17.03.2020 - Studies

The coronavirus pandemic is likely to cause a global recession. Italy is one – if not the – most exposed larger country to both the pandemic and recession.

The government has already responded to the crisis with a substantial package of fiscal measures, amounting currently (March 17) to EUR 25 billion. The increase of the public debt ratio as a result of measures to fight the pandemic and of the recession will sooner or later require an intense effort to ensure the solvency of the Italian state.

Corona crisis will leave deep financial scares

On March 5, the Italian government adopted an initial EUR 6.3 billion package of supportive measures for the economy. Upon the expectation that “economic activity [being] liable to fall more deeply and broadly in the near term”, the initial package was further extended on March 11 to EUR 25 billion, bringing the overall authorization to 1.1% of GDP. However, the latter figure will most probably increase both as a result of the fight against the pandemic and of recession. An economic downturn is now inevitable.

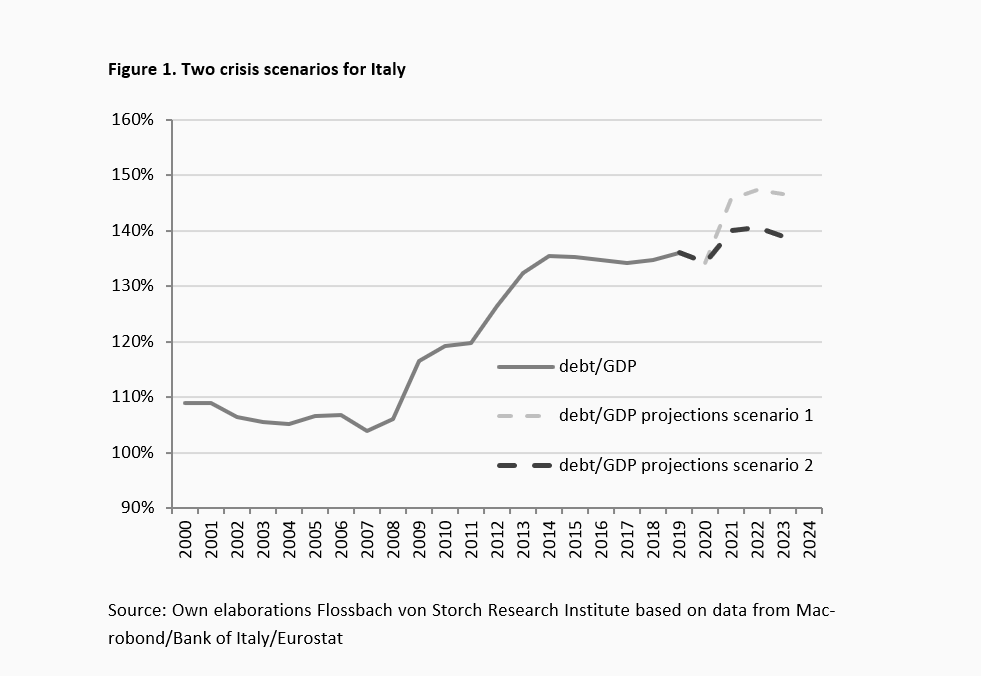

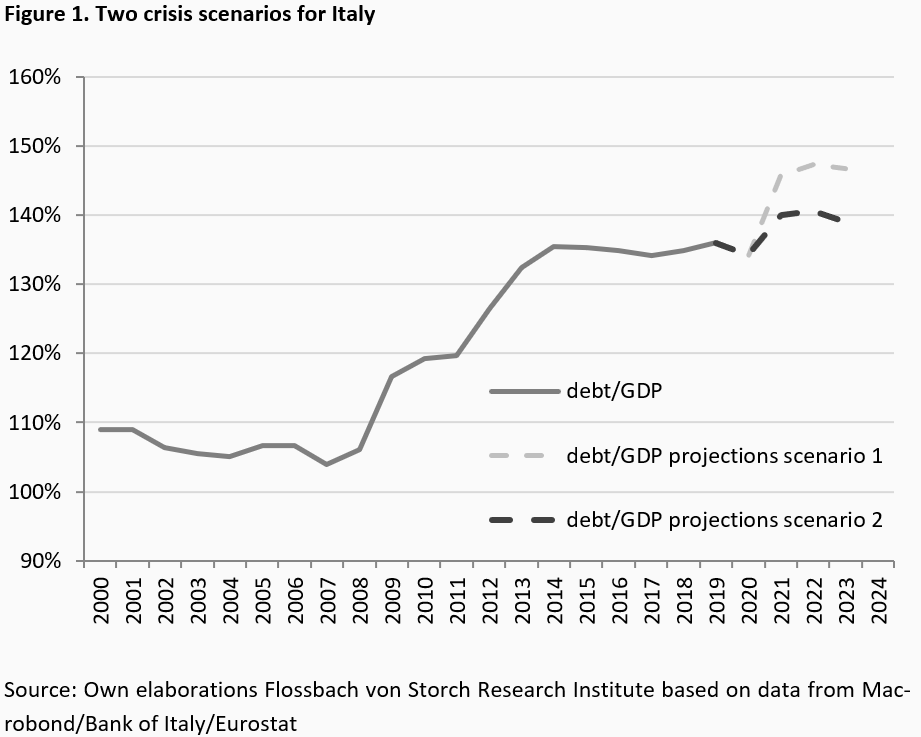

Figure 1 shows a simulation of the consequences of an economic crisis for general government gross debt. We simulate two scenarios:

Scenario 1: Severe economic crisis

To design this scenario, we take as a reference the economic impact of the 2009-2010 recession. Although the two events are not fully comparable, the economic crisis following the Great Financial Crisis should be a sufficiently good reference to approximate for an economic damage caused by an unexpected event.

Growth of nominal GDP fell by almost 7 percentage points in 2009, by almost 1 percentage points in 2010 and by 0.8 percentage points in 2011 compared with the average nominal GDP growth in the three years preceding the event. Back then, this led to a nominal GDP growth of -3.7% in 2009, +2.2% in 2010 and +2.3% in 2011. However, given a much lower average growth of nominal GDP (1.8%) in the period 2017-2019, a full-blown current crisis could result in nominal GDP growth of perhaps -5% in 2020, +0.8% in 2021 and +1% in 2022. Afterwards, we assume that nominal growth normalizes at levels from before the crisis (i.e. 1.8%).

The impact of the coronavirus pandemic and recession create a deficit in the primary balance. Assuming a similar effect as in the economic crisis 2009-2010, the primary balance could worsen by almost 3 percentage points of GDP in 2020 and by 2.2 percentage points in 2021 compared with the average over the three years preceding the event. Accordingly, this would lead to a primary balance of -1.6% of GDP in 2020 and -0.9% in 2021. For the period 2022-2024 we assume a normalization of public finances, leading to an average annual primary surplus of 1.3%. This would correspond to an average primary surplus generated in Italy over the period 2017-2019.

Finally, we assume that turbulence around the corona crisis and the economic downturn would lead to an increase of the average interest rate on the Italian government bonds. This assumption is the most difficult to make, compared with the previous two, given that the general context of the interest rates changed much after the Great Financial Crisis. Back then, the interest rates were at more normal levels and the European Central Bank had significantly larger room of maneuver to cut interest rates to contain rising risk premia on government debt titles and to answer to a looming economic crisis. Today, this room of maneuver is much more contained. At the same time, the participation of the ECB in the market for sovereign bonds through its extensive asset purchase programs accelerated the convergence of interest rates within the euro area to the low levels close to the interest rates on the German government bonds. This implies that the reaction of interest rates on the Italian government bonds is expected to be much more contained compared to the previous crisis. Accordingly, we assume that the average interest rate in Italy would increase in 2020 by a moderate 1 percentage point over the average levels experienced in 2019. This would correspond to an increase of the average interest rate to 1.9% in 2020. For the period 2021-2024, we assume that the average interest rate would go down slightly to 1.4%. This would accommodate for the hypothesis that a further increase in the public debt burden would require a slightly higher risk premium on the Italian government bonds.

Based on this scenario, the public debt ratio in Italy would increase from the current 136% of GDP to a maximum of 147.4% in 2022 and would then gradually decrease to 146.7% in 2023 and 145% in 2024.

Scenario 2: Economic crisis “light”

Provided that the economic impact from the COVID-19 crisis would be less severe and that extensive monetary and fiscal stimulus would contain the downturn and gradually bring the interest rates levels to the pre-crisis period, the trajectory of the public debt in Italy would be milder compared with the previous scenario. However, this is contingent on two crucial assumptions, namely, that 1) the impact on the nominal GDP growth over the three years 2020-2022 would be only half as severe as under scenario 1 and the growth rate of nominal GDP would return to the pre-crisis normal of 1.8% afterwards, and 2) the average interest rate would increase by only 0.5 percentage point in 2020, converging gradually afterwards to the pre-crisis level of 0.9% in 2024.

Under this scenario, the government debt ratio would increase to reach a peak of 140.6% in 2022. The debt ratio would then gradually decline to 136.4% in 2024.

Conclusion

Taking as reference the economic crisis from the recent past, this note analyses the likely fiscal consequences of the current corona crisis. Even a mild economic recession would bring the debt-to-GDP ratio in Italy to over 140% in the next two years. A recession twice as severe – which unfortunately seems more likely - would result in an increase of debt ratio by more than 10 percentage points, bringing it to 147% in 2022. Moreover, based on the experience of the last few decades, the rise of public debt in Italy is more likely to be permanent rather than only temporary.

With a debt ratio heading towards 150% of GDP it is unlikely that Italy will be able to access financial markets without external help. Given the limited funding capacity of the European Stability Mechanism, it seems inevitable that the European Central Bank will have to assume the role of the lender of last resort to the Italian government.

16.04.2019 - Macroeconomics

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch SE. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch SE remains solely with Flossbach von Storch SE. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch SE.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch SE.

© 2024 Flossbach von Storch. All rights reserved.

Agnieszka Gehringer

Senior Research Analyst

Agnieszka Gehringer joined the institute in 2015. She studied economics at the University of Rome “La Sapienza” and later earned a PhD in economics of complexity at the University of Turin. Since November 2019 she has been a professor of Economics at the Cologne University of Applied Sciences and since July 2016 a lecturer at the University of Göttingen. She has published several articles in academic journals and is an advisor to the EU.

All articles by Agnieszka Gehringer