01.06.2023 - Studies

After three bankruptcies, the question is how stable the US regional banking sector is. And could the increased interest rates that triggered the problems not also lead to distortions at banks in Germany?

The list is long and its first entry happens to be a Friday the 13th. On that day in October 2000, the USA had to announce the first bank failure after the turn of the millennium. The Hawaii Department of Commerce and Consumer Affairs closed the doors of the Bank of Honolulu. The state deposit insurance agency Federal Deposit Insurance Corporation (FDIC) took over the administration of the insolvency and wound up the business of the failed financial institution.

For a long time, the FDIC was an abbreviation that hardly anyone outside the USA knew what to do with. But this has changed abruptly since the beginning of March this year, after the authority had to dispose of three US banks with quite a lot of noise.

Silicon Valley Bank, New York's Signature Bank and, at the beginning of May, San Francisco's First Republic Bank threw in the towel after customers withdrew deposits and it was not possible to cover them quickly by selling assets at market prices. The reason: the book values of the assets on the balance sheet, mostly bonds, did not match the market values, which fell in the opposite direction as interest rates rose.

One of the beneficiaries of the crisis of the US regional banks is the giant JP Morgan Chase, which has now been able to get hold of remaining First Republic funds on the cheap.

This now adorns memorial stone number 566 in the cemetery of dead US banks since 2000, next to the Carolina Federal Savings Bank, for example, or the Alabama Trust Bank. Yet not even the celebrities of the hereditary financial wizards are to be found there: defunct investment banks like Lehman Brothers have found their place in their own tomb of former large speculators, with Margin Call written above the entrance.

Banking giants such as Lehman could not withstand calls for additional funding when the markets wobbled. Here, too, sales of supposedly valuable assets on the market regularly yielded less than was necessary to prevent bankruptcy.

The next commemorative stones could already be pre-produced. So the recent bankruptcies are not only worrying customers on the US mainland, but are making waves far into the Pacific.

For example, as panic spread after the collapse of Silicon Valley Bank, stock exchanges temporarily halted trading in Bank of Hawaii shares, which had crashed by as much as 36 percent. Haiwaii News Now hastily reported in May that the banks on the four islands of the 50th state of the United States were actually much more conservative in their lending than their counterparts on the mainland. And, incidentally, their depositors are much more loyal. A crash like that of the Bank of Honolulu is therefore not to be feared, it was said semi-officially.

Now, of course, it is the first duty of politicians, board members and supervisors to reassure the common people. It has been a long time since there has been so much praise for the banks as in the past weeks.

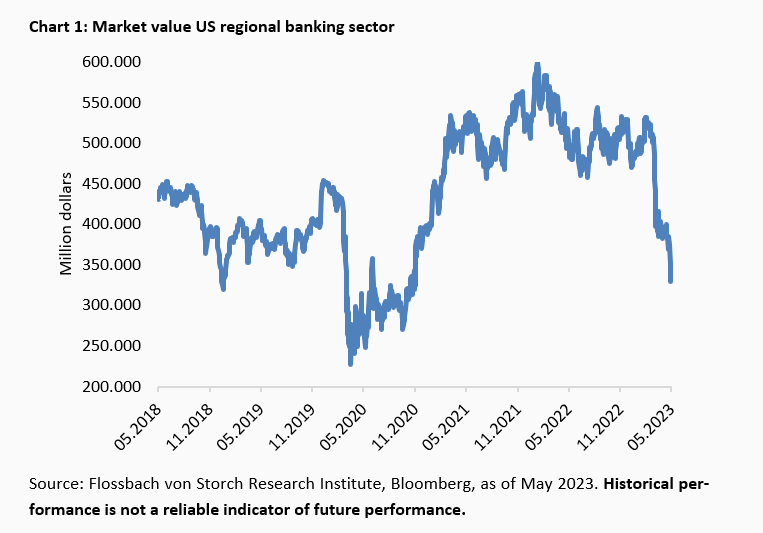

However, the calming pills did not work on the markets. For example, the market capitalisation of the US regional banking sector plunged 45 percent from its recent high at the beginning of 2022. Since the beginning of February alone, its value has plummeted by around 200 billion dollars over three months (chart 1).

Price losses on the stock market from not infrequently flighty investors are one thing. But how stable is the US regional banking sector really? And couldn't the increased interest rates, which triggered the problems, also lead to distortions at banks, savings banks and in the cooperative sector in Germany? In the worst case, are Swiss conditions threatening with a similarly spectacular rescue as recently at Credit Suisse, which, flanked by state and central bank guarantees in the triple-digit billions, had to take refuge with its competitor UBS?

In any case, smaller German institutions such as savings banks and Volksbanks already had to write off almost 13 billion euros on their securities portfolios last year because of the interest rate turnaround. However, they were able to cope with these losses thanks to reserves and capital cushions. And the German financial supervisory authority BaFin emphasises that, in contrast to the USA, there have been no emergency sales of bonds in Germany to plug liquidity gaps.

Be that as it may, it goes without saying that the banking sector is always about a lot of assets, debts and usually a little too little capital - despite all the regulation.

4.2 trillion dollars in assets, or on the other hand debt plus equity, is the size of the US regional banking sector, measured by 142 institutions from the S&P Regional Banking Index. By comparison, JP Morgan Chase alone had total assets of a good $3.7 trillion at last count. According to the latest data from the German Bundesbank, the German banking sector as a whole had total assets of 10.6 trillion euros at the end of March.

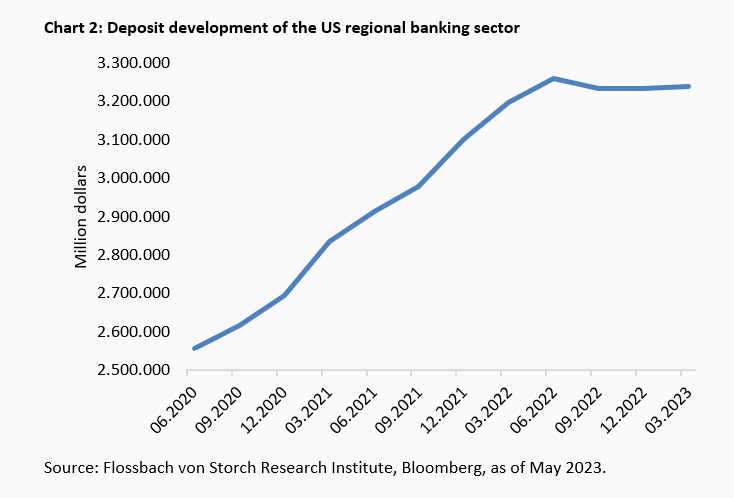

The crisis of the US regional banks was first reflected in stagnating deposits of a good 3.2 trillion dollars (chart 2).

Investors in the USA are increasingly putting new money into money market funds, which do not pay into the balance sheets of US regional banks, in the hope of a good return. This means that the institutions are missing an important source of funding for their growth.

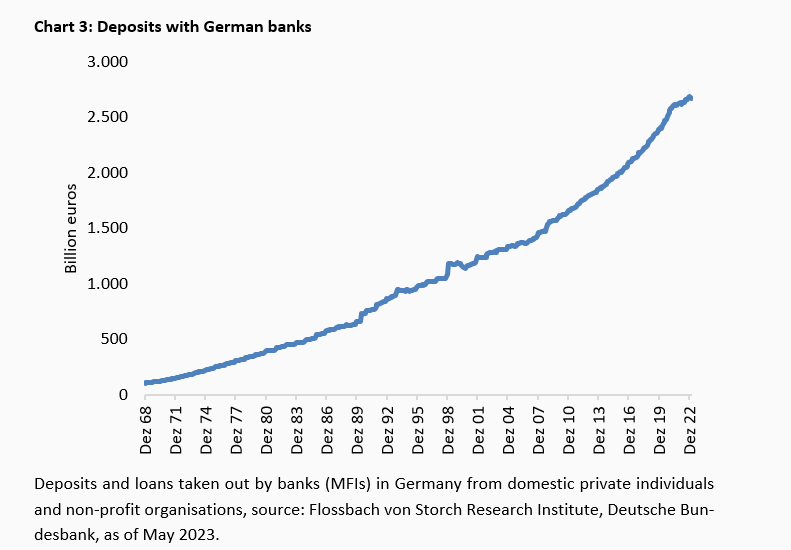

Deposits from private investors, traditionally a cheap financing pool, have also stagnated at German banks recently. From the record high of 2689 billion euros in December 2022, it most recently went down by 20 billion euros as of the end of March (chart 3).

By way of comparison, the top ten US banks - led by JP Morgan Chase - recently had almost three times the customer deposits of the US regional banks on their books, at $9.5 trillion. If you add the money parked with German banks by companies, savings books and savings bonds, you get a good 4.5 trillion euros in deposits as of the end of March 2023 (currently around 4.9 trillion dollars).

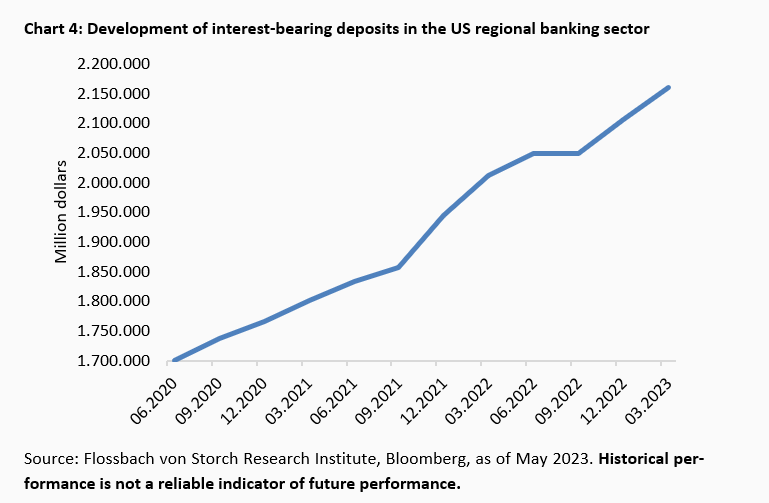

The interest rate turnaround has consequences for all banks. For example, US regional institutions have to pay interest on more and more deposits in absolute terms (chart 4).

However, the ratio of interest-bearing to non-interest-bearing deposits has remained constant over the past years at about 2:1.

This is also reflected in the balance of interest expenditure and interest income. Since the US regional banks are apparently still managing to invest and lend out customer funds at significantly higher interest rates, the interest margin is crumbling somewhat, but remains at a high level (chart 5).

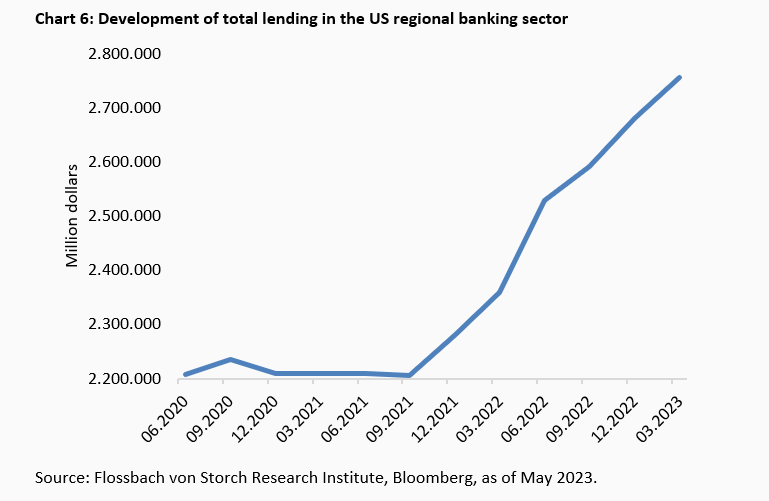

The liquidity glut of the Corona years is showing its dark side in the USA. The US regional banks, for example, massively expanded their lending business as a result (chart 6).

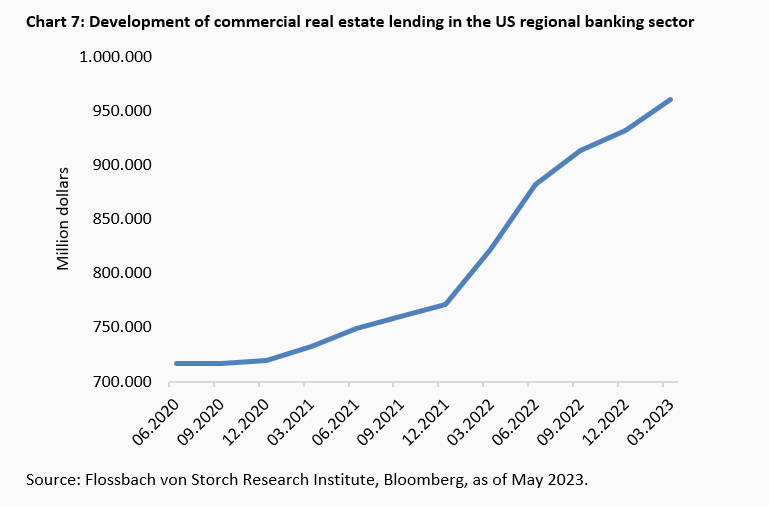

Traditionally, loans for the commercial real estate sector play an important role, and have experienced another powerful boost in the last two years (chart 7).

About 80 percent of all bank loans for commercial real estate in the US come from regional banks, Goldman Sachs estimates.

And commercial property prices fell in the first quarter of this year for the first time since the financial crisis more than a decade ago. This is shown by Moody's Analytics' so-called repeat sales index. JP Morgan Chase chief Jamie Dimon warned as recently as the end of May of a further downturn in US commercial real estate, the market size of which is estimated at $20 trillion.

One indication of the crisis is that Blackstone, the largest US commercial real estate financier, has been struggling with billions of dollars in outflows from its largest fund, worth 125 billion dollars, for half a year. Blackstone has since limited withdrawals from it.

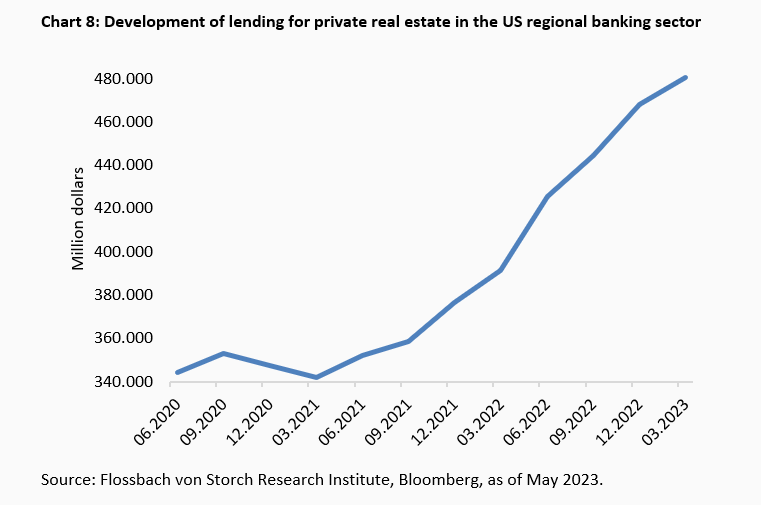

Since the summer of 2021, the stock of loans for the purchase of homes and flats by private individuals at US regional banks has also grown considerably, with an increase of more than one-third (chart 8).

Here, prices have fallen rapidly recently: in April, prices for the typical single-family house were 15 percent below their October high (median). One decisive reason is the long-term mortgage interest rates, which have risen to over seven percent.

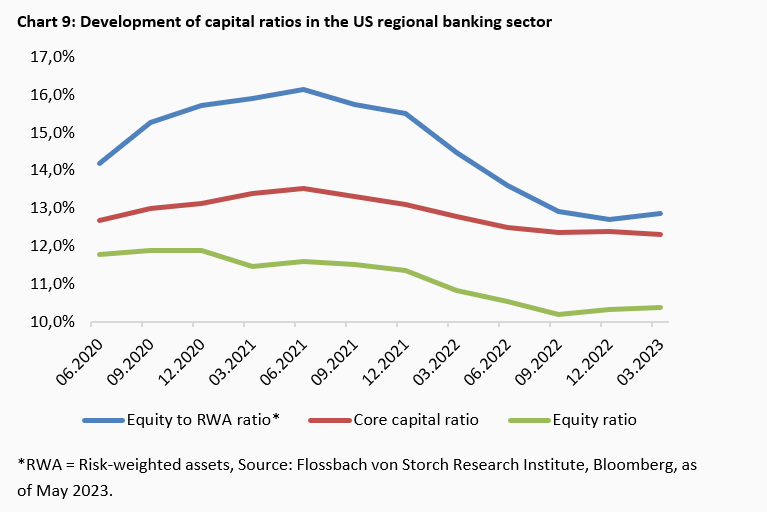

The price declines that call into question the value of the loans are hitting bank balance sheets with declining capital ratios (chart 9).

So while market and price risks are increasing, buffers at US regional banks have decreased.

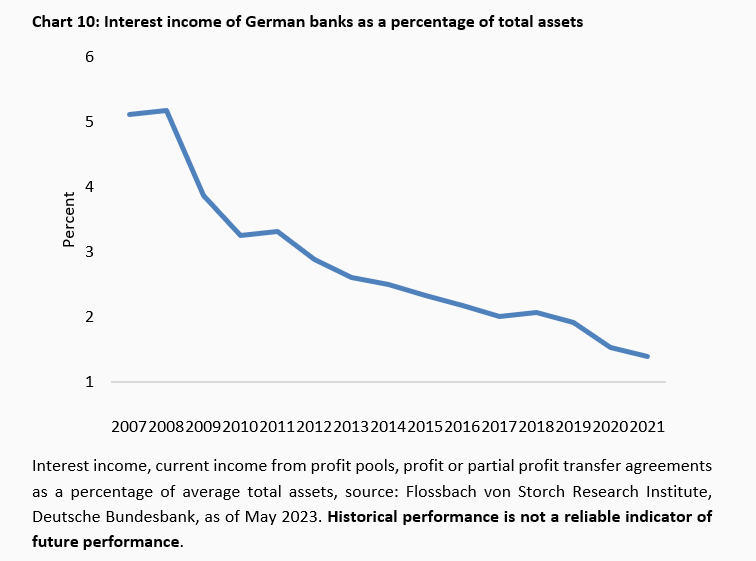

The situation is different for German banks. Here, for example, margins have been under pressure for some time. According to the latest available data, interest income as a percentage of total assets will shrink to 1.39 percent by 2021 - only a good quarter of the value achieved 13 years earlier (chart 10).

This income also includes income from profit transfer agreements, for example, which increases the margin.

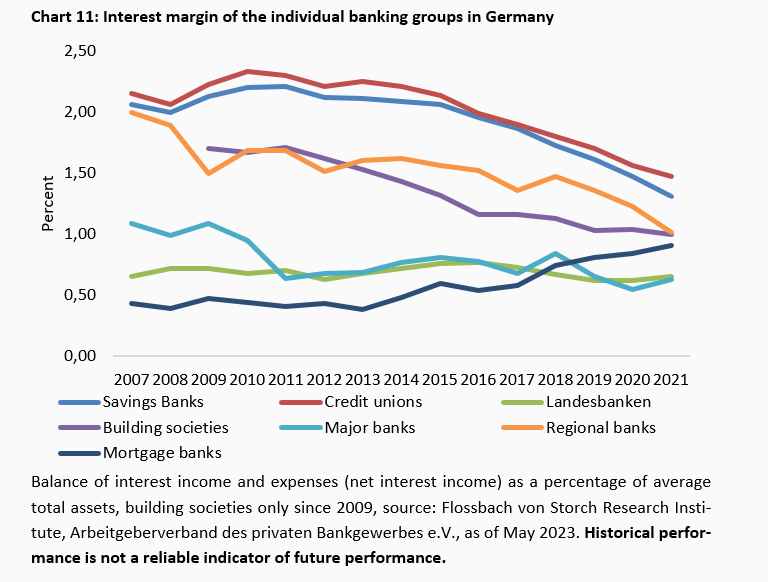

Measured in terms of pure net interest income as a percentage of the average balance sheet total, even lower and mostly declining earnings have been regularly evident across the individual bank groups for years (chart 11).

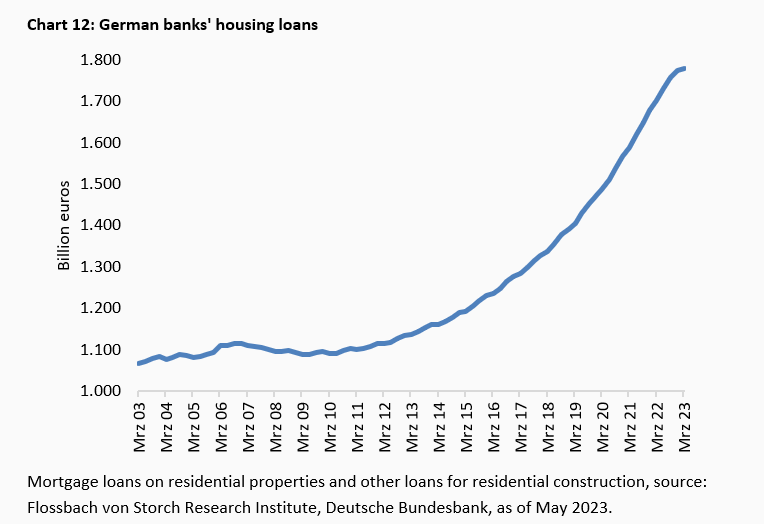

A major source of income is interest income from housing loans. In the course of the real estate boom of the past ten years, the volume of loans has increased by about half, after being almost constant in the decade before (chart 12).

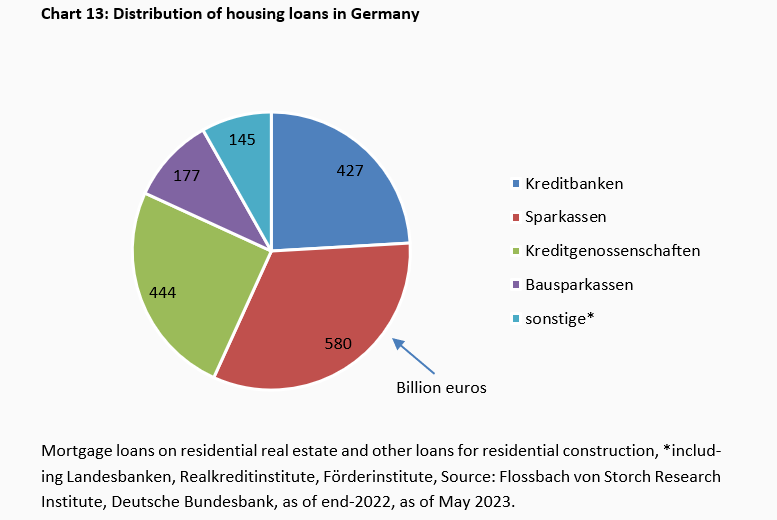

The fiercely competitive market, which is not very lucrative due to a flat interest rate structure over the years, is shared by the savings banks, private banks and the cooperative sector - each with considerable shares (chart 13).

In addition to residential real estate, loans for office buildings or logistics halls play a major role. According to data from the Association of German Pfandbrief Banks, domestic banks lent an average of almost 65 billion euros per year in new loans for commercial real estate between 2011 and 2020.

During this time, prices rose sharply: for office properties, for example, by around four-fifths. Meanwhile, the net initial yields for all commercial properties in 127 German cities fell from just under 6.0 to around 4.4 percent between 2011 and 2022. In the so-called top 7 cities (Berlin, Düsseldorf, Frankfurt, Hamburg, Cologne, Munich, Stuttgart), they were recently as low as 3.2 percent.

The fact that this is no longer sufficient to ensure interest coverage for new loans is evident on the stock market. For example, a large German commercial real estate company was able to finance itself in 2017, 2019 and 2020 through bonds at annual interest rates of 0.5 and twice 1.5 percent. Currently, the yields for these securities are around 9.0 per cent, which can be seen as an indicator of the enormous increase in refinancing costs.

According to the German Bundesbank, German banks had 839 billion euros in commercial real estate loans on their books at the end of February this year. German banks and real estate funds are also heavily involved in the foreign commercial real estate market through loans and investments. About a quarter of the commercial real estate loan portfolio of German banks is extended to borrowers abroad, according to the Bundesbank.

According to the Bundesbank, the core capital ratio for savings banks and credit cooperatives was just under 15.2 percent at the end of the second quarter of 2022. For the large, systemically important banks, it was 17.1 percent. Supervisors regularly consider such ratios to be adequate. The question is whether this will stand up to critical scrutiny.

Including housing loans, all real estate loans currently exceed the pure equity of the entire German banking sector by a factor of 5.9. Calculated very generously, including the fund for general banking risks, profit participation rights, subordinated liabilities and provisions, this results in a factor of 3.5 from capital plus all contingency reserves to loans for housing and commerce.

Conversely, this means that the banks could cover losses of at best 28.6 percent of all real estate loans until even the last reserve was used up. This would require a veritable crash, but then the banks' balance sheets would be completely bare and the entire sector could only be saved by nationalisation.

In a minor crisis, devaluations on all real estate loans of five percent, measured in terms of resilient capital, should be bearable, but ten percent would already be classified as critical. The BaFin recently cited a "surplus capital" in the German banking sector of 120 to 130 billion euros that would be available to absorb losses. That would correspond to about one-twentieth of all real estate loans. Not less, but not more either.

There is no shortage of crisis signals. In Germany, BaFin head Mark Branson recently warned of further turbulence in the banking sector: "It is not certain that this difficult phase - this stress test in real time - is behind us," Branson said, referring to the problems at the US regional banks and Credit Suisse.

Not all effects of the previous interest rate increases are visible yet, because valuations on the markets are only adjusted with a time lag. Banks must therefore prepare for further headwinds. "Stress phases often develop in phases," said Branson. Some German banks, he said, are facing high interest rate risks, low reserves and low capital buffers. Governance problems or hardly sustainable business models burdened further banks.

It is not reassuring that the Court of Auditors of the European Union (EU) recently reprimanded the European Central Bank (ECB) in a special report on banking supervision. The ECB, as the main supervisor of the 110 most important financial institutions in the EU, which account for 80 percent of all banking transactions, was doing too little to counter their credit risks.

The financing of German residential real estate is traditionally considered low-risk. But here, too, a situation has been brewing that is hardly comparable in historical terms.

The steep rise in interest rates will foreseeably burden the expenditure side and make it more difficult to obtain funding from short-term deposits, which have been favourable for many years because they do not bear interest. Recently, a price war has broken out in this area: several banks or financial subsidiaries of car manufacturers are offering time deposits with an interest rate of around three percent. Meanwhile, the 20-year construction loan from 2015, which is not due until 2035, is paying only 2.7 percent or even less.

New, expensive, and thus more profitable loans for the bank are almost a rarity: because the new business with residential real estate loans is virtually in a crash, which recorded a minus of 49.2 percent in the first quarter compared to the same quarter of the previous year. The reasons are also the uncertainties in view of the compulsory energy renovation planned by the federal government and the EU.

The banks are left with a reasonably decent source of income in the form of follow-up financing for maturing old loans, which brings them higher interest income than they have to offer on the deposit side. However, this financing must not overburden customers who have been spoiled by low interest rates if interest and repayment are to be guaranteed in the long run.

Lower valuations, and also the possible additional crediting for refurbishments, could lead to an interplay of problems in the banks' mortgage portfolios and among borrowers.

In its monthly report for February, the Bundesbank confirmed its long-known assessment of an overvaluation of German residential real estate. According to both the purchase price-income ratio and the results of estimates for the long-term relationship between property prices, income and interest rates, the prices for residential property are 20 to 30 percent above the reference value, according to the Bundesbank.1

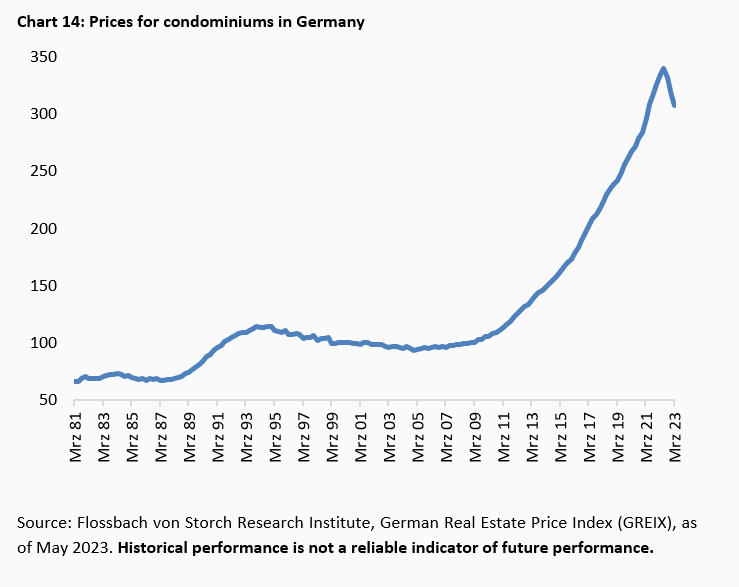

And the market is clearly slowing down: Prices for condominiums across Germany slumped by a nominal 9.5 per cent over the nine months to the end of March (chart 14).

Measured against consumer price inflation of around seven percent, this is a huge drop in real terms.

In some cities, residential property prices recently fell by up to 20 percent when adjusted for inflation, while prices nationwide averaged almost 15 percent below the peak when adjusted for inflation.

According to the index, Düsseldorf, Frankfurt and Hamburg, among others, were hit particularly hard by the price collapse, while prices in smaller cities such as Bonn fell less sharply. These are the first results of the new GREIX index, which is compiled on the basis of actual purchase transactions (expert committees) and is thus valid.

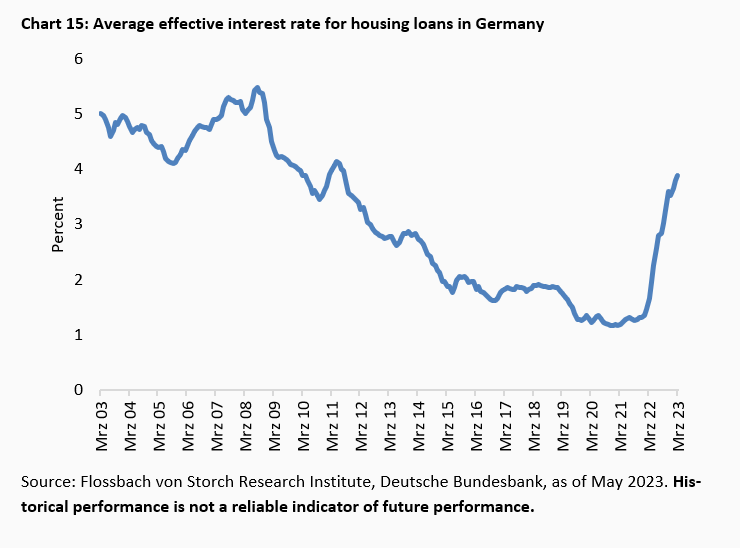

The main burden is the massively increased interest rate level (chart 15).

So the problem for German banks is: they are increasingly sitting on old loans from the low-interest period, will sooner or later have to grant higher interest rates on deposits, which they can no longer recoup in new business with real estate loans due to a lack of mass. And their customers are facing higher costs everywhere, which jeopardises their ability to repay loans properly.2

During the boom of the past few years, some banks financed more than the purchase price of the real estate at low interest rates - which were regularly significantly higher than the institutions' valuations even for new buildings. Low repayments have been standard for years. According to the loan broker Dr. Klein, the average repayment rate in January 2023 was 1.95 percent.

Such repayments mean that by the time the first building loan matures, around three quarters of the original loan amount is still due for refinancing. According to data from construction interest brokers, this is due after an average of 12 to 13 years.

The loan-to-value ratio (LTV), which is the ratio of the bank loan to the mortgage lending value of a property, also shows that banks have tended to be more risk-averse recently. According to Dr. Klein, the loan-to-value ratio in March was 82.19. At the beginning of data collection in 2010, the loan-to-value ratio was 76.87 per cent, well below the 80 per cent mark.

The 100-square-metre condominium from 1975, which was just worth 400,000 euros, is now plummeting to a market price in the direction of 320,000 euros. The upcoming investment in external insulation, a heat pump and new windows lowers the value by another 20 percent. Suddenly, the loan of 300,000 euros that was once granted and has hardly been repaid is no longer covered, or only just. What remains for banks is the hope that their borrowers can stay in work and, in case of doubt, mobilise reserves for energy-efficient renovation.

The costs for this could run into the trillions, should homeowners actually have to implement the plans of the federal government and the EU for heating replacement and energy refurbishment that are known so far. Conversely, the value of existing buildings could decrease significantly. Assuming an investment of two trillion euros for half of the existing stock, which has been little renovated so far, would mean a good 44 percent discount on its current value.3

The current crisis in the financial sector, which has so far gripped several US regional banks and, with Credit Suisse, a titan, is almost certainly not over. Once again, the heavily credit-financed real estate sector could prove to be the trigger for even greater turbulence. This time, however, not, or only to a limited extent, via packaged investments, but via direct financing.

Commercial real estate in particular is threatened with trouble. It would not be surprising if difficulties were to arise in the USA and Germany that would be unpleasant for the banks, and if this were to spill over into other markets.

Investments in residential real estate are no longer a safe bet either. Borrowers are losing income in real terms and, in addition, Germany may be facing energy renovations that could financially overburden quite a few owners.

The value of the loans lent by the banks is therefore in question. In addition, German financial institutions and US regional banks are likely to experience earnings difficulties, as customer funds can only be held with significantly higher deposit interest rates.

1https://www.bundesbank.de/de/publikationen/berichte/monatsberichte/monatsbericht-februar-2023-904654

22.03.2023 - Economics, Politics & Philosophy

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.

Christof Schürmann

Senior Research Analyst

At the Institute since 2022. The graduate in business administration (FH), previously worked as a journalist and deputy head of "Money" at WirtschaftsWoche. The trained banker and book author ("Die Bilanztrickser") taught balance sheet research part-time at the private university BiTS in Iserlohn.

All articles by Christof Schürmann