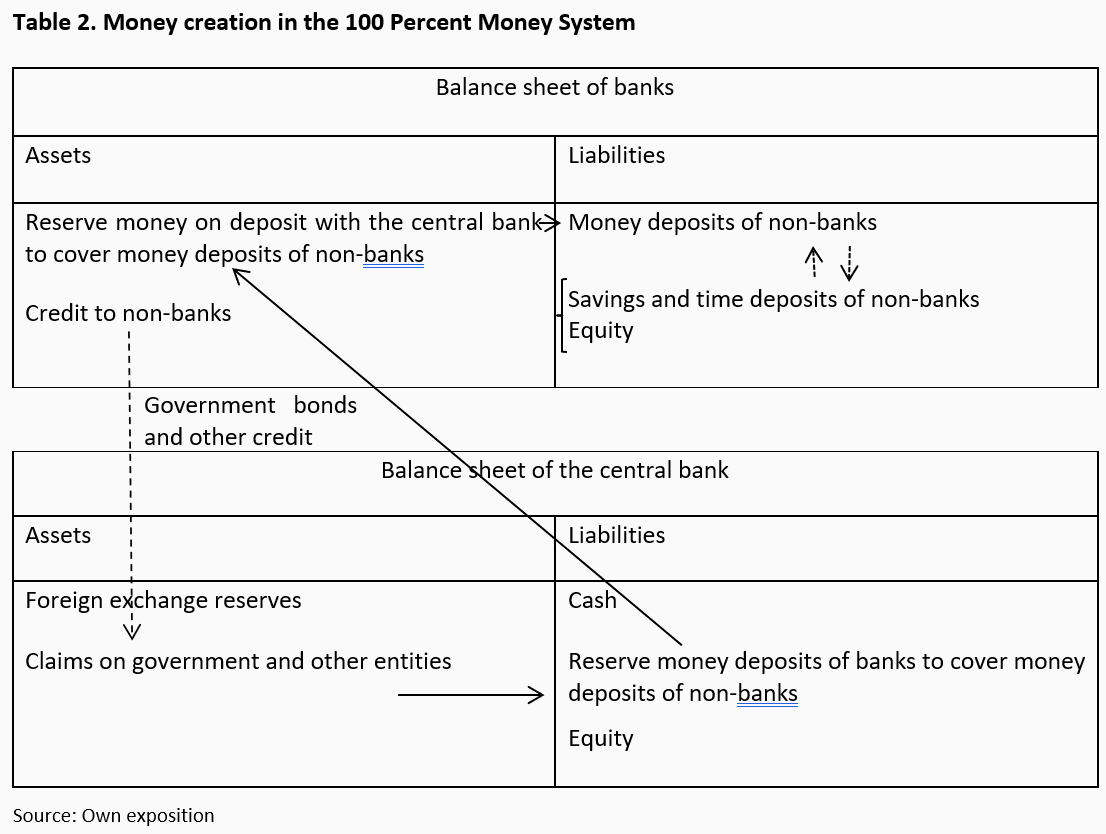

Now we move from the credit money system to the 100%-money system. This is illustrated in Table 2. In the first step, the central bank buys government bonds and, if necessary, other credit to non-banks from the banks against reserve money, until banks’ reserves are equal to the stock of money deposits (dotted arrow going from banks’ credit to non-banks to central bank’s claim on government and other entities, and arrow from there to reserve money deposits of banks to cover money deposits of non-banks on the liability side of the central bank’s balance sheet). Any private debt would be sold again against government debt to collateralize reserves covering money deposits entirely by government bonds.

Thus, the stock of money is initially determined by the central bank through purchases of government and (if necessary) private debt from banks (see arrows going from central bank’s claim on governments to reserve money deposits on central bank’s liability side and banks’ asset side of the balance sheet, and from there to money deposits of non-banks on the liability side of banks’ balance sheet).

As long as the volume of secure deposits remains below a level of liquidity deemed consistent with price stability, the central bank exchanges bank deposits against secure deposits at parity. When the volume of secure deposits begins to exceed the level of liquidity deemed consistent with price stability, the central bank ends the exchange at parity, freezes the volume of the secure deposit, and allows the market to establish an exchange rate between bank deposits and secure deposits. Thus, bank deposits would trade at variable prices like any other senior short-term bank debt. The price of bank deposits could vary between banks depending on their credit quality and ability to pay interest (as other bank debt does already).

Secure money deposits can be moved into bank savings accounts or equity instruments offered by banks to fund credit extension. To this end, the banks conclude with the depositor a savings or time deposit contract, or they sell equity shares to him. To lend the money on, the banks conclude a credit contract with the debtor. Thus, money moves from the account of the saver to the account of the debtor.

When lending takes place, the stock of money remains unchanged. But the balance sheet of the banking system increases due to the credit contract and the associated contracts for the funding of it, which transfer the temporary use of money from lender to borrower against a lending fee. In the 100%-money system, banks actually “intermediate” between savers and investors, as many economic textbooks erroneously claim this to happen in the fiat credit money system.6 If the holder of a secure money deposit wants to exchange this into paper money, the bank cancels the deposit, obtains with its reserve money holding paper money and pays this to the customer. The bank’s balance sheet decreases while reserve money deposits of banks decrease and paper money outstanding increases on the liability side of the central bank’s balance sheet.

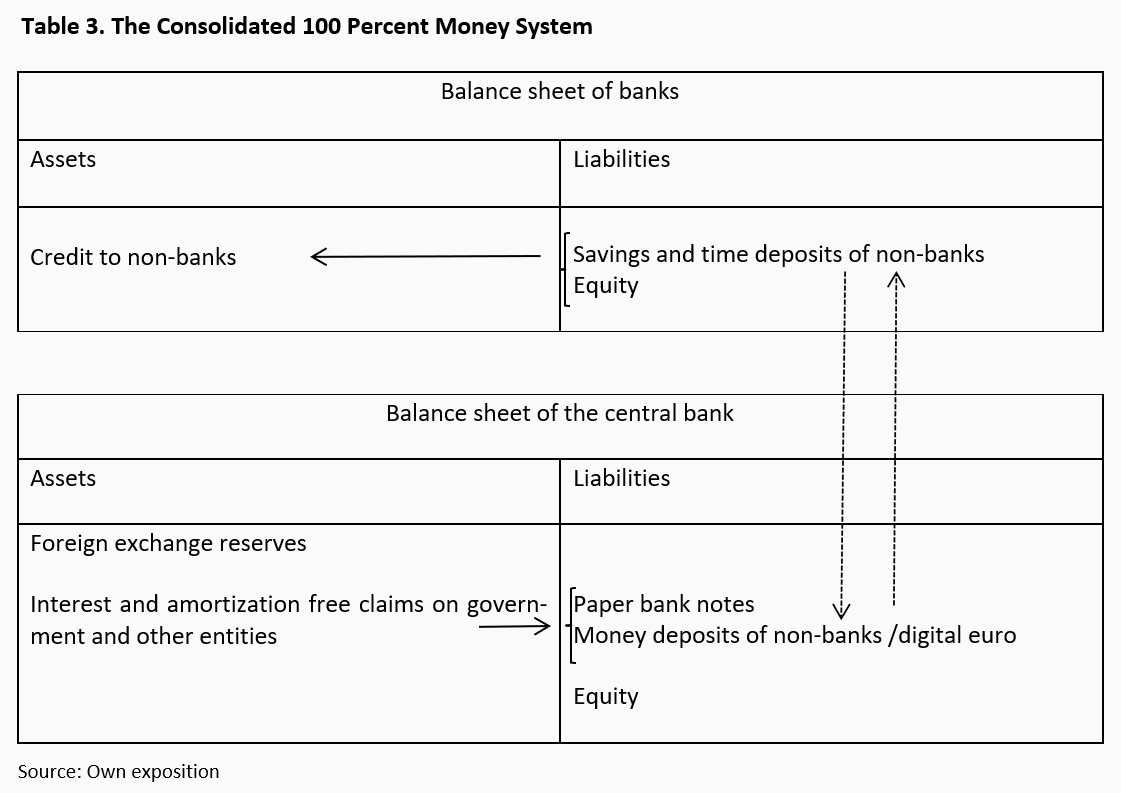

At the time of the Chicago Plan, when accounts were recorded in fat paper ledgers with pencils, retention of a two-tier system, with banks as the “front office” and the central bank as the “back office”, was regarded as essential. The central bank would have been unable to keep track of all accounts and transactions. Electronic banking has lifted this constraint. Hence, in a second step, the secure euro deposit could be consolidated on the ECB’s balance sheet. Reserve money holdings and money deposits are transferred from banks to the central bank. The reserve money holdings of banks cancel out against the reserve money liabilities on the balance sheet of the central bank, leaving it with money deposits of the non-bank public. The ECB could keep a central ledger for all accounts, or it could introduce a peer-to-peer transfer system using distributed ledger technology. The result is shown in Table 3.

In the latter case, the euro would become what the crypto world calls an “asset token”, backed solely by government bonds. Embedded in the token could be an algorithm stipulating the nature of its backing and rules for the creation of new tokens (see below). The algorithm would be tantamount to a digital watermark identifying the token as a valid digital euro (akin to the watermark in the paper banknotes). Entities tasked with proofing transfers of tokens in the DLT (so-called “nodes”) would only validate a transfer if the token under review was created according to the rules laid down in the algorithm. A token found in a proof of a transaction not to have been created according to the rules embedded in the algorithm would be treated as counterfeit money. Only the European Central Bank (and not the commercial banks as in the credit money system) would be responsible for issuing digital euro tokens. For users accustomed to paper money, the ECB would of course exchange digital euros at parity into bank notes.

Initially, non-bank debtors still have obligations towards banks created in the credit money system through credit contracts. When debtors repay debt in bank money, both the banks’ claims on them and their money deposit holdings diminish. When repayments are made in 100%-money / digital euros, the banks change them into bank money and cancel both the deposits and the corresponding credits against each other. With the increasing use of 100%-money / digital euros for payments, savings, and loans, fiat-credit is repaid, and bank money destroyed. The money system moves gradually from fiat-credit to the 100%-money / digital euro system.

A rule-based increase in the money supply

Any future increase in the money supply would take the form of additional purchases of government bonds by the ECB. Purchases would have to be decided independently of political influence and with a long-term perspective. For instance, in the spirit of Milton Friedman’s “k-percent rule”, growth of the digital euro money supply could be geared by the algorithm defining the digital coin to the long-term growth rate of real gross domestic product (the growth potential) of the euro area economy as estimated by a certain international organization (e.g., the OECD). Revisions of the potential growth rate summing up to more than 0.5% in either direction could lead to an adjustment of the algorithm in a hard fork, provided that the network participants, the “nodes”, reach consensus for the adjustment. Thus, money would no longer be an instrument for discretionary economic policy. But in view of the destabilizing role monetary policy has played in the credit money system, this would hardly be a disadvantage.

In the fiat credit money system, the central bank supplies and accepts central bank money used by banks to facilitate inter-bank deposit transfers. Thus, the rates the central bank charges on loans and gives on deposits of central bank money determine short-term interest rates. From the latter, longer-term bank lending rates are derived. As pointed out by Ludwig von Mises and Friedrich von Hayek, the central bank does not know the short-term interest rate consistent with non-inflationary economic activity and may set the rate too low or too high.7

If the rate is set too low, new demand for credit is induced to fund additional investment while money holders are discouraged from saving. Aggregate demand rises above supply, inducing inflation. When the central bank raises short-term rates in response, projects begun at lower rates become unprofitable and must be abandoned. Initiation of new projects declines. The economic upswing turns into a downswing. Inflation falls, the central bank lowers interest rates again, and a new cycle begins. Hence, the interest rate policy of the central bank is a key driver of the investment and credit cycle.

Since active monetary policy would be redundant when money supply is increased according to a clearly specified rule by an algorithm, the ECB would become superfluous. In its stead, a digital euro association (consisting of the authorized validators of transactions, the nodes) would act as a system administrator. Theoretically, inflation or deflation could result from a too large or too low rate of expansion of the money supply. However, any error would be kept small by the possibility to adjust for larger changes of the potential growth rate of the economy as described above. In any event, errors would not unleash the dynamics that led to the frequent boom-bust credit cycles in the fiat credit money system over the last half century.

To avoid money creation for fiscal policy purposes (as proposed by Modern Monetary Theory), governments would be obliged to distribute the money they receive from the bond purchases by the central bank directly to their citizens as a "money dividend", instead of budgeting it as revenue to fund expenditures. Any government violating this obligation (stipulated in the algorithm embedded in the euro) would be found to engage in distributing counterfeit money, automatically no longer qualify for bond sales to the ECB, and hence not receive new money for distribution to its citizens.

This notwithstanding, fiscal policy could of course be used for stabilization policy if a government would find this useful. However, any decision to stimulate the economy by running budget deficits would have to be consistent with long-term debt sustainability. Violation of the constraint set by debt sustainability would eventually lead to government bankruptcy as there would be no central bank able to act as a lender of last resort to the government. However, the consequences of a government default would be more manageable than in the existing credit money system because the forced write-off of bank credit would no longer destroy the money, which credit extension had created.

Seigniorage

Seigniorage is created by the increase in the money stock and (in the fiat credit money system) the difference between lending and deposit rates of the central bank and banks. In the fiat credit money system seigniorage income comes from both sources. Income from the first source accrues to the central bank, while income from the second source is shared between the banks and the central bank. In the digital euro model, seigniorage net of system operating costs comes from the first source only and is distributed to the wallet holders.8 Private money issuers have an incentive to attract users. Hence, they will also promise to pay dividends out of seigniorage income to account holders and use the rest to cover their costs and make a profit. Currency competition between the CBDC and private issuers ensures that profits remain contained and a sizeable part of seigniorage goes in the form of dividends to users.

Banks as intermediators

Commercial banks would now have to broker their customers' savings deposits in the form of digital euros to investors, and interest rates would be determined by the demand for funds for investment purposes and the supply of money savings in the credit market. Banks would resemble an investment fund whose assets are protected against first losses by an equity cushion. Savers could choose the bank that suits them according to their preferences for returns and first loss protection.

For instance, a bank with an equity cushion of 8 percent could offer a higher return at a higher risk due to its higher leverage than, say, a bank with an equity cushion of 16 percent. The equity cushion would absorb both credit risk and risk from maturity transformation. For savers to be able to make an informed choice, banks would be required to disclose the average duration of their assets and liabilities, and (quality) rating of their credit portfolio.

Commercial banks could of course continue to create their bank money through lending. But there would be no state guarantee for conversion at parity into digital euros. Thus, bank money would be equivalent to the most senior bank obligations with zero maturity. In contrast to digital euro holdings, these bank obligations could carry interest to compensate holders for the risks associated with the extended credits and maturity transformation of banks, which could lead to declines of euro prices of the obligations.

Freedom for interest

The central bank would no longer manipulate interest rates to control banks' credit money creation. Instead, interest rates would be determined in the market for loanable funds. The theoretically risk-free yield curve would emerge from market clearing interest rates for each duration according to the respective rates of return on safe investments on offer and the time preferences of savers. The actual yield curve would reflect the risk-free curve and banks’ risk premiums on credit and maturity transformations. Correspondingly, the yield curve in markets for credit securities would only reflect the risk-free curve and credit spreads as maturity transformations do not happen there.

Let’s have a closer look at how this would work. In a 100%-money system the market rate of interest would converge towards the rate of time preference of savers, the originary interest rate, to which the natural interest rate (reflecting the marginal return on capital) would adjust. Assume that depositor A concludes a savings contract with his bank, in which he renounces the use of a certain sum of digital euros for a certain time. He may do so when the bank offers him a rate of interest for borrowing his digital euros, which meets his rate of time preference (the originary rate). The bank now finds an investor B who borrows the digital euros, because he expects to use them to generate a return above the borrowing rate. Investor B buys capital goods from supplier C with the digital euros. C in turn concludes a savings contract like A and hands the digital euros over to the bank. The latter finds another investor D who borrows them again to buy capital goods, in order to generate a return above the borrowing rate.

The volume of credit and savings expands until the expected rate of return of investors meets the lending rate of the banks, which is determined by the time preference of savers and their lending margin. The marginal return on capital—or the “natural rate”—is now equal to the time preference of savers (the originary rate) plus the lending margin of the banks. Should the natural rate for any reason drop below the lending rate of the banks, investment would cease, and the capital stock would shrink due to depreciation until the marginal product of capital would rise again and restore the natural rate to the lending rate of the banks. Thus, rather than following boom-bust cycles as in the credit money system, investment would grow on a steady path. Economic growth would be higher, because the misallocation of capital created in boom-bust cycles would be avoided.

An end to the sovereign-bank doom loop

Since government debt would be used for backing money with an asset, digitalization of the euro offers the possibility to reduce the debt of the euro states and end the sovereign-bank doom loop. Recall that the central bank buys government bonds to create the central bank money for the secure deposit, which can be transferred peer-to-peer with DLT. Thus, bonds on the central bank’s balance sheet to back the outstanding (digital) central bank money stock are permanently taken out of the market.

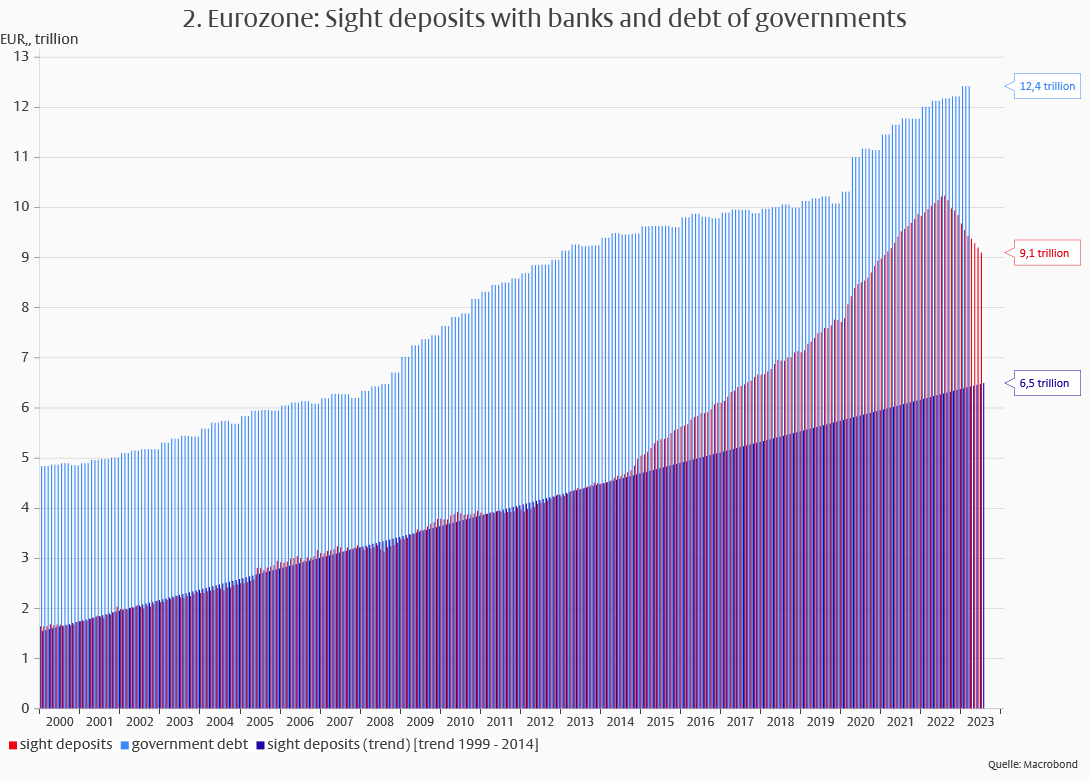

In the first quarter of 2023, euro area government debt amounted to EUR 12 trillion or 88 percent of GDP (Chart 2). At that time, sight deposits amounted to EUR 9.4 trillion. However, a part of these deposits was created by asset purchases of the ECB since 2015 and hence contributed to the monetary overhang built up with this policy. This overhang will have to be eliminated (through credit contraction) to return to price stability and should therefore not be exchanged into 100% digital euros. To determine the stock of sight deposits consistent with price stability, we extrapolated the trend estimated from 1999 to 2014. The trend value for June 2023 was 6.5 trillion euro (about 46 percent of GDP). This is the amount that needs to be backed by government bonds on the ECB’s balance sheet.

The ECB has bought a large part of this amount in its asset purchase programs and created reserve money against it. Banks could use these reserves (held in their ECB accounts) to back 100% digital euros. And they could sell the remaining part of government bonds needed to back 100% digital euros from their existing holdings or acquisitions in the market.9

Since the stock of bonds is permanently required as cover for the 100% digital euros, repayment would be suspended. Moreover, as interest income from the bonds would be returned to governments anyway, coupons could be reset to zero (by exchanging interest bearing bonds against zero coupon bonds with unlimited duration). With a zero coupon and infinite maturity, the bonds would cease to count as government debt outstanding in the market. Hence, outstanding market debt of euro area governments would fall to EUR 5.5 trillion or about 39 percent of GDP.

Soft currency reform instead of hard default

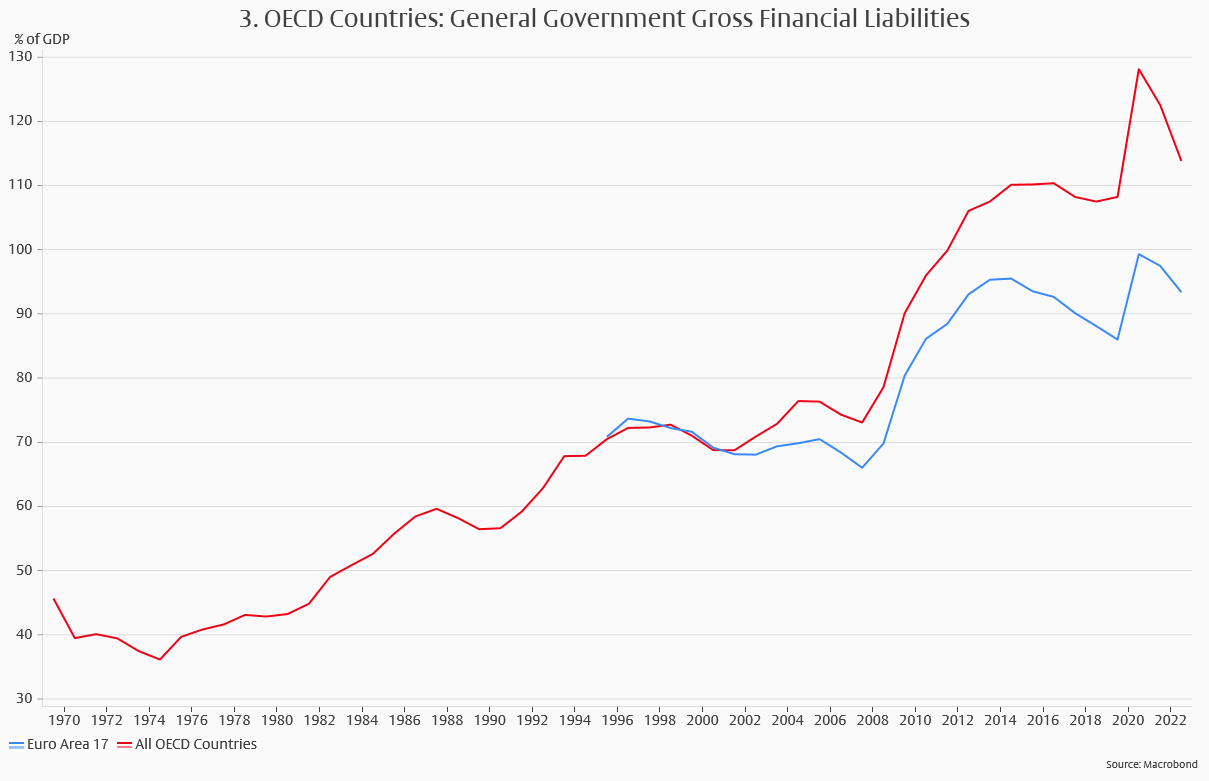

In response to interest rates falling to historical lows, industrial countries have accumulated government debt of historical proportions (Chart 3). The eurozone is no exception. With interest rates returning to more normal levels, the debt burden is hardly sustainable. History shows that there are three ways to reduce excessive debt: (1) repayment; (2) default; and (3) indirect default through monetary financing accompanied by debasement of the currency, often followed by currency reform. In the course of history, repayment was more the exception than the rule, default often the only available way when a government had no control over the currency in which it borrowed, and indirect default more the rule than the exception.10

Government defaults or debasement of the currency would most likely destroy European Monetary Union. But the introduction of a digital euro offers an alternative to these outcomes. Although it achieves the same result as a currency reform, it is not accompanied by an outright default of the government and the associated economic upheaval.

If the euro fails, Europe must not fail

“If the euro fails, Europe fails”, declared Chancellor Angela Merkel on 19 May 2010 in the German Bundestag. However, tying the fate of the European Union to its rickety currency was downright reckless.

The European Economic Community and later Union brought peace and prosperity to a continent ravaged by brutal wars in the first half of the last century. Its major achievements included reconciliation between the former “archenemies” France and Germany – which led to the reconciliation of Germany with its other earlier war enemies –, customs union, and the single European market. While these achievements were reached on politically and economically sound ground, the launch of European Monetary Union was flawed.

When EMU was contemplated, most economists and many politicians agreed that a state currency within the fiat credit money system was unviable without a state, i.e., a political union. Therefore, efforts were made to create a political union in parallel with monetary union. However, the project of a political European union failed. Monetary union was launched, nonetheless. Initially, the euro benefitted from falling interest rates. But when interest rates rose again, triggering the Great Financial Crisis of 2007-2008, the euro was about to fall apart. Only the replacement of cheap private by cheap public credit and renewed easing of monetary policy could save it.

As the period of record low interest rates is over and credit is becoming more expensive again, it is only a matter of time when the euro will come under stress again. But this time, it will not be possible to save it again by pushing interest rates back to their previous lows. Hence, without systemic reform, two paths appear likely in the future: (1) The ECB will keep domestic interest rates below the level consistent with price stability and below foreign interest rates. The result would be a debasement of the currency and the emergence of alternative, private means for exchange and the store of value. (2) Highly indebted countries can roll over maturing debt only at rising penalty interest rates. Debt service becomes politically unsustainable, they exit EMU, and the euro breaks apart.

New Deal for the euro

Digitalization could be combined with a “New Deal for the euro” to safe the common currency (and avoid the disastrous consequences of its failure): The fiscally conservative northern countries with lower debt levels would agree to the one-off monetization of old debt on the balance sheet of the ECB for the creation of the 100%-digital euro. In return, the higher indebted southern countries would accept that after the one-off monetization of their old debts, a renewed monetization of national debts would be impossible. They would get a larger debt reduction, if bonds were bought by the ECB so as to reduce the debt ratios of each euro state to same level.11 But as all euro member countries would benefit by getting new room for prudent fiscal policy, the northern countries could afford to be generous.

With the rules for establishing the digital euro and augmenting the money supply embedded in the algorithm of the digital euro, it would be impossible for governments to monetize future debt. Governments in payment difficulties could opt for bankruptcy and debt restructuring or, if desired, issue their own fiscal money (as was contemplated by the governments of Greece and Italy at various points in time).12 But any money issued in breach of the contract and called euro would simply be counterfeit money (like issuing counterfeit central bank notes).

Currency competition

Europeans use American platform companies to communicate and shop on the Internet. They use the US Dollar for a large part of their international payments. A digital euro would significantly reduce Europe’s dependence on the US Dollar as a means for international payments and create a formidable competitor for other global digital currencies likely to emerge in the medium term future. All global users would benefit when several currencies compete for their favour.

At present, competition among money issuers takes place primarily in the international foreign exchange markets for sovereign currencies. At the national level, sovereign currencies have been established as monopoly currencies by law and are only rarely challenged by competitors. Only Bitcoin has emerged as a challenger but is used on a larger scale only in countries where trust in sovereign currencies is low. However, with electronic payment systems facilitating currency management, currency competition may well move to the national level, unless governments ban private currencies by law.

In a paper published in 1976, Friedrich von Hayek proposed a regime of currency competition.13 In his analysis, conducted during the first part of the inflationary 1970s, Hayek diagnosed a permanent abuse of the government prerogative for money creation and regarded inflation as largely generated by governments. The government secures the monopoly for money issuance to bolsters its power. The elevation of money to legal tender primarily serves the purpose to allow the government to interfere in private contracts and to change the means of payment established there to its advantage, if opportune. Hayek saw a return to a commodity money order, e.g., in the form of the gold standard, only as a second-best solution, because money is also created there by a monopoly (though the hands of government are more tied there).

Optimal money can only emerge from free competition of private issuers. To this end, Hayek proposed that certain banks issue money, the purchasing power of which they hold stable against a basket of raw commodities. Money with stable purchasing power will be preferred against money with declining purchasing power so that the best money is found through competition. When currencies compete among each other (and banks not issuing currencies back deposits in full with reserves), there is no need for a central bank. Because competition secures an adequate supply of money, monetary policy is redundant. And because money is not created as private debt money, there is no need for a lender of last resort.

Some Austrian economists have criticized Hayek’s idea of currency competition because they regard it as a violation of Ludwig von Mises’ “regression theorem”. This stipulates that no money can come into existence that did not exist as a commodity before. Moreover, they claim that information costs are higher in a competitive system than in a monopolistic one. However, neither argument is convincing. Bitcoin moved from a computer program to a currency when a vendor accepted it as payment for a pizza on 21 May 2010. No commodity preceded it. And with internet based new information technology information costs have come down substantially.

Others have argued that competition would soon be followed by a private oligopoly or monopoly of money issuance as good money drives out bad. They disregard, however, that markets are never in static equilibria but always in dynamic disequilibria. Thus, as soon as excessive seigniorage income accrues to a money issuer, an entrepreneurial opportunity is created for another issuer to enter the market and compete for the income. Money issuers cannot go bankrupt as they do not need to take on debt. But they can, of course, debase their money. This is more likely in the case of a sovereign issuer who can declare his money as legal tender than in the case of a private issuer who must seek to satisfy his customers.

As the example of Bitcoin shows, no special legal framework is needed for private “active” money (which is an asset and not lent into existence by a public-private partnership like in the fiat credit money system). Bitcoin emerged as trust in the legally established currencies fell during the financial crisis. But like any other asset, private money would of course need to be protected by legally enforceable property rights. Moreover, to create a level playing field for currency competition, the principle of entrepreneurial freedom and liability would also need to be applied in the financial sector. Thus, bailouts of ailing financial institutions are banned under state subsidy rules so that moral hazard created by implicit or explicit promises of bailouts is eliminated.

Would investment suffer?

The great economist Joseph Schumpeter praised the fiat credit money system for its ability to supply entrepreneurs with new money created by extending credit to them without having to collect savings beforehand. Would the digital euro model deprive entrepreneurs of new money because banks no longer can create it through credit extension? We do not think so.

When Schumpeter wrote about credit funded investment, capital markets were less developed than today. Banks played the key role for the funding of companies’ investment projects. Today, capital markets have become much more important. Companies use them for debt and equity funding. Start-ups can get risk capital through venture capital funds. Banks securitize loans or create certificates of deposits and sell them in the capital markets. In the digital euro model banks would continue to do all this, and fund loans they wish to keep on their balance sheet by collecting digital euro deposits in the same way they attract credit money deposits from other banks today.

Thus, it is a fallacy to believe that a 100%-money system would lead to an accelerated disintermediation of banks and deprive investors of bank credit. The 100%-money system would only deprive the banks of their ability to create new money through credit extension but leave their role as intermediaries between savers and investors intact. For investors there would no material change to their ability to obtain credit.

Governments tend to be hostile towards monies they cannot control for fear of loss of the use of money creation as a financing instrument. Banks share their aversion against non-credit monies because of the loss of their seigniorage income from bank money creation. However, the strongest resistance is likely to come from central bankers who would lose power and lucrative jobs in a 100% digital money system. According to Parkinson’s Law, a bureaucracy always expands, and never contracts. Hence, for the ECB to be unwound, which would be consistent with the move to a 100% digital euro, Parkinson’s Law would have to be suspended. That would certainly be no easy feat.

Moreover, central bankers’ defense of their benefice is helped by campaigners against “state money” and the abolition of paper banknotes. Some of the opponents of digital money see the real risk for an even bigger abuse of money by governments and their central banks for narrow political purposes. But instead of looking for ways to use the new technology to end the present abuse, they support the prevention of monetary reform. In their view, a digital central bank currency opens the door to the abolition of paper money and the opportunity for the state to monitor private payments with digital currencies and introduce negative interest rates as a stealth tax.

To support their argument, some point to China, where they expect the digital Yuan to strengthen government surveillance of citizens. Others promote conspiratorial theories.14 Some also erroneously argue that in a 100%-money regime the central bank needs to replace private banks as an allocator of credit (which misses the fact that 100%-money is not created through private credit extension).

Although many of these campaigners profess to be libertarians, they ignore that monetary reform opens the door to competition between state and private money. Thus, they strengthen the status-quo of the public-private partnership of money creation in a monopolistic setting, which they say they oppose. By the same token, campaigners against the abolition of paper money ignore the inevitable trend towards electronic payments with bank money. They fail to comprehend that a digital central bank currency could even guarantee the continued existence of paper money as a necessary non-electronic backup for electronic money.

The freedom to choose between paper and digital money issued by the state central bank and digital money issued by private entities is the best insurance against government meddling with money. But by rejecting a digital euro the campaigners allow the authorities to introduce digital money in limited quantities to protect the public-private partnership of money creation under state authority.

Overcoming the multiple resistance would be a formidable task. In fact, as long as the system keeps working somehow, the resistance is most likely insurmountable. As history (notably in Germany) has vividly demonstrated, chances for a system change only emerge during times of severe distress as in the course of a money crisis. In view of the deficits in the euro architecture and the return of financial stress with the resurrection of inflation, a money crisis is a distinct possibility in the medium-term future. It is for this possibility that we discuss here (again) the digital euro model we already presented many times before. When the euro fails, policy makers should not again be able to excuse their myopia, like they did in the Great Financial Crisis, by saying that nobody saw it coming and nobody had thought about how to deal with it.

References

Bindseil, Ulrich. Tiered CBDC and the financial system. ECB Working Paper Series No 2351 / January 2020

Fisher, Irving. 100% Money. Adelphi (N.Y.) 1935.

Hayek, F. A. Denationalisation of Money. Institute of Economic Affairs. London, 1976.

Mayer, Thomas. Austrian Economics, Money and Finance. Routledge 2019.

Mayer, Thomas. Long-Term Strategies to Reduce Public Debt from a Historical Perspective. The Economists’ Voice, 2023, vol. 20, issue 1

Footnotes

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch SE. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch SE remains solely with Flossbach von Storch SE. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch SE.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch SE.

© 2024 Flossbach von Storch. All rights reserved.

Thomas Mayer

Managing Director and Founder

Before starting the institute, Thomas Mayer was Chief Economist of Deutsche Bank and in that role headed Deutsche Bank Research, the bank’s economic think-tank. He also worked for Goldman Sachs, Salomon Brothers, the International Monetary Fund and the Institute for the World Economy in Kiel. Since 2003 and 2015, he is CFA Charterholder and honorary professor at University of Witten-Herdecke, respectively.

All articles by Thomas Mayer