13.12.2023 - Comments

The Jesuit order could probably be the richest fraternity in the world if it had only held on to its most important shareholding. In the 1950s, they owned 51 per cent of Bank of America. A stake that today is worth around 120 billion dollars. However, the largest shareholders have long been others: first and foremost Warren Buffett's Berkshire Hathaway Holding, a preacher of capital without religious conceit.

But is the world's best-known investor so happy with his package, which represents a good 13 per cent stake in the second-largest bank in the USA? At least the share price performance speaks against it. Bank of America's share price is 40 per cent below its interim high at the beginning of 2022 and, apart from dividends, the share has not earned anything on balance for around six years.

Past share price performance of this kind has no predictive value for the future. Neither are the key figures mentioned here suitable for recommending action in the securities of the banks mentioned. They only represent an excerpt.

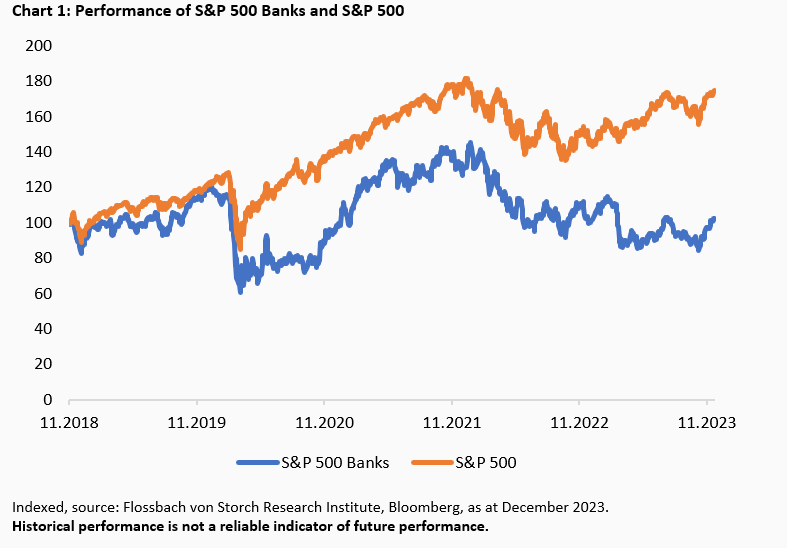

Bank of America is not the only disappointing stock. US banks are generally lagging well behind the market (chart 1).

The development is surprising. According to widespread opinion, banks should actually be the winners of the rapid interest rate hikes by the US Federal Reserve (Fed). Not only should they benefit from the widening of the interest margin (the difference between lending and deposit interest rates), but they can also rake in a healthy and risk-free income from the excess reserves they created during the period of quantitative easing. This is because the Fed is currently paying interest on its deposits at 5.375 per cent. Based on the 3,276 billion dollars recently parked at the Fed, this amounts to a good 176 billion dollars in risk-free income per year if the interest rate remains constant for at least twelve months.

That would actually be a reason to cheer. However, the subdued performance of bank shares indicates that investors are focussing less on the profit and loss account and more on the balance sheet. It is an unfortunate tradition at banks that risks lie dormant here.

One argument for the weakness in Bank of America's share price over the past 24 months, for example, is that it is the leader in a balance sheet item that the International Monetary Fund (IMF) identifies as a key risk indicator (KRI) for banks. This relates to securities that banks book in a special item on their balance sheet: the held-to-maturity (HTM) category.

In addition to the trading portfolio, which is recognised in the balance sheet at fair value, the accounting regulations of the United States Generally Accepted Accounting Principles (US GAAP) provide for two further key categories for the investments of financial institutions: In addition to HTM securities, these are available-for-sale (AFS). Translated: held-to-maturity securities and available-for-sale securities.

AFS investments are to be valued close to market value; any differences between book value and market value are recognised in other comprehensive income (OCI), a subsidiary balance of the traditional income statement. Although the result of this OCI is recognised in equity, it does not initially affect profit. Only when a bank realises an actual plus or minus on the sale of an AFS security does this also become visible in the income statement (so-called recycling).

HTM assets, on the other hand, must be recognised at amortised cost. They only change the equity (and in turn the income statement) of a financial group after a sale. Differences between market value and book value are the rule, so that investors or bank customers find either hidden reserves or hidden liabilities within this category. Although such book losses are not the only danger for a bank or the financial sector, they signal a key risk.

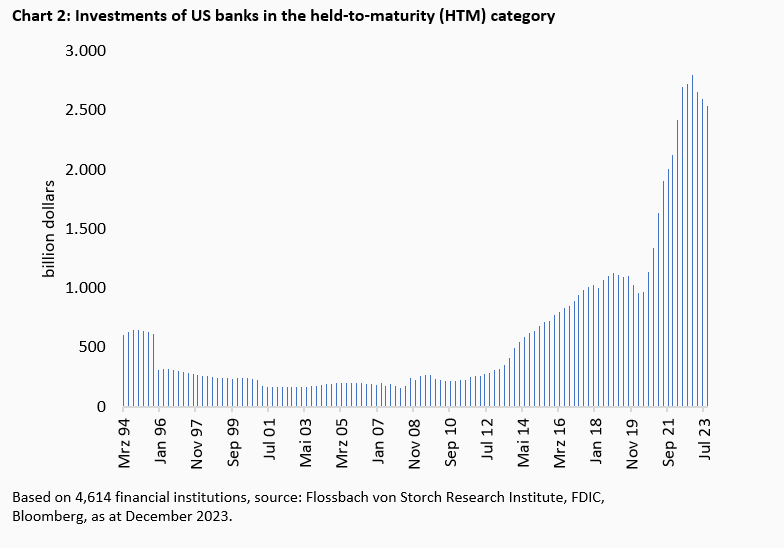

It is striking that since the coronavirus slump on the markets in spring 2020 and the subsequent turnaround in interest rates, US banks' investments parked there have increased to previously unknown levels. According to the latest available data as at 30 September, HTM assets stood at USD 2,540 billion, a good 150% higher than in the summer of 2020. Over 15 years, they have even increased more than tenfold (chart 2).

There is little doubt that the banks' CFOs have taken advantage of the room for manoeuvre in their accounting policies to avoid burdening equity. This is because every change in market interest rates also changes the value of the respective AFS and HTM investments. In the case of held-to-maturity, this change only has an impact on equity when the investment is sold. The temptation to conserve equity by transferring to this category is therefore likely to be great.

Current book losses are mainly due to the rise in interest rates, which has significantly reduced the market value of bonds. In addition, there are weaker credit ratings of debtors, for example, which may also depress market values.

And we are no longer talking about a handful of dollars. Even during the financial crisis, the banks' book losses in the AFS and HTM categories were hardly worth mentioning.

However, the crash on the bond market, which has pushed almost all bond investments in the portfolio down by double-digit percentages, is wreaking havoc on bank balance sheets. It is well known that the three US regional banks Silicon Valley Bank, First Republik Bank and Signature Bank had already failed to weather the storm in the spring.1 In Europe, Credit Suisse Suisse collapsed (for slightly different reasons) and had to be forcibly married to UBS.

However, this may not mean that the problems in the (US) banking sector are off the table. Now that the latest quarterly reports as at 30 September are all available, a gloomy picture emerges, at least at first glance.

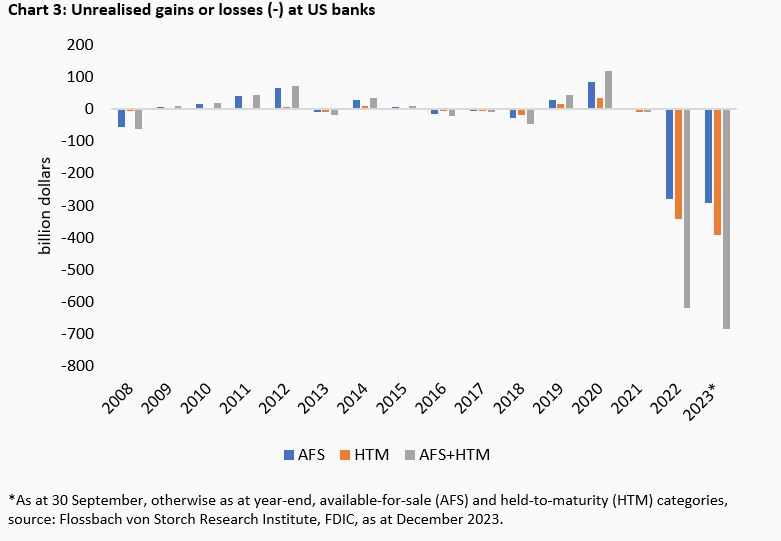

Unrealised losses from available-for-sale and held-to-maturity securities totalled USD 683.9 billion in the third quarter. This was 22.5 per cent higher than in the previous quarter. In the particularly critical HTM category, book losses totalled USD 390.5 billion (chart 3).

The Federal Deposit Insurance Corporation (FDIC) attributes this primarily to "an increase in mortgage interest rates". According to a random sample by London-based Risk Quantum, 63 per cent of US banks in the HTM category recently held mortgage-backed securities. These mortgage-backed securities (MBS) have been widely recognised and feared since the financial crisis, even though their structure may have changed.

The unrealised losses are a burden on future income, as the securities are generally long-term and fixed-interest. The low interest rates on these securities explain the high book losses, which totalled 15.4 percent for HTM securities alone as at 30 September. If the financing costs, i.e. the banks' funding via customer deposits or their own bond issues, do not fall significantly again, this will put pressure on profits.

In turn, losses from the sale of HTM securities - viewed in isolation - reduce equity. This in turn could reduce the capital ratios, which restricts the associated business activities and, in the worst case scenario, calls the authorities into action - if a bank no longer fulfils regulatory requirements.

Now, with more than 4,600 US banks, not every ramification can be recognised. However, the potentially dangerous process is simple. Customers withdraw funds either out of a loss of confidence or in the face of better investment opportunities. If a bank does not have enough cash on hand, it has to sell longer-term investments such as HTM securities. This in turn would cut into the bank's capital base.

But is the "worrying gap" (Wall Street Journal) a major threat in itself?

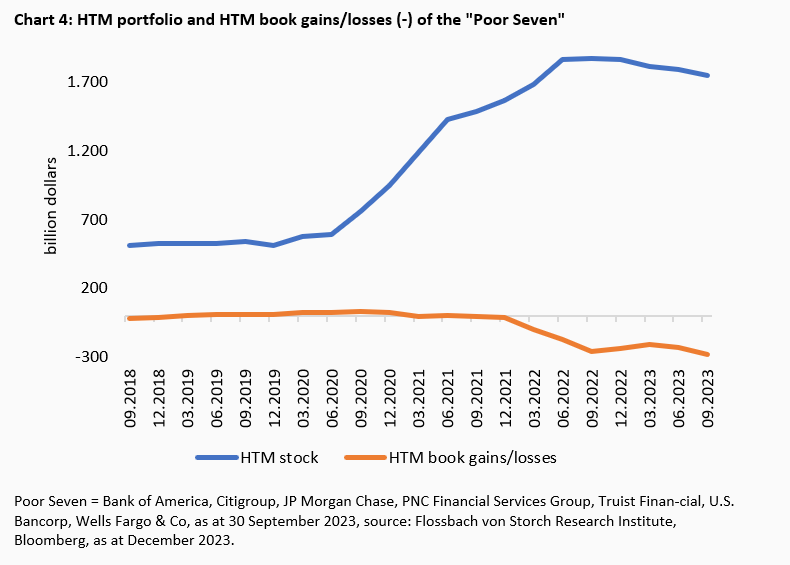

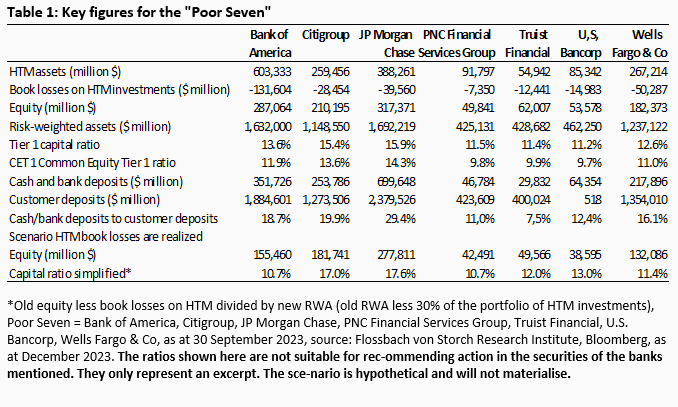

If you dig a little deeper, the first thing you realise is that there is a cluster risk. This is because seven financial institutions alone hold 69 per cent of all HTM securities in the US financial sector. These "Poor Seven" - Bank of America, Citigroup, JP Morgan Chase, PNC Financial Services Group, Truist Financial, U.S. Bancorp, Wells Fargo & Co - account for 73 per cent of all book losses: most recently, this amounted to 285 billion dollars (chart 4).

This hidden burden is in turn unevenly distributed within the Group. As much as 46 per cent of the "Poor Seven's" book losses from HTM securities are on Bank of America's balance sheet. That is 33.7 per cent of all book losses of the 4,614 US financial institutions.

The bank is systemically important. Like Citigroup, JP Morgan Chase and Wells Fargo & Co, it belongs to the List of Global Systemically Important Banks, which are subject to special capital requirements.2

In its 2022 annual report, Bank of America states a minimum requirement for its hard core capital of "at least 9.5 per cent". The general requirement here is to fulfil a ratio of at least six per cent.

This and other capital ratios, such as the somewhat "softer" Tier 1 ratio, in which other equity-like components are added to equity, regularly refer to the ratio to risk-weighted assets (RWA).

The RWA represent the investments of a bank, but only as a section weighted according to the respective risks. A risk can have a weighting of zero per cent (a claim against the Federal Reserve, for example) up to 100 per cent. At zero risk, an investment appears in full on the balance sheet, but not at all in the RWA derived from it.3

Assuming that the "Poor Seven" had to sell all HTM securities at the most recently recognised book losses, this would change the capital ratios. It is also assumed that 30 per cent of the assets sold belong to the RWA.

In the event of a sale, equity would initially fall by the amount of the book losses. If the assumption that 30 per cent of the HTM investments are included in the RWA is correct, their amount would be reduced accordingly in the event of a sale.

The result: in a simplified calculation, Bank of America's capital ratios would decrease, while Citigroup's would actually increase. This is because the assumed reduction in RWA following a sale more than compensates for the relatively small decrease in equity (see Table 1).

In this case, the greater decline in the denominator in the ratio of equity to RWA therefore overcompensates for the equity losses, which are also reflected in the decline in the numerator. Experts then speak of a "capital release". However, the fewer HTM securities are also allocated proportionately to the risk-weighted assets (and are in the denominator), the more sales at a loss would impact the capital ratios.

However, it is likely that a bank would realise significantly lower prices in a forced sale than the current book losses show. How such a cascade of fire sales can drag markets and banks into the abyss has been known since the financial crisis - and was made accessible to a wide audience in the Hollywood masterpiece "The Big Short" (2015).

In addition to capital, a bank's liquidity is also important. In times when customers can trigger a bank run within minutes using a smartphone app or with a few mouse clicks on their PC, it makes sense to keep cash reserves well filled. At Silicon Valley Bank, for example, 85 per cent of deposits were gone within two days.4

Including deposits at other banks, JP Morgan Chase, Citigroup and Bank of America in particular currently have very substantial reserves. Customers could withdraw just under one in five to a good one in four dollars without the three major banks being forced to sell investments (see also Table 1). The situation looks thinner at Truist Financial, for example. However, the conglomerate also offers insurance services and is therefore not directly comparable in terms of its balance sheet structure.

In Europe, banks must regularly apply the International Financial Reporting Standards (IFRS). The IFRS abandoned the concept of HTM and AFS a few years ago.

In addition to the trading portfolio, banks report investments either in the fair value through other comprehensive income (FVTOCI) category or in the amortised cost (AC) category. The former is similar to the AFS category, the latter to the HTM category under US GAAP.

However, it is not easy to identify differences between the book value and market value of ACs. Last summer, the European Banking Authority (EBA) therefore collected comprehensive data with a cut-off date of the end of February. Following fluctuations over the course of the year, interest rates are currently back at roughly the same level as in late winter, meaning that this data is at least still useful as a guide. According to the data, EU banks held €2,240 billion in bonds on their books, 59% of which were at amortised cost and 41% in the FVTOCI category. 5

Book losses in the AC category including hedges totalled 75 billion euros net, without hedges 113 billion euros (equal to gross). Under a "shock scenario" with, for example, the rapid widening of interest rate spreads on euro government bonds, the book losses would rise to a net figure of 133 billion euros, according to the EBA.

Whether banks have to realise their book losses depends on a number of factors. A very significant fall in market interest rates to record lows would be salutary in the truest sense of the word, which is therefore unlikely. Then the book losses would disappear.

In the USA, the banking supervisory authorities have taken steps to guarantee previously uninsured bank deposits and provide liquidity. This has so far prevented further bank runs like the one in spring.

Ultimately, HTM investments are a known risk, so problems that have come under less scrutiny to date could presumably be more dangerous. However, it is also clear that in the event of another major financial crisis, the forced sale of HTM securities below book value would cause additional pain - more than ever before, should this be necessary in the foreseeable future.

However, things could get tight even without a crisis - if interest rates rise significantly above current levels and customers withdraw deposits on a large scale in order to switch them into funds, for example.

2https://www.fsb.org/wp-content/uploads/P271123.pdf

3 The risk weighting for mortgage-backed investments also fluctuates between 0 and 100 %. 0 % is applied to government-guaranteed mortgages, for example.

5https://www.eba.europa.eu/eba-publishes-findings-ad-hoc-analysis-banks-bonds%E2%80%99-holdings

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.