27.09.2023 - Studies

Inheritances, gifts and one-off payments offer financial freedom. However, how people deal with their new wealth varies according to their origins and associated emotions. A look at theory and empirics.

Not only tennis fans still remember 7 July 1985 - Boris Becker became the youngest Wimbledon winner of all time at the age of 17. In the following 15 years, he rushed from one sporting success to the next. He becomes the idol of an entire (tennis) generation and earns 25 million US dollars in prize money alone. At the turn of the millennium, Becker ended his active career. A good fifteen years later, in 2017, a London court declared him insolvent. It seems as if Becker woke up at the end of his career as a wealthy man next to a fortune, but did not know how to deal with this new situation.

He is not alone in this. The tabloids are full of stories of lottery winners who spent all their winnings within a few years.1 Although few people become sports stars or beneficiaries of gambling, there are other ways to get a larger fortune: an inheritance, gifts or life insurance payouts are less glamorous, but much more common.

What happens to people who experience a sudden increase in wealth? What feelings are addressed and how does their consumption behaviour change according to theory? What does empirical research say about this? Do heirs and lottery winners all end up broke or do we end up subject to the "availability bias", i.e. the fact that human misfortunes sell better than success stories?

Between 2015 and 2024, approximately six million intergenerational inheritances will take place in Germany - this is 600,000 inheritances per year. A total of 2.1 trillion euros will be passed on to the next generation. On average, 360,000 euros are inherited per inheritance. Assuming two heirs per inheritance, in line with the fertility rate of the 1960s, this amounts to 180,000 euros per person. About half of the inheritances contain real estate assets. Consequently, these are the higher inheritances. In most cases, financial assets are also inherited. The testators are increasingly the generation of the children of the economic miracle. Inheritors are the baby boomers and increasingly also the subsequent "pill generation".2 In addition to inheritance, there are also gifts. Measured in terms of tax volume, they account for about one third of inheritances in terms of number and amount.3

The popular savings form of life insurance also accumulated considerable sums in 2022. German life insurers paid out a total of 49 billion euros in capital benefits in 2022. Compared to the new business of 340,000 policies, this is about 140,000 euros per person.4 Thus, more than one million people in Germany are confronted with having an (additional) six-digit euro amount at their disposal every year.

The first theory on the question of how people deal with increases in wealth and income was put forward by Milton Friedman in 1957.5 In his Permanent Income Hypothesis, he assumes that both income and consumption break down into a permanent and a temporary part. Temporary income changes are uncorrelated with temporary consumption changes - i.e. a one-time payment is not directly consumed. Permanent consumption only changes if the expectation of permanent income changes. Nevertheless, permanent consumption is influenced by the ratio of wealth to income. If a one-time payment is saved, this ratio increases and permanent consumption rises.

A study from 1972 refuted Friedman's theory for smaller amounts and confirmed it for larger ones.6 Friedman himself also gives arguments for and against his theory. The central legacy of the theory remains the realisation that not all types of income are to be treated equally in economic terms.

Economist Richard Thaler and lawyer Cas Sunstein built on this insight in 2008. However, instead of assuming the financially rational investor with complete information, as Friedman did, the two focus on the human individual with all his strengths and weaknesses. Decisions therefore do not always have to be rational. They claim that different pots or accounts are formed in the mind for different types of income, the "mental accounts". Money mentally has a label and can thus no longer be used arbitrarily.

Thaler and Sunstein conclude that a sudden increase in wealth that is not self-generated is considered a "gain". Such a bonus is not needed to make a living. People are therefore more likely to spend "gains" on luxuries, as opposed to self-earned money. This tendency is reinforced by the fact that spending "profits" is not considered a loss of wealth. "Profit" is a pot that - like a gift - stands apart from normal wealth.

A study based on surveys in China supports the hypothesis.7 Participants were asked to indicate how they would use (hypothetical) lottery winnings and earned income. Self-earned income was always spent more on a "reasonable" alternative such as replenishing one's canteen balance. Lottery winnings were increasingly used for luxury goods such as a meal in an expensive restaurant.

However, the results of the study are not symmetrical. A lottery win is indeed used more often for luxuries than self-earned money, but the luxury goods are not preferred as strongly as the reasonable alternative in the case of self-earned money. Thus, there is a structural preference for reasonable expenditure. The study authors provide various explanations: They assume that limited personal financial possibilities of the participants inhibit spending on luxury goods. In addition, there is the fact that Chinese culture values thrift and hard work more highly than extravagance and indulgence. There is also speculation about the influence of the amount of the one-off payment. In particular, the authors point to the influence of the emotions associated with the payment. The distinction they make between "happy money", which is primarily used for luxury goods, i.e. hedonic consumption, and "unhappy money", which is used for sensible consumption, leads us to "emotional accounting".

The idea that it is not only the origin of money, but also the emotional link with the amount that determines how it is used was already explored in 2009:

"Specifically, we argue that the emotional response to the receipt of a sum of money can become associated with the money itself in the form of an "affective tag". In effect, we suggest that in the same way that money is categorised by its source in mental accounting, it can also be categorised by the feeling it evokes."8

If the fundamentally positive feelings that arise from one-time payments are overlaid by negative emotions, a targeted motivational push to lighten one's mood arises. One strategy for this is hedonic avoidance, i.e. rejecting hedonic consumption. Alternatively, a distancing from money can occur by postponing the decision on its use - in short, the money is saved for the time being. Or the money is used for projects that seem "virtuous" to the individual. This is an attempt to "cleanse" oneself of negative emotions.

A prominent example of the latter behaviour is provided by the German politician and banker's son Tom Koenigs. He donated his inheritance to the Vietcong:

"When I came of age at 21, I realised that he [his grandfather] had left me a lot. I was active in the student movement in Berlin at the time, I was more concerned with the question of justice and equality than money. I consequently gave that away to the Vietcong."9

And further:

"At that time I simply wanted to help the small threatened people of the Vietnamese."10

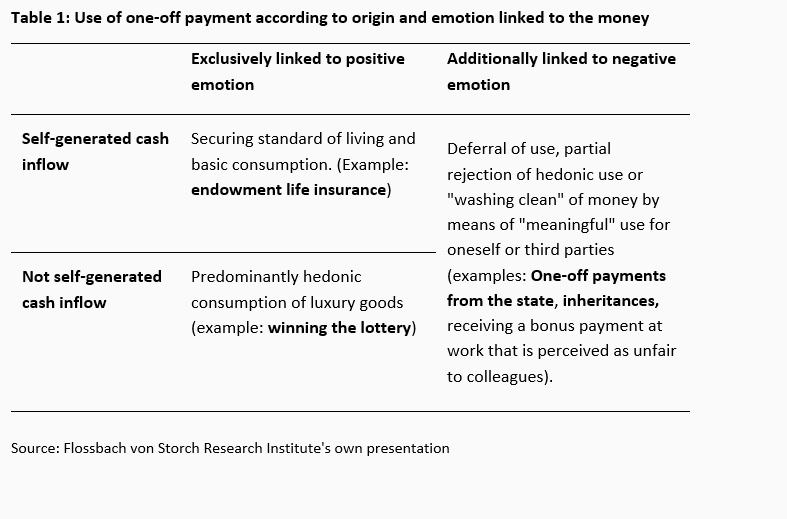

If we combine our previous results along the two dimensions of origin of money and emotions, the following schematic typification emerges:

People deal more sensibly with money they have earned themselves than with money they have received from third parties. However, if the additional money is not only emotionally positive, the person tries to overcome the associated negative emotions. This can be done by postponing its use, refusing to spend it for hedonic purposes or using it in a "meaningful" way. The latter can be done, for example, by donating to charity, providing financial support to friends and family, or investing in durable goods such as furnishings. We match these theoretical findings with empirical studies in the following.

Let's start with self-generated wealth, which is linked to positive emotion. According to theory, the resulting wealth should be used "wisely" to secure one's standard of living. Negative emotions such as guilt do not influence the use.

The German Insurance Association provides empirical evidence. Payouts from endowment life insurance policies are converted into annuities to a considerable extent. The Annual Report 2022 states:

"Apparently, citizens used already existing assets or the maturity benefits from endowment policies to take out immediate or deferred annuity policies for a single premium." 11

The report shows that two out of three euros of all newly invested single premiums are accounted for by pension insurance policies.

In addition, the mere prospect of creating a cushion for old age through one's own work seems to have a positive emotional impact on savings contributions to be paid in the future: Every second newly concluded contract for regular payments is an annuity or pension product. In this case, the use as an annuity payment (in retirement) is thus already determined as the use for the money at the beginning of the savings process. Only one in ten policies, on the other hand, is an endowment policy, where one decides anew on the use of the capital at the age of 65. The mere prospect of creating a cushion for old age through one's own work seems to have a positive emotional impact on the savings contributions to be paid in the future.

How representative the behaviour of policyholders is for the population as a whole remains an open question. However, with a total of more than 2.5 million newly concluded pension or endowment life insurance policies in 2022 and a portfolio of almost 70 million contracts, there is a solid data basis. By comparison, the number of home loan and savings contracts in Germany is just one third, at 23 million.

The data on our second example, lottery winnings, are naturally much thinner. However, it is known that one out of three lottery winners in the USA will become insolvent at some point and that lottery winners have an increased probability of bankruptcy three to five years after winning compared to the population as a whole. And this despite the fact that the winnings are generally sufficient to pay off all existing debts.12 The money not earned is therefore spent over time. Once it is used up, it is not possible to reduce consumption to a normal level.

To protect the winners, some lottery companies therefore convert the winnings into long-term pension payments. In studies based on this form of payout, after half the payout period, in this case ten years, the winners had saved as much as 16 percent of the amount paid out up to that point. At the same time, however, a decline in earned income was found.13 Stretching the payout over time thus seems to provide for a somewhat more sensible use. Nevertheless, a long-term safeguarding of the standard of living as achieved by life insurance cannot be observed.

The Corona pandemic provides further illustration of how people deal with income they have not earned themselves: In March 2020, 300 billion US dollars, about 1200 USD per person, were announced in one-time payments by the American state to its citizens. One year later, another 1400 USD per person were added.14 Although the amounts are significantly lower than the typical lottery win, all citizens benefited from the payments, which makes the results more representative.

In contrast to lottery winnings, state gifts are emotionally mixed: in principle, attitudes towards one-off payments from the state are positive.15 In particular, the classic negative emotions such as guilt and unjustified preferential treatment are not present, since all citizens are equally entitled to the money and, unlike e.g. inheritance, there is no direct connection between the payment and the death of a relative. Some citizens, however, doubt the meaningfulness of state one-off payments in principle. Their emotional relationship to the payments is therefore negative. One should therefore see a mixture of hedonic consumption and "pure-washing" use in their use.

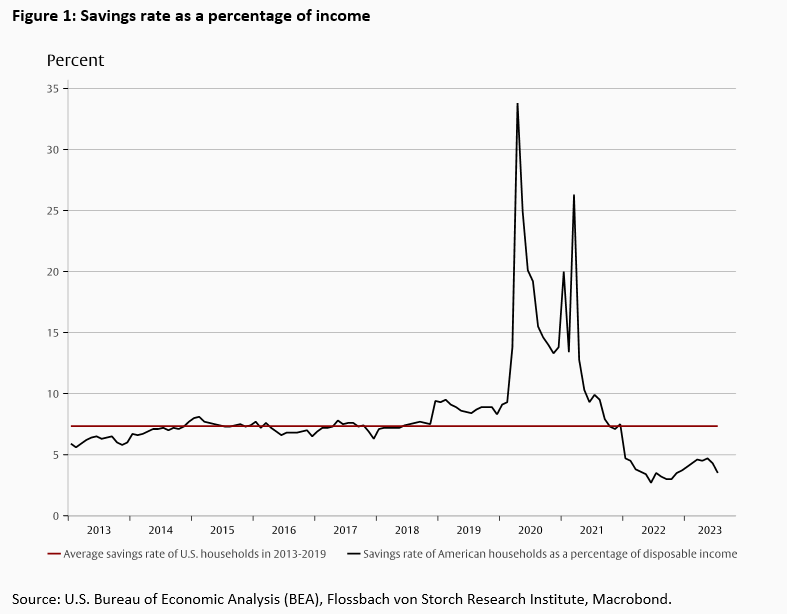

The savings rate of American households as a percentage of disposable income before, during and after the Covid-19 pandemic provides information on when the money was used (Fig.1):

First, the household savings rate increased significantly in 2020 compared to the pre-Corona level. At the same time as the second aid package, the savings rate fell below the pre-pandemic average. Until today, people are spending the money they saved.

The consultancy Deloitte initially identified rising spending on "durable goods" and "recreation gadgets" during the period of public life restrictions.16 The former includes, for example, new home furnishings. The meteoric rise of the home bicycle provider Peloton is an example of the latter. With a purchase price starting at 1500 euros per bike and additional monthly costs of 39 euros, this can be described as a luxury good.

As public life became more normalised, spending shifted to the service sector: a nine percent increase in total American household spending from 2021 to 2022 was accompanied by a disproportionate 20 percent increase in spending on restaurant visits. Spending on overnight stays on "Out Of Town Trips" grew even faster at 39 percent.17 From a mixed use of payments for durable goods and luxury goods, a slow transition to increased hedonic services has emerged.

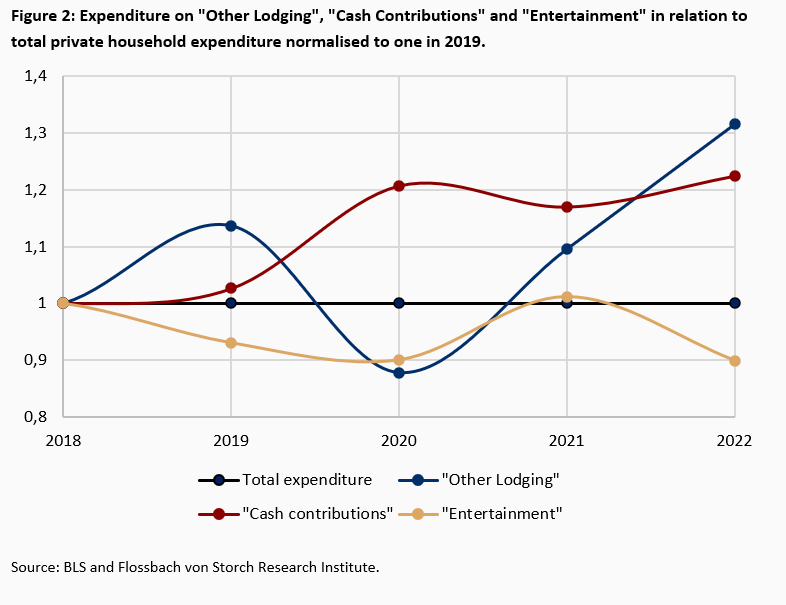

However, if one compares the expenditure of private households before Corona with that during the pandemic, another aspect emerges. The category "Cash Contributions" shows the largest increases. This includes spending on non-personal consumption and thus items such as donations to charitable organisations, financial educational support within the family and gifts - all of which are "meaningful" expenditures. Figure 2 shows the shares of different types of expenditure in relation to total household expenditure.

Between 2019 and 2021, the (hedonic) expenditure for "Entertainment" increased more strongly than the total expenditure. The decrease in 2022 was compensated by the category "Other Lodging", which includes in particular the already mentioned "Out Of Own Town Trips". Together, as already described, we see that people are indulging themselves. In addition to these hedonic motives, however, there is also a clear increase in expenditure on "cash contributions". Compared to total spending, the share rose from 3.2 percentage points in 2019 to 3.8 points in 2022 - an increase of almost 20 percent.

Whether these changed spending patterns can be attributed solely and causally to the one-off payments is, of course, not clear. The bottom line, however, is that, as theoretically predicted, one sees a part of hedonic consumption and a part of "purely laundering" use of the state one-off payments.

Inheritance is the classic example of one-off payments that have a distinctly negative emotional connotation. A sudden increase in wealth at the expense of another human life often triggers profound feelings of guilt and even identity crises. In psychology, this is known as "Sudden Wealth Syndrome".18 According to our theory, the guilt should limit the hedonic consumption of the inheritance and be reflected in higher savings rates compared to lottery winners.

A study by Jay Zagorsky from 2012 shows this: For every three euros of inherited wealth, the individual saves on average between 1.5 and two euros. A maximum of half of an inheritance is therefore consumed. The National Bureau of Economic Research confirms the figures. For inheritances of more than 150,000 US dollars, assets increased by 66% three years after the inheritance.19 A study by the German Institute for Retirement Provision shows that - at least in the short term - half of an inheritance is not touched at all.20 Compared to lottery winnings, all three studies show a much more "sensible" approach to inherited wealth. We remember: On average, only 16 cents are saved from lottery winnings for every dollar won.21

Inheritances of less than 150,000 US dollars even show increases in wealth within three years that are many times greater than the inheritance. This indicates that with smaller inheritances there is no restriction of work activity. There would be no other way to achieve a further increase in wealth. In contrast, one study found a six percent drop in average income for lottery winners, even if they won a maximum of US$5,000. The proportion of winners with positive income fell by ten percent. Apparently, sensible management is not only limited to inheritance, but also to other lifestyle.

Anecdotes of people who have completely spent large fortunes within a short period of time are often exploited by the media and stick in our minds. Due to the "availability bias", the impression is created that a sudden windfall per se plunges people into misfortune. This contradicts the fact that (larger) one-off payments generally have a positive connotation and in some cases massively expand the financial scope of the individual. However, differences can be observed in the use of the increase in wealth depending on the origin and the associated feeling.

People are generally more sensible with money they have earned themselves than with money they have not earned themselves. This is reflected, among other things, in increased probabilities of insolvency and low savings rates of lottery winners. The emotions attached to the payment play the second central role in the use of one-time payments. Feelings of guilt inhibit the impulse to consume luxury goods and increase the desire to use the money sensibly. In this way, one distances oneself from one's feelings of guilt or cleanses oneself of them. This is reflected in higher savings rates in the case of inheritances and in increased "cash contributions" in the case of one-off state payments. This at least gives hope that the heirs of the baby boomers will preserve the capital stock they created and not give it away to questionable, Vietcong-like recipients for consumption.

And Boris Becker? He made his fortune himself and lost it again. Perhaps his talent and his career seemed like a "sixpence in the lottery" to him? Perhaps he is simply an exception to the rule. Or when was the last time you heard anything about Steffi Graf?

1 5 schräge Millionäre, die ihr Vermögen verprasst haben | News | BILD.de

2 DIA_Studie_Erben_in_Deutschland_LowRes.pdf (dia-vorsorge.de)

3 Erbschaften und Schenkungen bis 2022 | Statista and Geerbtes und geschenktes Vermögen 2022 nach Rekordjahr 2021 um 14 % gesunken - Statistisches Bundesamt (destatis.de)

4 die-deutsche-lebensversicherung-in-zahlen-2023-publikation-pdf-data.pdf (gdv.de)

5 The Permanent Income Hypothesis (nber.org)

6 The-Relative-Size-of-Windfall-Income-and-the-Permanent-Income-Hypothesis.pdf (researchgate.net)

10 Ibidem

11 die-deutsche-lebensversicherung-in-zahlen-2023-publikation-pdf-data.pdf (gdv.de)

12 What percent of lottery winners eventually go bankrupt? - Blog (ngpf.org) and MIT_REST_110030 961..969 (gwern.net)

14 CARES Act - Wikipedia und Bidens "American Rescue Plan" - Hans-Böckler-Stiftung (boeckler.de)

15 Emotional Accounting: How Feelings About Money Influence Consumer Choice by Jonathan Levav, A. Peter McGraw :: SSRN, page 76.

16 Consumer spending on services | Deloitte Insights

17 CONSUMER EXPENDITURES--2022 - 2022 A01 Results (bls.gov)

18 Sudden Wealth Syndrome - Wikipedia

19 Microsoft Word - Inheritance and Saving Up.doc (nber.org), Table 1.

20 DIA_Studie_Erben_in_Deutschland_LowRes.pdf (dia-vorsorge.de), Table 14.

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch SE. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch SE remains solely with Flossbach von Storch SE. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch SE.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch SE.

© 2024 Flossbach von Storch. All rights reserved.

Sven Ebert

Senior Research Analyst

At the Institute since 2022. The actuary and actuary DAV holds a doctorate in probability calculation from the Karlsruhe Institute of Technology. He has been a lecturer at the Technical University of Cologne for several years and is active in the DAV actuary training programme of the German Actuarial Academy. His topics include old-age provision and behavioural finance.

All articles by Sven Ebert