20.07.2022 - Comments

Many people may be familiar with the situation: Shortly before buying a share or an investment fund, you start to hesitate. Do you really want to tie up your money for so long? Perhaps it would be better to leave it on the bank account than to have it return only in the distant future. After these thoughts, the plan to invest is abandoned altogether.

In economics and psychology, this is known as time preference. People prefer to be in possession of a good today rather than having it in the future. The euro in the distant future simply has less utility than the euro one has in one's wallet here and now. It is therefore difficult to compare today's euro with the future one, let alone to set them off against each other.

In many situations, however, there is no way around comparing current and future payments. Is the price of a financial product appropriate for retirement planning? Do the expected future payouts compensate for today's sacrifice? Therefore, a framework is needed to make payments occurring at different points in time comparable with each other. In economics, this process is called discounting.

For discounting, one usually uses compound interest. If an investor has the same benefit from 100 euros today as from 110 euros in one year's time, her implicit discount rate is 10%, which describes her time preference.1 Once one has determined this discount rate, one can apply it to other cash flows to express today's utility in a euro amount. For example, if a pension product pays out 20,000 euros once in 30 years, this would have the same utility for the investor as the amount of 1,145 euros today.2 Therefore, the investor would not be willing to pay more than this price for the product in question.

The method described above, which uses compound interest to compare cash flows that occur at different points in time, is known as exponential discounting.3 It is the common practice for choosing between investment alternatives. It is intuitive, taken for granted and rarely questioned. Even the legislator requires the use of this calculation methodology in many cases, such as in risk management of investment funds.

Less known is that exponential discounting is just an assumption. Exponential discounting is not a given or even a law of nature. It is just one of many ways to deal with investors' time preferences. The reasoning goes back to the Expected Utility Model by Samuelson (1937).4 It is the first complete economic model, as it is known today, that can be used to measure the utility of investors' future cash flows in order to make investment choices based on them. The model makes few assumptions, such as a positive and constant time preference and time-consistent behaviour of individuals. The discounting in the model corresponds to the formula of compound interest and is mathematically easy to handle. These attributes contributed to the fact that exponential discounting has become the standard in economics and the financial industry.

However, the application of exponential discounting has serious flaws. It does not correspond to human action, or to the action which can be determined by observations and experiments.

The exponential formula of compound interest with constant time preference can hardly account for human impatience, which to some extent causes time preferences in the first place. Various experiments have shown this, the best known of which is the survey by Richard Thaler (1981).5 He showed that individuals do not possess a constant time preference. For in exchange for an amount of $15, subjects demanded $50 in one year or $100 in ten years. If exponential discounting is used to calculate the implicit discount rates, they are 233% for one year, but only 21% for 10 years.

The time consistency of action assumed in the Samuelson model can also be doubted. In one experiment, individuals were asked to choose between a direct payment of $100 or $110 the next day. The majority preferred the immediate lower payment. However, when offered a payment of $100 in 30 days or $110 in 31 days, the choice fell on the latter higher.6 This behaviour cannot be explained by an exponential discount function, because those who prefer the lower amount today would also have to assign a higher utility to the lower amount in 30 days under an exponential discount function, rather than waiting another day for the higher amount. Thus, there appears to be inconsistent behaviour over time.

The academic literature offers various alternatives to exponential discounting, which, however, also come with advantages and drawbacks. The work of Phelps & Pollak (1968) and Laibson (1997) exploits a simple trick by reducing all future payments to a fraction.7 Their empirical data suggest that investors value the utility of future cash flows at only 40% of the nominal amount. Additionally, to account for the time structure, they use the compound interest effect for discounting. This type of discounting is referred to as quasi hyperbolic discounting.

Another approach that can represent both impatience and time-inconsistent behaviour goes back to Ainslie (1975) and relates the respective expected cash flow to the time span.8 If a cash flow does not occur for another year, it must be halved to equal today's utility. If it is another year in the future, the amount of the payment is divided by three, and so on. This type of discounting is called hyperbolic discounting.

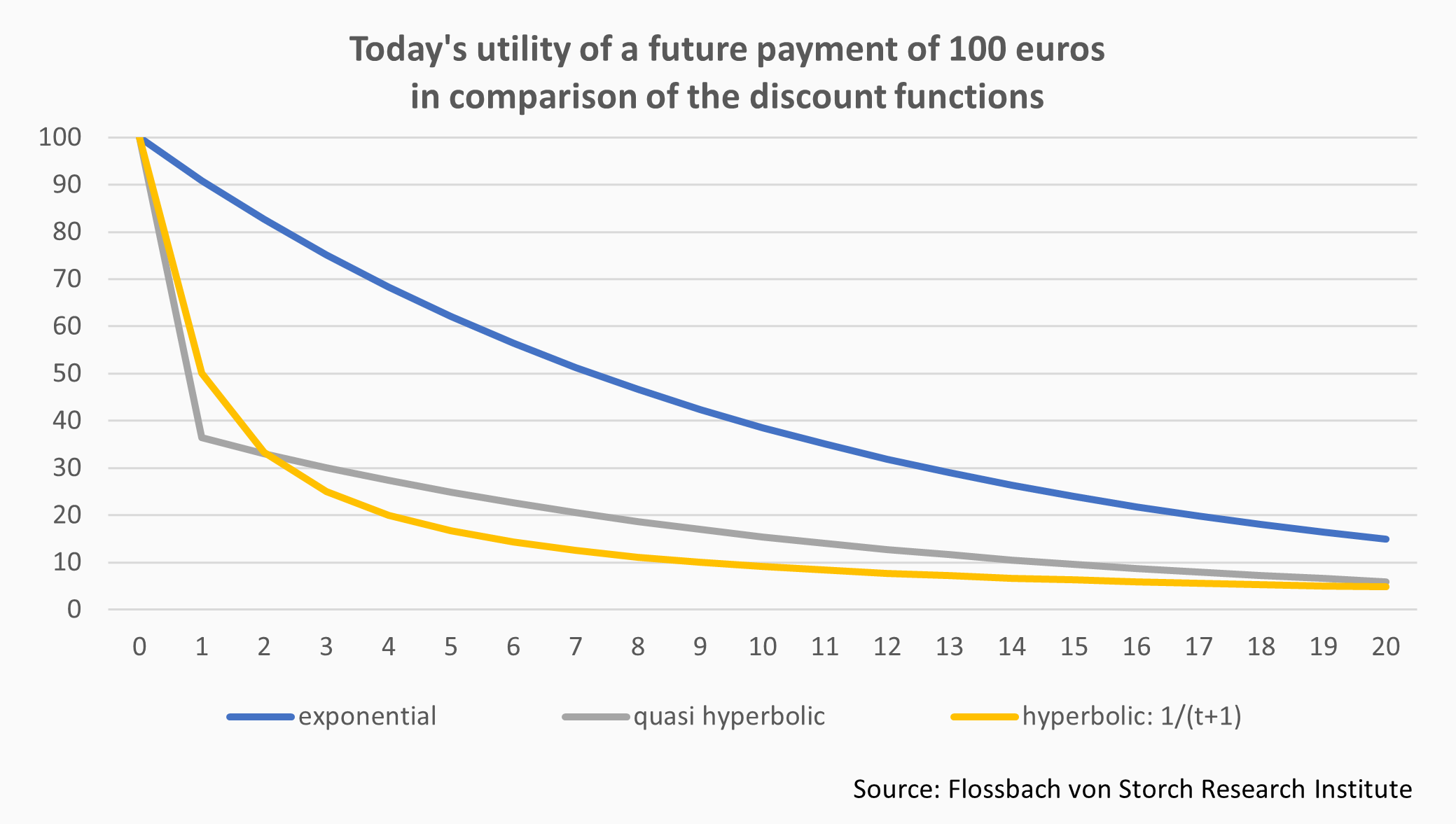

The graph shows todays utility of a future payment of 100 Euro, which is discounted using the three approaches discussed. It is striking that with the two hyperbolic discount functions the largest loss of utility occurs directly between today and the first year. In contrast, the utility drops only slowly with the exponential discount function.

However, the two hyperbolic approaches discussed are not free of empirical contradictions. Nevertheless, models with hyperbolic and quasi-hyperbolic discount functions offer interesting implications. They can explain why many investors do not use capital markets in the first place. They are not willing to tie up their money for short investment horizons because it does not correspond to their intrinsic concept of utility. For them, the prices of financial products such as stocks or mutual funds would have to be significantly lower given the expected payoffs.

One's own so-familiar hesitation to buy a stock or mutual fund can be attributed to one's time preference. Even if the prices of financial securities seem fair given their future payoffs, it may be because the valuation approaches prevailing in the capital markets simply do not match one's intrinsic utility.

1 Calculation: 100 € (1+10%) = 110 €.

2 Given the discount rate of 10%, we obtain: 20.000 Euro / (1+10%)30 = 1.145 Euro.

3 In general, the formula for exponential discounting of a future cash flow reads as follows: D(t) = 1 / (1+i)t, where i is the discount rate and t is the time at which the payment occurs..

4 Samuelson, P. A. (1937): “A Note on Measurement of Utility”, The Review of Economic Studies, 4(2), p. 155–161.

5 Thaler, R. (1981): „Some empirical evidence on dynamic inconsistency“, Economic Letters, 8(3), p. 201-207.

6 Fredrick, S., G. Loewenstein & T. O’Donoghue (2002): “Time Discounting and Time Preference: A Critical Review”, Journal of Economic Literature, 40(2), p. 351–401.

7 Phelps, E. und R. Pollak (1968): “On Second-Best National Saving and Game-Equilibrium Growth”, The Review of Economic Studies, 35(2), p. 185-199, and Laibson, D. (1997): “Golden eggs and hyperbolic discounting”, The Quarterly Journal of Economics, 112(2), p. 443-477.

8 Ainslie, G. (1975): “Specious Reward: A Behavioral Theory of Impulsiveness and Impulse Control”, Psychological Bulletin, 82(4), p. 463–496.

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch SE. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch SE remains solely with Flossbach von Storch SE. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch SE.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch SE.

© 2024 Flossbach von Storch. All rights reserved.