09.09.2019 - Studies

Due to the weakening inflation expectations and trade war’s uncertainties, major central banks are expected to implement strategies to prevent an accident.

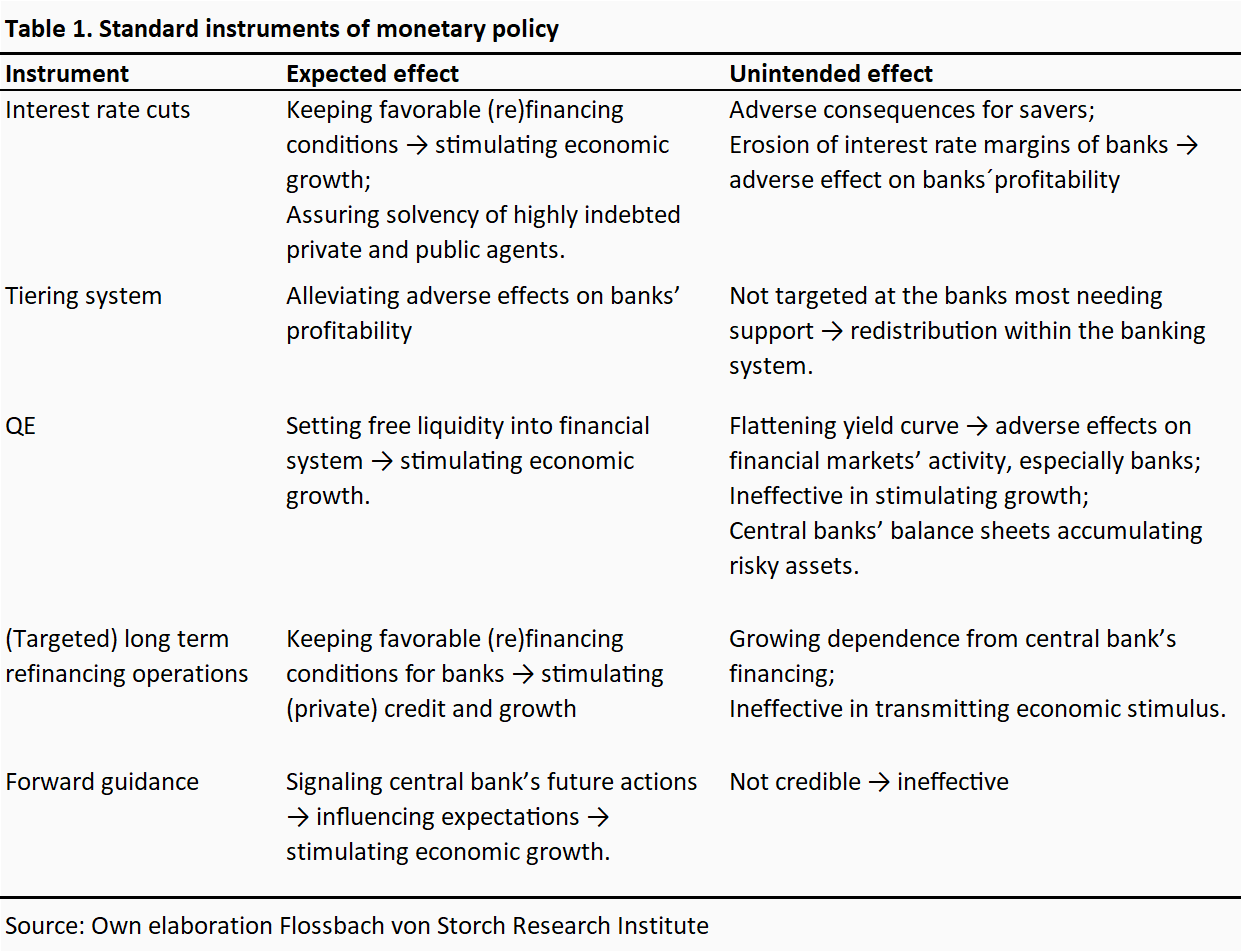

It is plausible to expect that the upcoming monetary easing will begin with standard instruments – especially interest rate cuts and quantitative easing. However, in view of their declining marginal productivity and the technical difficulties in implementing some of them, innovative instruments will be demanded in the next step.

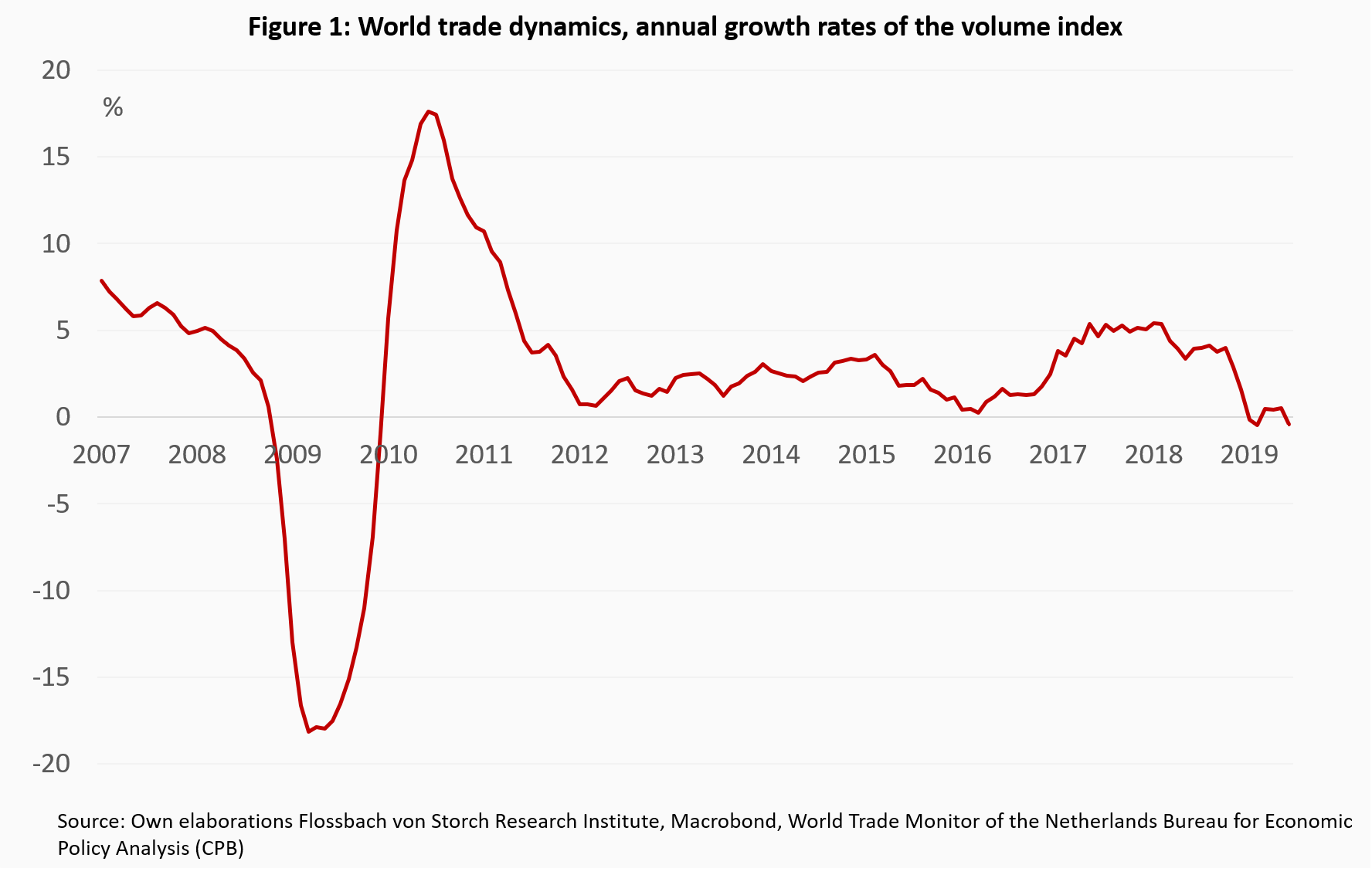

According to their own logic, central banks worldwide should have growing reasons to be concerned. The global economy is showing visible signs of contraction. Although several factors are likely to contribute, the US-China trade war is probably the one with the highest explanatory power, with spillover effects clearly visible on the global level: global trade has weakened considerably since its peak in January 2018 (Fig. 1).

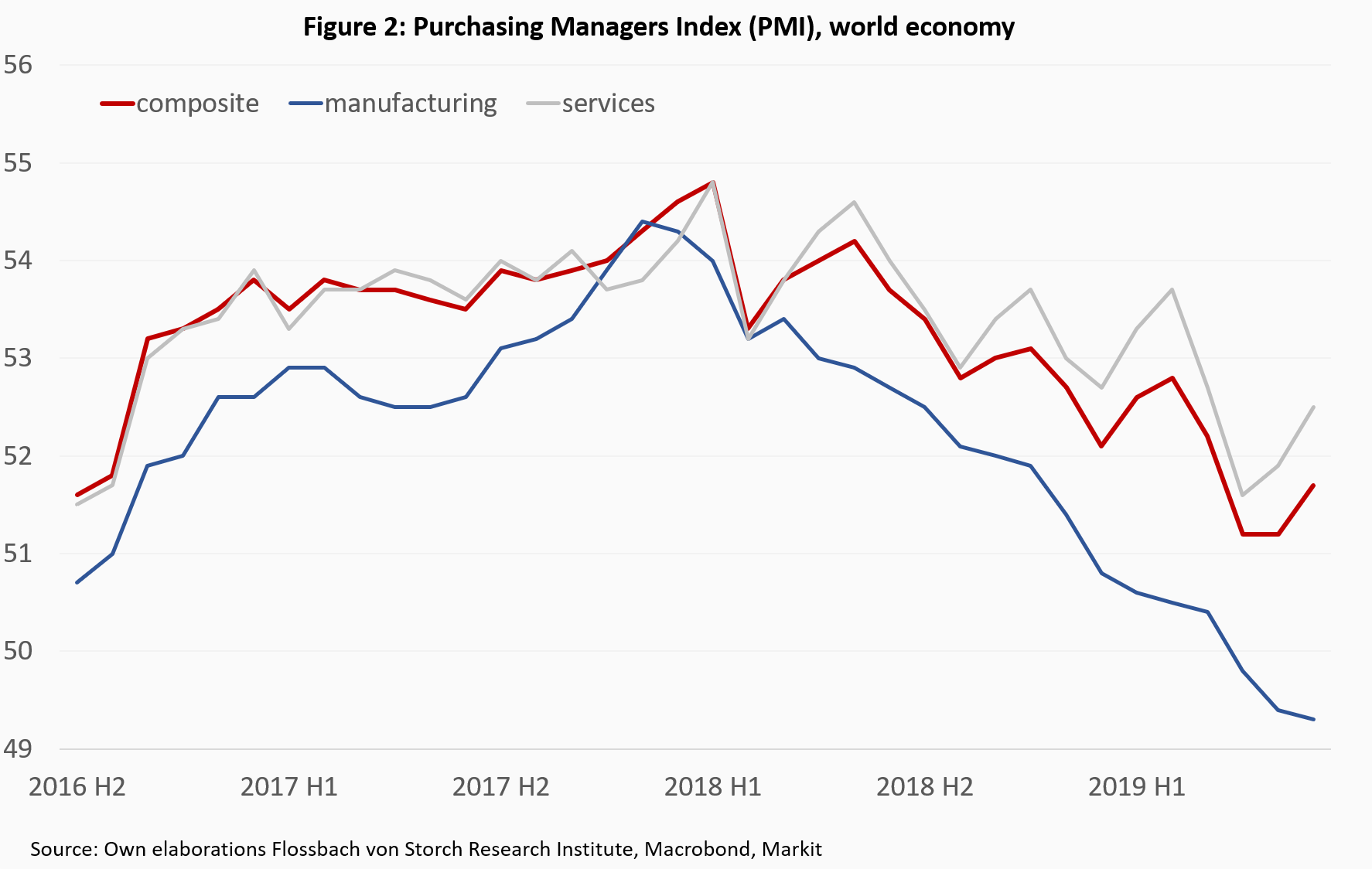

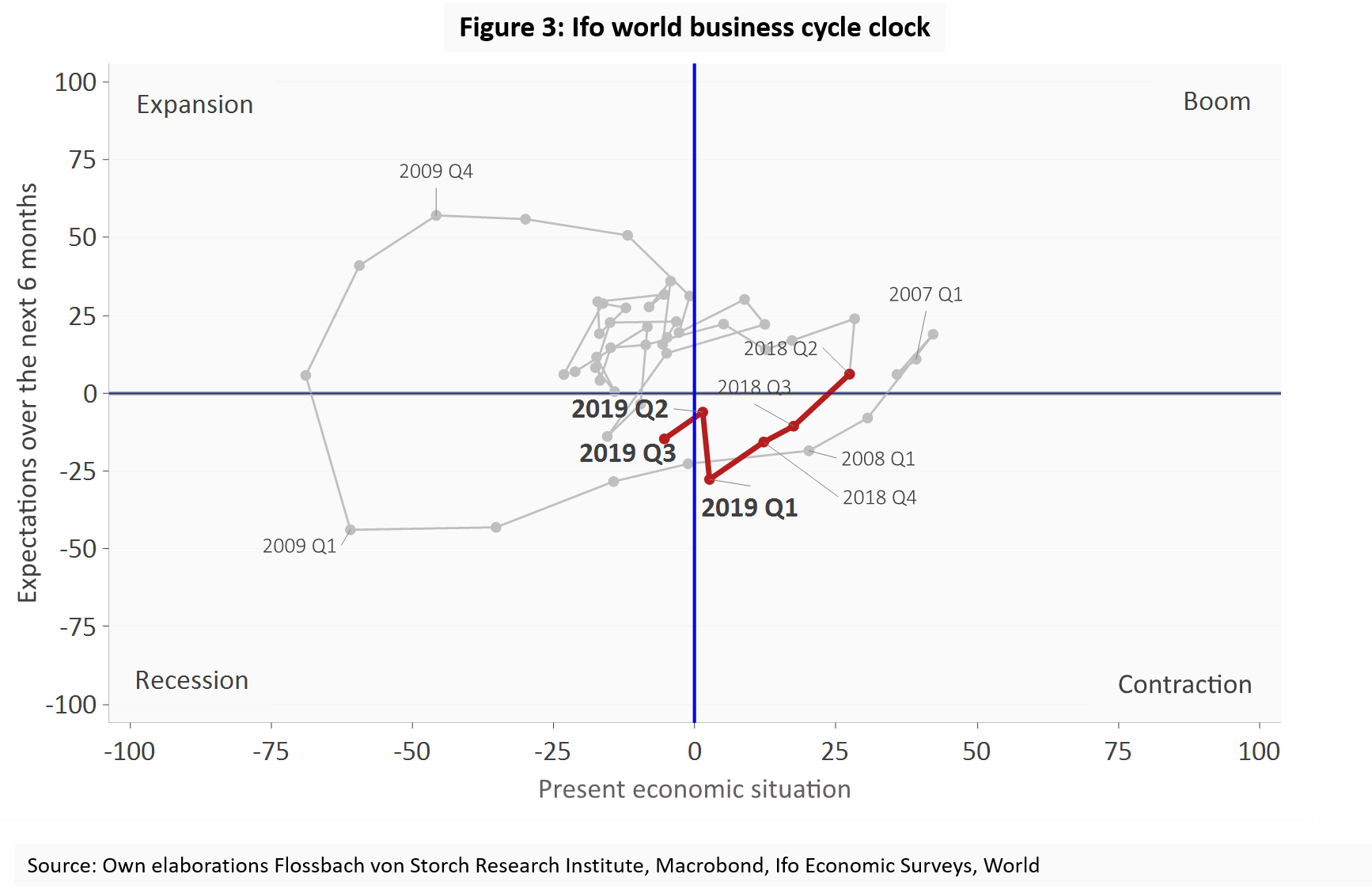

This weakness in trade is clearly reflected in broad economic activity worldwide. The negative impact is not surprisingly borne by the manufacturing sector, which accounts for the bulk of tradable activity. However, services are not unaffected. Although less involved in international trade, the negative impact on services is likely to be driven by the contraction in manufacturing, as services often play a supportive role for the latter. All this is reflected in the declining Purchasing Managers Index (PMI) for the global economy (Fig. 2). Accordingly, the Ifo world business cycle clock – measuring experts’ assessment of the present economic situation and their expectations over the next six months – slipped into recession territory in the third quarter of 2019 (Fig. 3).

However, the main concerns of central banks will regard inflation indicators. Inflation expectations in the major economies have fallen sharply, reflecting the slowdown in economic growth. But also actual core inflation is gradually departing the customary central banks’ confidence intervals.

No one really knows how long the current business cycle will eventually last. But the available signals from the data point to a more sustained economic weakness. This suggests that it is the central bank’s turn to react. But their reaction function will depend strongly on the degree of economic downturn to come. In the first-round of monetary easing, it is plausible that central banks will stick to already tested instruments. However, since the marginal productivity of these instruments is likely to have declined during the last round of stimulus – or these instruments were never particularly productive anyway – other innovative instruments are likely to be implemented in the next step.

Table 1 summarizes the different policy options to be likely implemented in the first step. The common perception of the current central bankers’ view is that there is still space for interest rates to fall. This is clearly the case with the US Federal Reserve, which has managed to lift interest rates to unimpressive but positive 2.5 percent in the last “normalization cycle”. However, this view is also representative of central banks, which are currently confronted with policy rates at or below zero.1

However, due to the broadly acknowledged potential collateral damage of negative interest rates, especially for banks, the need for some compensating mechanisms is often recognized. Some central banks (the Swiss National Bank, the Bank of Japan, the Riksbank and the Danmarks Nationalbank) have already introduced the so-called tieringsystems of interest rates, with the aim to attenuate the burden of negative interest rates on reserves held by commercial banks in the central bank’s balance sheet. It is currently presumed that also the ECB will accompany its broadly expected interest rate cut at the September meeting with some kind of tiering system. It is uncertain which exact design the ECB will choose. It could, for instance, opt for the Swiss model, in which commercial banks’ excess reserves below a certain threshold are exempted from negative interest rates. Or it could follow the system of deposit certificates for excess reserves à la Danmarks Nationalbank. But regardless of the concrete design, the fact that the European banking system is much more heterogeneous than any other of the national systems suggests that tiering in the euro area could be less effective and could, moreover, cause unintended redistributive effects.

Among other unconventional, albeit now standardized, options, central banks could revive quantitative easing (QE). Except for the ECB, there should be no particular restrictions on the size and the composition of assets. In principle, central banks could buy public sector and corporate bonds as well as equities and various categories of exchange traded funds (ETFs), among other financial innovations. For the ECB, QE is more challenging, but not impossible to implement. The strong case for a new QE is underlined by the alleged effectiveness of the past programs. Indeed, in his speech from July 2019, Philip Lane claimed that “(…) the ten-year bond yield would have been around 95 basis points higher in the absence of the APP.”2

However, under the current rules, the ECB is bound by the capital key and emission limits, which are almost depleted with the last QE round. In order to achieve a critical mass of investable assets, either the existing restrictions must be substantially weakened, or – formally less complicated, although more difficult to justify in practice, due to polarized views on that matter – the ECB could decide to extend the pool of eligible assets to equities, ETFs and other asset classes not eligible under the past programs.

Also the parameters of the so called long term refinancing operations (LTROs) – with or without targeting – could be adjusted (the length and the price), to render the refinancing conditions for banks even more favorable than they currently are.3

Finally, there is a certain convincement among central bankers that forward guidance is still a powerful tool for influencing market participants’ expectations. While, on the one hand, the forward guidance could contribute to strengthening credibility of central bank’s action, on the other hand, it itself depends on the credibility of the central bank's overall strategy. The longer it takes for central banks to achieve their policy goals, the more difficult it is for the forward guidance to compensate for the delay-driven credibility losses.

As already anticipated, not all these options are available for all central banks. Central banks being ahead of the “schedule” are likely to activate earlier other, more unconventional measures.

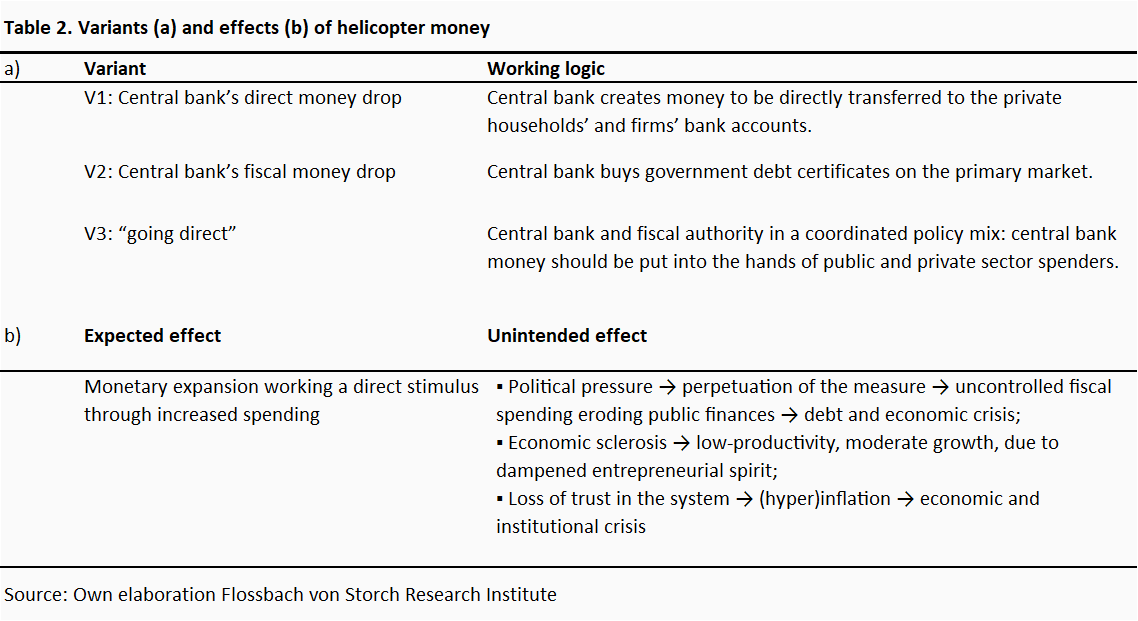

Should the current growth contraction turn into recession and should central banks perceive their policy arsenal as exhausted, the likely next step would be some variant of helicopter money (Table 2).

The idea is not new, originated by Milton Friedman in 1969 more as an intellectual game rather than a real-world application.4 But an increasingly evident helplessness and emergency due to the lack of desired economic effects of monetary policy instruments implemented so far, there is currently a noteworthy revival of the appeal to consider helicopter money as a viable policy option.5 Among the different variants, an approach dubbed “going direct” proposed in a paper issued by Blackrock and co-authored, among others, by former central bankers Stanley Fisher and Philipp Hildebrand, may be the most appealing from a policy-makers’ point of view, given its structured and rule-based design.6 The idea is that:

The major flaw of the proposal is that it is intended to be a temporary, crisis-dependent tool. Experience to date with the entire set of “unconventional” monetary policy tools has shown that this is very hard to achieve. This is more likely in an environment of high indebtedness and political pressure to ensure the solvency of public finances. Moreover, easy access to central bank money would not support the unfolding of entrepreneurial spirits, leading to dampened economic growth. Finally, upon the lack of the expected outcomes, market participants could eventually lose confidence in the system and lead it into an economic and institutional crisis.7

The major central banks are likely to react soon with a new stimulus to counter the current growth contraction and mounting uncertainties in the global economy. One should expect a gradual approach, with well-tried instruments applied in the first place. However, should the growth contraction unexpectedly turn into a full-blown recession, more active and creative approaches will very probably complement the monetary policy arsenal. Helicopter money is the most likely to emerge here. Whether central banks themselves are so far as to admit this could be questioned. But luckily the are known for their extensive creativity.

1 This is confirmed, for instance, by the ECB’s new chief economist Philip Lane in his speech at the Bank of Finland conference on Monetary Policy and the Future of EMU from July 2019, where he states “Our negative policy rate thus contributes substantially to providing monetary accommodation.”

2 See Philip Lane’s speech at the Bank of Finland conference on Monetary Policy and the Future of EMU from July 2019.

3 In March 2019, the ECB launched a third series of targeted LTRO (TLTRO III). It consists of a series of seven TLTRO operations at a quarterly frequency, each operation with a maturity of two years, starting in September 2019. Borrowing rates can be as low as 10 basis points above the average deposit facility rate over the life of each operation, depending on the lending pattern of the participating bank.

4 The idea was taken up again by ex-Fed president Ben Bernanke in 2002, who saw helicopter money as an adequate monetary policy instrument to manage the Japanese economic crisis.

5 The ex-vice-chair of the ECB Vítor Constâncio writes on his twitter account in August 2019: “(…) we need to recognize the limits of monetary policy after 10 years of many experiments. Ever lower negative rates are not a solution. Monetary and fiscal policies collaboration is the way forward, exiting when the inflation goal is attained.”

6 See also „Central banks will need new tools to combat the next downturn”, Philipp Hildebrand in the Financial Times, September 3, 2019.

7 Against this, see Thomas Mayer, „A digital Euro to compete with Libra”, Flossbach von Storch Research Institute, 2 July 2019, for a proposal for monetary reform to allow money creation directly instead of through lending by commercial banks.

16.08.2018 - Society & Finance

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch SE. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch SE remains solely with Flossbach von Storch SE. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch SE.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch SE.

© 2024 Flossbach von Storch. All rights reserved.

Agnieszka Gehringer

Senior Research Analyst

Agnieszka Gehringer joined the institute in 2015. She studied economics at the University of Rome “La Sapienza” and later earned a PhD in economics of complexity at the University of Turin. Since November 2019 she has been a professor of Economics at the Cologne University of Applied Sciences and since July 2016 a lecturer at the University of Göttingen. She has published several articles in academic journals and is an advisor to the EU.

All articles by Agnieszka Gehringer