29.01.2024 - Studies

Behavioural psychology shows: Satisfactory capital investment depends on the individual's financial goals and risk appetite. Good asset management takes this into account and provides customised solutions. And investors can also contribute to wealth accumulation through their behaviour.

Sometimes everything seems like a big misunderstanding: on the one hand, there is the German saver with his savings account, knowing full well that his interest will be eaten up by inflation. On the other hand, there is the financial sector with its wide range of fund products, which are often perceived as "speculation", especially with high equity stakes.1 Good asset management tries to close this gap. It analyses the (financial) wishes and needs of the individual and offers investment strategies to achieve them.

This study attempts to draw a blueprint for the investment of private investors from the perspective of behavioural science. We develop a two-stage investment process: the assets are first mentally divided into two separate sub-accounts, so-called mental accounts. Different investment strategies are derived from the different objectives of the accounts. This contradicts academic portfolio theory, according to which portfolios should be viewed holistically and optimised with a view to expected returns and fluctuations in returns. Although this portfolio theory has proven to be unsuitable in practice, it is still taught and consulted by some investors.

Instead of considering expected returns and return fluctuations calculated from financial data as objectively valid for all investors, questionnaires in the portfolio theory of behavioural science offer investors the opportunity to subjectively explore their own goals and risk preferences and find suitable investment strategies. Establishing routines helps to stick to a chosen investment strategy even in turbulent times. The findings provide practical tips for capital investment.

In 1979, a fundamental work in behavioural science by Amos Tversky and Daniel Kahnemann sparked a discussion about the criteria people use to make financial decisions. It begins with the following experiment: test subjects could choose whether they would rather receive 2,400 Israeli pounds, 80 per cent of a monthly median net family income, as a gift or take part in a game of chance. In the game of chance, they had a 33 per cent probability of receiving £2,500 and a 66 per cent probability of receiving £2,400. With a probability of one per cent, they received nothing. Although the expected value of the gamble of £2,409 is higher than the certain payout of £2,400, only one in five took the bet.2

In 1997, Hersh Shefrin and Meir Statman took up the observations of Kahnemann and Tversky and combined them with the "mental accounting" introduced by Richard Thaler in 1985.3 As an alternative to the classic "mean-variance theory", they formulated a "behavioural portfolio theory": according to the theory, capital investment is mentally divided into two pots, which are viewed separately by the investor. The two pots are "protection from poverty", i.e. protection from poverty or maintaining the standard of living, and "prospect for riches", i.e. the prospect of wealth or wealth accumulation. The objectives and therefore the investment strategies of these two pots complement each other. Statman compares the two "mental accounts" with layers of a pyramid of needs.

The lower tier forms the basis for maintaining the standard of living. Here, security and liquidity considerations ensure a conservative or less volatile investment. Above this is the growth-orientated part of the assets or the money with which one tries to become "rich". Depending on what wealth means to the individual, the individual chooses more volatile investments for the chance to achieve their goals.4

Empirical examples support this theoretical categorisation: at Santa Clara University, two savings plans that are simultaneously saved in by the same employees have different risk profiles. Apparently, one plan is used to secure the standard of living and one to accumulate assets. Unit-linked guarantee products, which combine a minimum interest rate on contributions with the possibility of additional gains from equity funds, are particularly popular in German life insurance. These products are known as hybrid products and are presented in sales as "the best of both worlds". They attempt to combine investment in both layers.

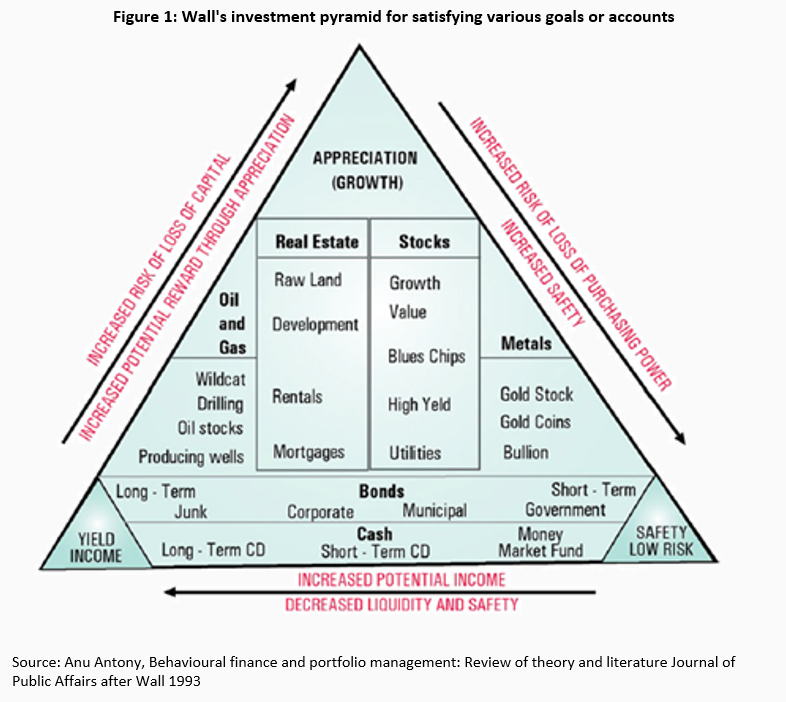

Moreover, layered pyramids have a long history in financial advice. As early as 1952, a guide to fund investment listed the various investment options depending on the layer.5 Figure 1 shows an illustration from 1993.

The system is always similar: bonds and cash form the basis for securing the standard of living. Above this are large, stable, high-dividend companies and, at the top, equities with growth potential.

However, splitting into two accounts can also be more exotic: the case of Mavis Wanczyk is known from America. The former nurse secured her standard of living by investing in her employer's pension scheme. Her aim was to be able to retire early by building up her assets. To achieve this, she played the lottery with the remaining funds. At the age of 53, she won 758 million dollars and quit.

Parallel to the discussion about mental accounts, the understanding of utility functions was refined. In a 1992 paper, Tversky and Kahnemann estimated the change in utility of financial decisions based on a reference point with a power function defined section by section. Two findings were central: Firstly, losses of a certain amount are approximately twice as painful as gains of the same amount. This phenomenon is called loss aversion.6 Secondly, doubling the gain does not double the benefit. The benefit only increases by around 85 per cent. This is called diminishing marginal utility. Similarly, doubling a loss does not double the weight.7

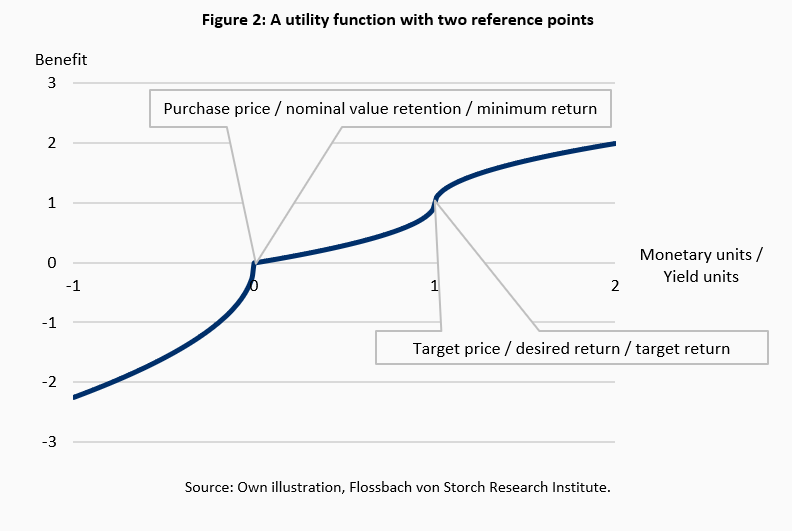

Shefrin and Statman presented a fundamental further development in 1997. They added another reference point to the theory. According to their aforementioned Behavioural Portfolio Theory, financial securities have a purchase price and an aspiration level. The utility function then consists of three sections.8

Prices below the purchase price are perceived as a loss. The utility function is convex in this area. There is an affinity for risk. Between a safe price increase and a risky 50/50 bet, which either gives the investor double the price increase or none at all, the investor decides in favour of the risky 50/50 bet. The function between the purchase price and the level of demand is still convex, but the gradient is smaller. The additional benefit of a risky alternative compared to a safe one is lower than below the purchase price. Investors take fewer risks in this area in order to get closer to their aspiration level. Above the aspiration level, price increases are no longer as valuable as below it. Risk aversion prevails. The function is concave, i.e. the investor favours safe capital growth over a 50/50 bet, which either gives him double the growth or none at all. If an investor's goal is nominal value preservation, the purchase price and the target price coincide. In this case, the classic two-part utility function of Kahnemann and Tversky arises.9

So far, we have seen two things: Firstly, people mentally divide their assets into several pots, with which they pursue different goals and therefore different investment strategies. Secondly, the benefits of investment strategies can be mapped using utility functions that revolve around two reference points depending on the investment objective.

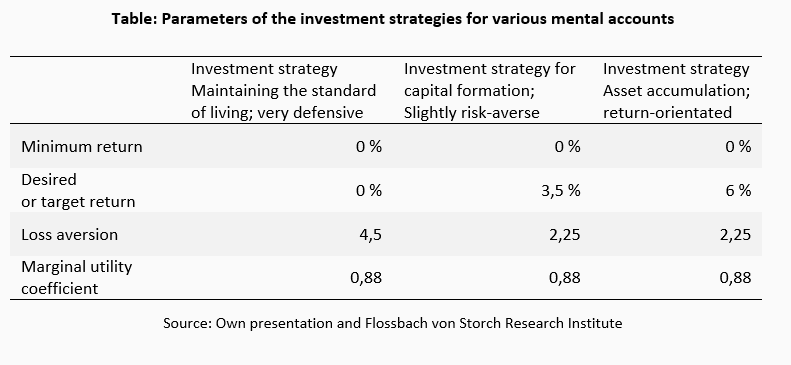

In the following, we concretise these considerations using an example. We calculate the benefit-maximising mix of equities and a fixed-income alternative for three different investment strategies. We distinguish between a defensive, a slightly risk-averse and a more return-orientated and even more risk-averse risk profile. The very defensive investment strategy fits the mental account "Maintaining the standard of living". The two strategies with higher expected returns can be seen as two possible forms of investment in the "Wealth accumulation" mental account. Depending on their own goals, investors will find themselves in one of the two strategies.

Instead of using price levels, we operate below with annual expected returns. The purchase price corresponds to nominal value retention, i.e. an expected minimum return of zero per cent. The target price or the target or desired return differs according to the mental account and personal investment objectives. The desired return can be thought of as the return that the investor associates with thoughts such as "I will achieve my financial goals with this return" or "this return is sufficient for me".

The idea of thinking in terms of sufficient rather than maximum returns is supported by practice and science. Howard Marks, co-chairman of the investment firm Oaktree, recently stated in an interview with the Financial Times:

"One of the concepts I always argue for is the "higher-enough" return. People unthinkingly assume you want as much as you can get. But thinking rationally, isn't there some point that you have enough, and you shouldn't take more risk than what you need to get there?"10

And Nobel Prize winner Herbert Simon coined the term "to satisfy", a neologism made up of "to satisfy" and "to suffice". The term stands for decisions made by individuals that are not optimal but satisfy their own needs sufficiently.11

According to a recent representative survey, one in six investors in Germany is driven by the thought of "at least not making a loss". For these investors, securing their standard of living takes centre stage; wealth accumulation plays a subordinate role. For the "preservation of the standard of living" strategy, we therefore assume that the desired return is zero per cent and corresponds to nominal value preservation.12 With return assumptions of 3.5 per cent and six per cent, the return expectations of the remaining investors in the study are divided into thirds. As approximations for the desired returns in the two "wealth accumulation" strategies, we therefore choose a desired return of 3.5 per cent for the slightly risk-averse alternative and a desired return of six per cent for the return-oriented strategy.

We choose the parameters of the utility functions of the three model investors on the basis of Kahnemann and Tversky's estimates.13 For the "wealth accumulation" strategies, we use the mean loss aversion of 2.25 found there. For "maintaining the standard of living", we assume a loss aversion of 4.5, which is twice as high

The expected returns on the investment in shares and the risk-free investment are still missing. In two out of four years, an annual return of six per cent is expected on the stock market. Every four years, a loss of minus 5 per cent or a gain of 15 per cent should statistically occur within one year. The slight asymmetry takes account of the fact that the annual median return of share indices is generally below the mean return. Similar to the current interest rate on 10-year German government bonds and the interest on deposits at some direct banks, the risk-free alternative should pay interest at three per cent per year. The mix between equities and risk-free investments can be varied in ten per cent increments.

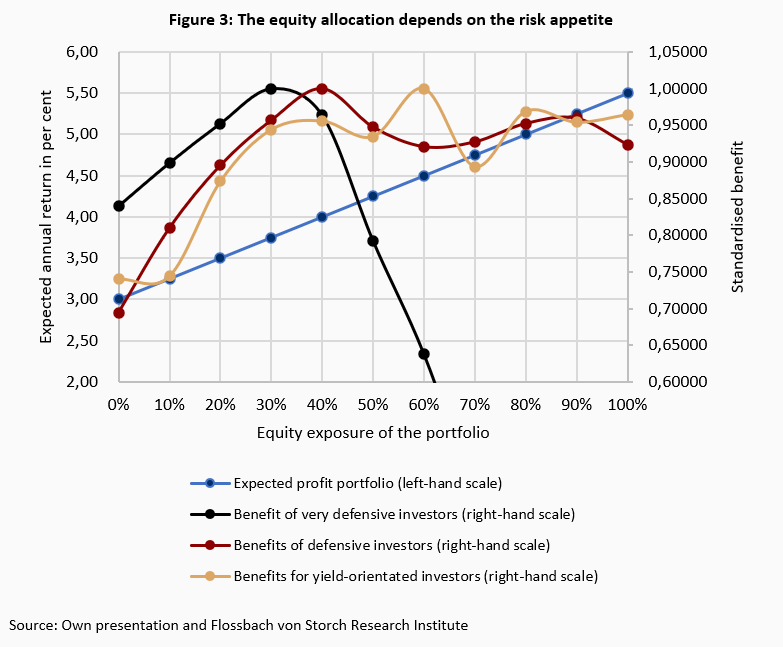

Based on these assumptions, an equity allocation of 100 per cent delivers the highest expected return - 5.5 per cent. However, the equity ratios of the three investment strategies that maximise the expected benefit deviate from this.

The best way to secure your standard of living is with a mix of 30 per cent equities and 70 per cent risk-free investments. Higher equity ratios reduce the benefit in the adverse equity scenario due to the strong loss aversion. With 30 per cent equities, the average return of 3.75 per cent is significantly higher than the targeted wealth preservation. And even in years in which equities generate losses, the overall result remains just positive due to the high risk-free interest rates. The high risk-free interest rates make it possible to invest three out of ten euros in shares despite a pronounced need for security.

For comparison: with a risk-free interest rate of one per cent, only one in five euros would be invested in shares with the same investment preferences; with an interest rate of 0.5 per cent, it is only one in ten. A lower risk-free interest rate can only compensate for small losses from shares. Loss aversion comes into play even with lower equity ratios.

For slightly risk-averse wealth creation, investors should invest two out of every five euros in shares. This satisfies their higher risk appetite below the desired return of 3.5 per cent. To do this, he utilises his loss aversion, which is only half as pronounced as in the defensive strategy. Higher equity ratios bring him less benefit, as he is risk-averse for returns above 3.5 per cent.

The return-orientated strategy reaches its maximum benefit when six out of ten euros are invested in equities. Initially, an increase in the equity ratio ensures that the risk affinity is satisfied. From a ratio of six to four between equities and safe investments, loss aversion and risk aversion gain the upper hand.

Different investment objectives require different investment strategies. The equity allocation that maximises the benefit differs depending on the resulting risk profile. Assuming that the strategies are intended for long-term investing and that the actual return therefore corresponds to the expected return, the investor forgoes returns. In the case of the "maintaining the standard of living" strategy, the difference to the maximum possible return is 1.75 percentage points. In return, there is an emotional benefit: the reassuring feeling of a secure portfolio and - in the case of the very defensive strategy - the satisfaction of the feeling of "not making a loss".14 The return foregone from the choice of strategy can be described as a "peace of mind" premium.

In order to determine your own investment strategy, you should be clear about your (financial) goals. When asked, many people first mention "financial security". However, the ideas behind this can vary greatly. For some, security means not having to worry about their savings even in financial crises, while for others it means building up a pension, which requires a certain minimum return. Another goal of many people is to be able to provide for and support their own family, especially their children. If I want to finance my child's education or studies, for example, there are immediate indications of the investment horizon, savings rates and necessary returns.

Questionnaires are a way of researching your own goals, comparing them with your own risk-bearing capacity and translating them into a concrete investment strategy. A good questionnaire combines (financial) goals and the required returns with the amount of (temporary) losses that the individual can tolerate. The recommendation of a risky strategy should be avoided if there is a lack of personal experience or a small financial cushion. Therefore, before recommending high equity ratios, it is essential to enquire about previous personal experience and the size of other mental accounts. A "cold start" with a pure equity portfolio with high volatility can lead to sleepless nights, early selling and lasting bad experiences.

Good questionnaires take into account possible anomalies in user behaviour such as exaggerated self-confidence - known in behavioural science as "overconfidence bias". Depending on the parameters initially asked, subsequent questions adapt dynamically. Ideally, the user implicitly finds his personal benefit function(s) with a questionnaire and receives an explicit recommendation for the investment. Sound advice from experts naturally fulfils the same purpose.

On the investor side, honesty is essential for success. Questionnaires are not exams. A higher risk appetite is not the same as a higher score. More is not better. Rather, the recommended risk class should match your own feelings. More risk should make you "uneasy", less should create the feeling of aiming for a "too low return level" for your own goals.

After the initial assessment, the goals only need to be reviewed every few years or after significant personal experiences. You may start a family or your children may leave home. You inherit, change jobs or become self-employed. The experiences you have had and your changed life situation have an impact on your financial situation. If decisions that I felt comfortable with five years ago make me feel uneasy today, I need to reassess them.

As we have seen, a well-chosen investment strategy may fall short of the maximum possible long-term return. However, a strategy that is theoretically more profitable but does not suit the individual will, in case of doubt, generate an even poorer return as it is not maintained. An inappropriately chosen investment strategy creates the risk of "losing one's nerve". Rapid shifts in the portfolio and frequent "in and out" of the market produce transaction costs instead of increases in value. Charlie Munger, Warren Buffett's recently deceased partner, hits the nail on the head:

"The big money is not in the buying or selling, but in the waiting."15

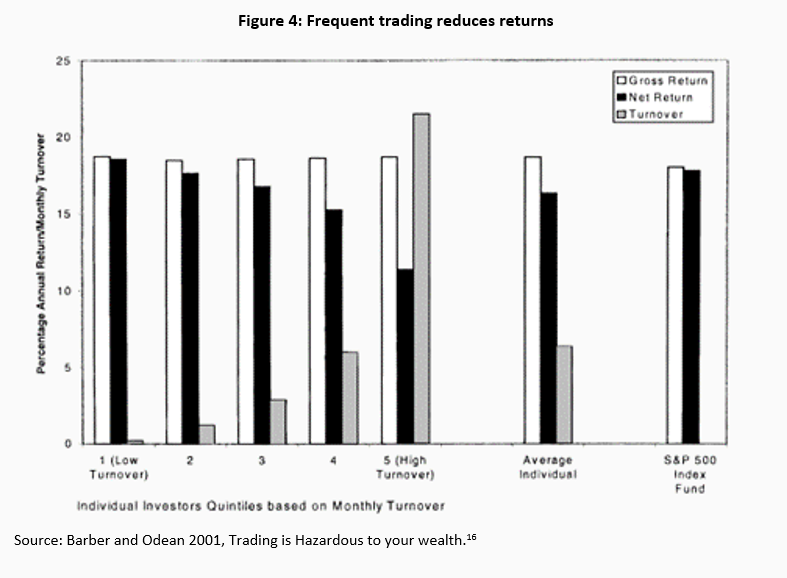

An empirical study from the year 2000 confirms the quote and quantifies the loss. Researchers Brad Barber and Terrance Odean found a switching premium of 30 cents per one euro of return among private investors who traded individual shares excessively. This is due to the transaction costs incurred, which are not offset by higher returns. The investor therefore pays a "switching premium". The more the investor trades, the higher the premium.

Applied to our example calculations above with the various strategies, this means that excessive trading generates a switching premium of up to 1.65 percentage points: with full investment in equities and excessive trading, the expected return falls from 5.5 per cent to 3.85 per cent. Excessive traders therefore have a lower expected return than investors who only have an equity allocation of 40 per cent and do not reallocate. Even in the slightly risk-averse asset accumulation strategy we have presented, the "peace of mind" premium of 1.5 per cent is lower than the switching premium. Ergo: It is better to choose a suitable strategy once and stick with it instead of taking on too much and gradually losing returns by constantly switching investments.

What are the reasons for excessive behaviour? A 2018 study by Mey Wang, Thuy Phan and Oliver Rieger identified the underlying character traits: Overconfidence, impatience and (uncritically) following investment advice from friends and family.17 The characteristics are reflected in three well-known phenomena of behavioural science for financial markets: "Overconfidence", "Disposition Effect" and "Fear of Missing Out".

Despite the generally recognised fact that only a few achieve above-average returns on the capital market, investors who trade excessively increasingly believe that they belong to this small group. They believe that they have more information about the market than the majority of other investors or that they have above-average forecasting skills.18 They attribute their successes excessively to their own ability. They suffer from overconfidence.

Impatience or the "disposition effect" manifests itself in premature profit-taking. The investor enjoys the good feeling of a quick trading success. However, as the actual loss aversion is greater than originally thought, losses are sat out. The reluctance to realise the loss means that loss-making investments are held longer than justified. The result is increased trading volume with poorer results.

Well-intentioned advice from friends causes many investors to fear missing out on a unique opportunity, the "Fear of Missing Out". You invest in the supposedly hot investment tip from your personal environment to avoid looking like an outsider. Otherwise you may end up turning down well-intentioned advice and missing out on a unique opportunity. Better to reallocate quickly. However, the predicted excess return often fails to materialise. The transaction costs remain.

How can investors protect themselves from "overtrading"? Or to put it positively: How do you develop into a goal-orientated, long-term investor?19 Trading apps and smartphones allow you to continuously monitor the prices of your investments. With just a few "clicks", you can follow impulses and rebalance your portfolio. However, wishing for a return to the days when prices could only be obtained from the newspaper and orders had to be faxed is futile and, what's more, not expedient: "Overtrading" existed even before the first iPhone, as the above study by Barber and Odean shows. In addition, the innovations mentioned have made access to the capital market easier for many people and reduced transaction costs - a good thing. So how do we deal with the existing environment?

We have already discussed the importance of a well-chosen investment strategy. However, using willpower and cognitive abilities alone to stay on course is beyond us. We can only utilise these two powerful tools of the human mind to a very limited extent. This is why, despite all our cognitive abilities, we are also creatures of habit. We cope with around half of our everyday lives without consciously thinking about decisions. We use routines and habits.20 If a routine determines our actions, all our willpower is useless because it is not used at all. Routines are triggered automatically and are then controlled by the subconscious.

Based on a study by the University of Würzburg, psychologist Wendy Wood therefore comes to the conclusion that people with higher self-control are not characterised by greater willpower and are therefore better at resisting affective situations. Rather, they use their cognitive abilities to establish routines that minimise the occurrence of sudden temptations and impulses.21 It is therefore important to use cognitive abilities to replace bad habits with good ones. This is an insight that was already suggested by Wolfgang Goethe:

"It's not enough to know, you also have to apply. It's not enough to want to, you also have to do."22

How do we create routines that give us the resilience we need when short-term price setbacks trigger fear or supposedly "hot" tips circulate in the press or in our private lives and - despite knowing better - we are in danger of instinctively falling into behaviour that could damage our returns? We should create an environment that prevents impulsive behaviour and replaces harmful routines with those that make us long-term investors. Wood identifies four basic pillars for the formation of good routines - context, friction, reward and repetition.23

A stable and supportive context: Does reviewing my portfolio have a fixed place in my everyday life and how is the review triggered? It's better to devote half an hour to your portfolio on a regular basis, e.g. on the first Tuesday of every month, than every time your friends tell you about their latest investment tips in the pub. You can keep going to the pub and discussing investments with friends. However, you need to be aware of what actions this may trigger and adapt them accordingly. As an alternative to impulsively switching investments after receiving tips, you could, for example, get into the habit of picking up a book on the financial markets and reading up on the recommended asset.

Secondly, control via friction. Desired behaviour must be easy and undesired behaviour difficult. In other words, I keep investment information and access data for my portfolio neatly organised in a fixed place for my monthly portfolio check so that I have all the necessary documents to hand without having to think. My trading app, on the other hand, should not be able to be opened by facial recognition, but only with manual password entry. I should set up two-factor authentication for trades, which means I need to add another device. Ideally, you should use a stationary PC for this, which has to be booted up first.

The design of asset management apps can make excessive trading even more difficult: For example, after placing a sell order, a message could appear stating that high trading frequency generally reduces investment success. The message concludes with the question of whether the order should really be placed. This double confirmation is familiar from messages that appear before closing unsaved documents in word processing programmes - and protects us from hectic situations by interrupting our routine. The content of the sell order message can vary depending on the holding period and size of the trade so that it does not wear out.

In addition, current information on the capital markets could be placed more prominently on the app screen than the "trading button". This redirects attention and prioritises information gathering instead of trading. What successful user guidance looks like can be observed on websites and in other applications of large technology companies such as Amazon, Google, Meta or Netflix. It is crucial for investors to use a tool that primarily supports their goals and not those of the app provider.

Rewards form the third pillar. In order for behaviour to become automatic, our brain needs positive feedback on the behaviour we perform. After completing a portfolio check, it is therefore best to treat yourself to something. For example, go to the cinema or out for a good meal with family or friends. Pay for it with the trading fees you have saved.

And fourthly: repeat, repeat, repeat. It takes time for behaviour to become a routine. Simple everyday routines, such as eating an apple every day, feel "automatic" after just over two months. More complex behaviours with several individual components are more difficult to automate and require more time. Exactly how much depends on the routine. But if a routine is skipped once, fortunately it doesn't start all over again the next time. Even a certain regularity helps to change behaviour step by step.

However, if you fall back into old patterns more frequently, it is advisable to think again about the context you have set yourself. Occasional hasty trades are only temporary setbacks on the way to becoming a goal-orientated investor. However, if this behaviour continues or recurs, it is worth considering why it is still too easy to trade. Perhaps you no longer had a book to hand to redirect your attention?

People divide their investments into several pots, so-called mental accounts. They pursue different goals with the pots and treat them separately. What successful investment in the individual pots means depends on your own (financial) goals and is different for everyone. It is therefore important to find out what your personal goals are and to harmonise them with your personal risk tolerance. Questionnaires or personal advice can help with this.

Yield-maximising investment strategies are only the best if the individual can stick with them. Otherwise, the "switching premium" paid for excessive trading exceeds the "peace of mind" premium paid for satisfaction with the investment decision.

The right routines help investors to stick to their strategy and promote targeted, long-term investing. You should therefore use your cognitive abilities to create good routines.

1 M. Kleinheyer: Money illusion despite inflation worries - Flossbach von Storch Research Institute

2 Kahnemann and Tversky: Prospect Theory: An Analysis of Decision under Risk, 1979, Problem 1.

3 H. Shefrin, M. Statman: Behavioural Portfolio Theory, 1997 and R. Thaler: Mental Accounting and Consumer Choice (ufl.edu), 1985.

4 M. Statman: Behavioural Finance - The second generation, CFA Institute Research Foundation, 2019.

5 M. Statman: Behavioural Finance - The second generation, CFA Institute Research Foundation, 2019, page 93.

6 Whether loss aversion applies universally is controversial. This is questioned for smaller amounts. However, the phenomenon is recognised for large amounts, such as those involved in savings processes. See also: E. Yechiam: Acceptable losses, 2018.

7 D. Kahnemann and A. Tversky: Advances in Prospect Theory, page 311.

8 Incidentally, Shefrin and Statman's observation goes back to Harry Markowitz, the founder of the classic mean-variance portfolio theory.

9 H. Shefrin, M. Statman: Behavioural Portfolio Theory, 1997.

10 Financial Times, R. Armstrong: Unhedged - Investing after easy money.

11 H. Simon: Rational Choice and the Structure of the Environment, 1956.

12 M. Kleinheyer: Money illusion despite inflation worries - Flossbach von Storch Research Institute

13 A. Tversky, D. Kahnemann: Advances in Prospect Theory: Cumulative Representation of Uncertainty, page 311.

14 M. Statman: Behavioural Finance - The Second Generation, 2019, page xiv.

16 B. Barber, T. Odean: Trading is hazardous to your wealth: the common stock investment performance of individual investors, 2000.

17 T. Phan, M. Rieger, M. Wang: What leads to overtrading and under-diversification? Surveyevidence from retail investors in an emerging market , 2018.

18 For a discussion, see M. Statman: Behavioural Finance - The Second Generation, 2019, Chapter 9.

19 We do not want to take this away from people who trade because they enjoy it. This study is limited to analysing how private investors can achieve their financial goals in the long term.

20 W. Wood: Good Habits, Bad Habits, 2019 and [4]Can Brain Science Help Us Break Bad Habits? | The New Yorker

21 W. Wood: Good Habits, Bad Habits, 2019 & W. Hofmann, R. Baumeister, G. Förster, K. Vohs: Everyday Temptations: An Experience Sampling Study of Desire, Conflict, and Self-Control, 2012.

22 Johann Wolfgang von Goethe - Wikiquote

23 W. Wood: Good Habits, Bad Habits, 2019.

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch SE. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch SE remains solely with Flossbach von Storch SE. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch SE.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch SE.

© 2024 Flossbach von Storch. All rights reserved.

Sven Ebert

Senior Research Analyst

At the Institute since 2022. The actuary and actuary DAV holds a doctorate in probability calculation from the Karlsruhe Institute of Technology. He has been a lecturer at the Technical University of Cologne for several years and is active in the DAV actuary training programme of the German Actuarial Academy. His topics include old-age provision and behavioural finance.

All articles by Sven Ebert