25.03.2024 - Studies

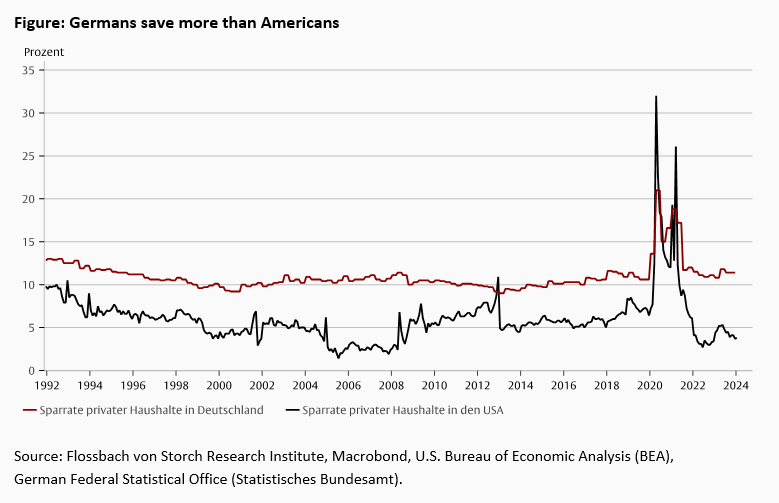

We Germans are still the world leaders when it comes to saving.1 Compared to the USA, private households in Germany save around twice as much of their disposable income. The savings rate in Germany is eleven per cent compared to just six per cent in the USA. Both countries have a statutory pension insurance scheme, which is organised on a pay-as-you-go basis, and additional company or private insurance schemes, which are funded. While pension contributions to pay-as-you-go insurance schemes are not included in the savings rate, they are taken into account in funded schemes.2

Unfortunately, we make too little of this virtue: German pensioners are poorer than their American counterparts. The disposable income of people over 65 in Germany is less than 90 per cent of the average disposable income of the population as a whole. In the USA, this figure is almost 95 per cent.3 In addition, only just under 60 per cent of pensioners in Germany live in their own property. In the USA, the figure is almost 80 per cent.4

Anyone who saves more but ends up with fewer assets is obviously investing at a lower rate of return. The decisive net return has three components:

Net return = increase in the value of investments - taxes - fees.

So do Americans invest in higher-yielding investments; do they pay less tax; are the fees lower? Or is it a bit of everything that gives Americans the edge?

In the first of two articles on this topic, we compare occupational pension schemes in Germany and the USA. In the second part, we then look for problems in private pension provision in Germany.

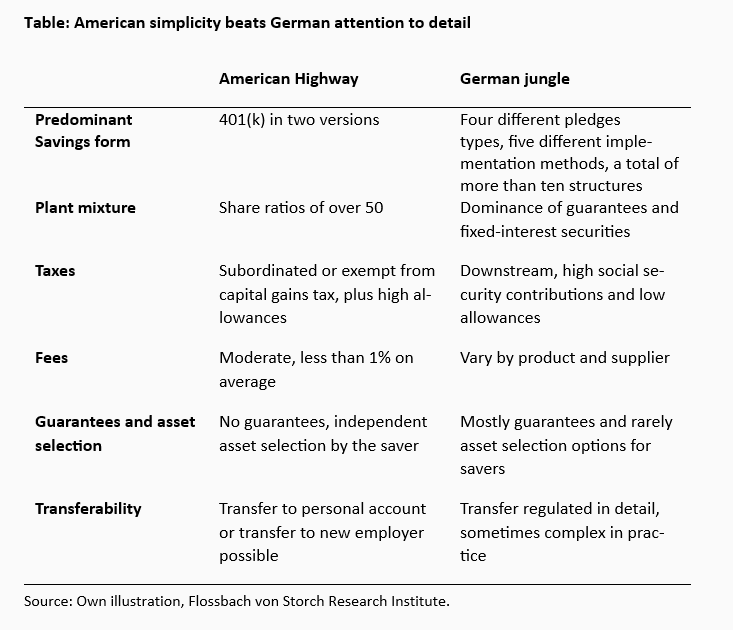

In the USA, there is a dominant form of company pension scheme, the 401(k) plan. It owes its name to the section of tax legislation that defines it. It is a savings plan in which the employee bears the risks and rewards of their own investment. The employer merely makes a contribution to the savings instalments. It is therefore also referred to as a "defined contribution" plan.

76 per cent of all American employees have access to a 401(k) plan. Almost 79 per cent of people with access save for their retirement as part of the plan.5 This means that six out of ten American employees use the company pension scheme with a 401(k) plan.

The employee can typically choose from various investment funds within the plan. In addition to pure equity and bond funds, mixed funds are also available. There are also products in which the proportion of fixed-interest investments is increased in old age in order to reduce volatility shortly before retirement.

In aggregate, the plans are characterised by solid equity ratios: Over 70 per cent of savers have at least 7 out of every 10 dollars invested in shares. Among those under 40, the figure is even higher at more than 90 per cent.6 As a result, the average 401(k) account increased by 14 per cent year-on-year to USD 118,600 in 2023 and the number of 401(k) millionaires rose by 11.5 per cent.7

401(k) is offered in two versions. The traditional plan has been around since 1978, and in 2006 the Roth 401(k) plan was added as an alternative. It is named after one of its spiritual fathers, former US Senator William Roth. The two plans differ only in terms of taxation.

In the traditional 401(k), the payments into the selected funds are deducted from the gross salary and thus reduce the taxable income. Only the social security contributions of 7.65 per cent have to be paid directly.8 If you have a lower income in retirement or move to a federal state with lower income tax rates, this results in a tax advantage. In the Roth plan, contributions are taken from net income that has already been taxed. In return, the payouts in old age are completely tax-free. Investment income within the plan also does not have to be taxed.

In 2024, employees may contribute up to USD 23,000 to their plans. The employer can contribute up to USD 46,000. The contribution limit is adjusted on an ongoing basis. Last year it increased by 4.5 per cent. Employees aged 50 or older can also make a "catch-up contribution" of up to USD 7,500 per year.9 This allows them to make up for savings missed in younger years.

If the saver exceeds the age limit of 59.5 years, he can withdraw the capital from the account at will. However, some schemes only allow larger withdrawals after retirement. It is not absolutely necessary to annuitise the capital. In the traditional 401(k) plan, however, the (progressive) income tax creates an incentive to consume the capital in instalments. If capital is withdrawn from the plan before reaching retirement age, there is usually a penalty of ten per cent of the amount withdrawn.

In the traditional 401(k) plan, the saver undertakes to continuously withdraw capital from the plan from a certain age. In this way, the American state avoids the saver deferring his income tax payments on the contributions "ad infinitum". The start and amount of these "required minimum distributions" are constantly adjusted in line with life expectancy. Currently, the first instalment must be withdrawn at the age of 73 at the latest. The assumed remaining life expectancy is 26.5 years. At least 3.8 per cent of the capital is therefore paid out and taxed each year.10

If the saver changes employer, he has several options for continuing the savings plan. They can leave it with their old employer or - if available - take it with them to their new employer. In addition, a transfer to a private savings plan, an "Individual Retirement Account", is also possible. The choice of options puts pressure on the prices of the products, which reduces the fees. The average cost of a 401(k) plan is less than one per cent of assets per year. For larger employers with more employees and more assets, costs can drop to less than 0.5 per cent of assets under management. A study observed falling costs in all size categories for the years 2009 to 2012.11

Saving with a 401(k) is convincing in all three components of the net return: the increase in the value of the investments - also known as the gross return - is sufficient for real wealth accumulation due to the high equity ratios. It averages between five and eight per cent.12 The traditional plan enables a tax advantage in old age through deferred taxation. The Roth plan does not tax capital gains at all. Savers' switching options ensure low cost rates.

The clear regulatory framework makes it easier for new providers to enter the market. The transparency resulting from the simplicity enables employees to fulfil their investment responsibilities. It is precisely this simplicity that makes 401(k) plans a success story.

In Germany, company pension schemes are just as widespread as in the USA: 54 per cent of employees have a company pension scheme. This is only six percentage points below the American level.13 However, unlike in the USA, savers are not simply divided between two similar plans.

On the one hand, there is the classic defined benefit model, which guarantees the saver a fixed one-off benefit or pension. The investment risk is borne by the employer. On the other hand, there are now three defined contribution models in which the employer is only required to make limited guarantees regarding the subsequent payout amount.14 These are the defined contribution benefit commitment (BOLZ), the defined contribution commitment with minimum benefit (BZML) and the pure defined contribution commitment (RBZ). The first two require more or less high contribution guarantees. The latter can only be implemented within the framework of a collective agreement and is therefore also known as the social partner model.

Each of the four types of commitment can then be implemented in up to five different ways. A distinction is made between insurance-based methods, i.e. via a life insurer, a pension fund or a pension fund, and non-insurance-based methods, i.e. a direct commitment by the employer or the establishment of a provident fund.15 There are over ten different models.

German savers usually have little choice when it comes to selecting an investment. Depending on the implementation method, their options are already limited by regulation: For example, if the employer decides to implement the occupational pension scheme via a pension fund, the investment regulations prohibit equity ratios of over 35 per cent.16 In addition, legally prescribed contribution guarantees make it necessary to secure these with the help of guarantee products. It is not always possible for employees to choose their investments.

The Riester pension, which can also be implemented as a company pension scheme, showed par excellence how a nominal guarantee of contributions prescribed by politicians systematically destroys the return: either the contributions were initially divided between shares and bonds on the basis of risk budgets and then had to be shifted entirely into bonds to fulfil the guarantee in the event of price slumps on the stock market. Alternatively, the capital was secured by zero-coupon bonds and the rest was invested in shares. However, this procedure became obsolete in the low-interest phase, as after the purchase of the bonds and the deduction of costs, there was no capital left to invest in shares.

In principle, equity ratios and returns vary depending on the occupational pension solution used: insurers with equity ratios in the low single-digit range achieved returns of around 3.5 per cent in 2014. Pension funds with equity ratios of 25 to 30 per cent, as used by some DAX companies, generated returns of around 7.5 per cent in the same year.17 High gross yields are therefore not impossible in Germany. Compared to the USA, however, the equity ratios are usually significantly lower. On the other hand, returns struggle with contribution guarantees and investment regulations imposed by politicians. Savers pay the price, often without being able to influence the investment themselves.

The jungle created by the large number of commitment types and implementation channels results in a maze of regulations for taxation: contributions up to a limit of EUR 3,624 per year are exempt from social security contributions. Double this amount is exempt from income tax. In old age, payments from a company pension are then taxed as income and social security contributions must be paid. Therefore, taxes and contributions are sometimes due twice above the exempt amounts - a so-called double contribution. In contrast, payments into direct commitments are tax-free indefinitely and there is now an allowance for health insurance contributions in the payout phase. Contributions to long-term care insurance, on the other hand, must be paid in full. Capital gains tax is generally not payable.

Seen from a distance, the taxation rules are similar to those of the traditional 401(k) plan in the USA. However, the tax-free amounts are only 15 or 30 per cent of the US level. Exceptions attempt to compensate for this. However, this does not give the German occupational pension scheme a fundamental regulatory advantage in terms of taxes and social security contributions.

Each type of company pension scheme in Germany requires its own specialised legal and actuarial knowledge. This legislative fragmentation drives up costs both directly and indirectly: on the one hand, the administration of assets becomes costly. On the other hand, there are barriers to entry for new providers, which limits competition.

Using the example of the Riester pension, the CFA Society Germany has illustrated the impact of regulatory costs on the net return. In a sample calculation, there is a difference in return of 1.5 percentage points per year for the saver. A 50-year equity savings plan, which starts with an annual savings sum of 1,000 euros and is continuously topped up, delivers a final capital of 400,000 euros at standard market costs. This corresponds to an average interest rate of 5.5 per cent. In the reference scenario, a central investment platform with lower costs proposed by the CFA, the figure is over 650,000 euros or seven per cent.18

The extent to which high administrative costs in asset management and a lack of competition are responsible for the costs cannot be determined across the board. Nor do we know whether larger employers in particular can negotiate special conditions for their employees. In any case, it is worth comparing providers. A recently published survey on the effective costs of life insurance policies by BaFin showed enormous differences: if you take out a unit-linked life insurance policy at the age of 37, you pay no more than 1.3 per cent per year with the 25 per cent cheapest providers. With the 25 per cent most expensive providers, the costs are at least 2.35 per cent, i.e. a whopping 80 per cent more.19

The conclusion on fees is similar to that on taxes and social security contributions: In principle, it is possible to obtain favourable conditions in Germany similar to those in the USA. However, it is only possible to get there via a tortuous route, which requires a high level of expertise and persistence on the part of the entrepreneur.

The transferability of entitlements in the event of a change of employer is also subject to a great deal of regulatory detail: in principle, there is a right to transfer between pension funds, pension funds and direct insurance. However, this only applies if the transfer value does not exceed a limit of around 90,000 euros. This corresponds to a pension of just 300 euros. If an entitlement has grown to more than this amount, a new occupational pension scheme must be taken out with the new employer. For older employees in particular, this may no longer be worthwhile due to possible acquisition costs. In addition, practitioners report that the transfer of an entitlement does not always go smoothly.20

Transferring commitments outside of the above-mentioned regulation then again depends on the individual case and the goodwill of all parties involved. Whether a commitment can be continued as a private savings plan must also be examined on a case-by-case basis. These hurdles make a change, even if it is possible, unattractive for the individual employee.

Occupational pension schemes in the USA are like a well-developed highway on which everyone can quickly and safely reach their goal of securing their standard of living in old age. Gross returns are high, tax breaks incentivise saving and fees remain reasonable due to competition and low regulation. In addition, savers can largely decide for themselves what risks they want to take when investing their capital.

Setting up a company pension scheme in Germany is like a jungle expedition. The employer has to fight his way through a thicket of regulations in search of good solutions for his employees. If he is not thorough in his choice of route and expedition leader, his employees sometimes suffer losses. Guarantees and other regulations introduced to supposedly protect the investor make progress difficult in many ways.

This results in demands on German politicians. A path should be cut through the regulatory jungle and a "savings motorway" should be built: They should concentrate on one type of commitment and simplify it as far as possible. Simplicity must take priority in order to create transparency and enable self-determined saving. Such a simple solution should dispense with guarantees, guarantee improved transferability and include an extension of tax incentives.

1 Statista: Savings rates of private households in countries worldwide until 2019.

2 T. Mayer: Savings glut due to old-age provision?, 2020.

3 OECD: Pensions at a glance 2021, Slide 7, Figure 1.9.

4 Statista: Housing situation by age group 2023 and US Census Bureau: Annual homeownership rates, 2024.

5 Transamerica Center for Retirement Studies: Post-Pandemic Realities: The Retirement Outlook of the Multigenerational Workforce, 2023.

6 Investment Company Institute: 401(k) Plan Asset Allocation, Account Balances, and Loan Activity in 2020, Figure 8, 2022.

7 CNBC based on Fidelity: 401(k) millionaires and average balances rose in 2023, Fidelity says, 2024.

8 1,45% Medicare Tax and 6,2% Social Security Tax

9 Fidelity: 401(k) contribution limits 2023 and 2024, 2024.

10 Employee Fiduciary: 401(k) Required Minimum Distributions – What You Need to Know, 2023.

11 Investment Company Institute: The BrightScope/ICI Defined Contribution Plan Profile: A Close Look at 401(k) Plans, 2014.

12 TIME: Average 401k Return Rate: What To Expect?, 2023.

13 Federal Ministry of Labour and Social Affairs: Distribution of old-age provision 2019, 2020.

14 German Actuarial Association: BOLZ, BZML und RBZ – Wir bringen Licht in den Dschungel aus Abkürzungen und Arbeitsrecht, 2022.

15 An overview of the common possible combinations can be found in footnote 14.

16 Federal Ministry of Justice: AnlV - Verordnung über die Anlage des Sicherungsvermögens von Pensionskassen, Sterbekassen und kleinen Versicherungsunternehmen, §3(3), 2020.

17 Wirtschaftswoche: Company pension schemes: Weak returns on forms of insurance, 2014.

18 CFA Society Germany: Positionspapier_Altersvorsorge_2022_web_FINAL.pdf (cfa-germany.de), Tabelle 2, 2022.

19 Bafin: Specialist article - When life insurance costs too much, 2022.

20 S. Pieper & S. Müller: How does the transfer of occupational pensions work?, 2023.

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.

Sven Ebert

Senior Research Analyst

At the Institute since 2022. The actuary and actuary DAV holds a doctorate in probability calculation from the Karlsruhe Institute of Technology. He has been a lecturer at the Technical University of Cologne for several years and is active in the DAV actuary training programme of the German Actuarial Academy. His topics include old-age provision and behavioural finance.

All articles by Sven Ebert