29.01.2020 - Comments

Since mid-January, the coronavirus has been keeping the world on tenterhooks. A city with over a million inhabitants is under quarantine, British Airways has suspended all flights to China and even Upper Bavaria is not immune to the virus. In China, 6,000 people have already become infected and more than one hundred deaths have been reported.

Even stock markets do not appear to be immune to the coronavirus. The Shanghai Composite Index fell by more than three percent within two weeks and prices on the US stock exchanges are also under pressure.

Stock markets are particularly prone to narratives - short stories that convey emotions and values. The image of a deadly virus that spreads at breakneck speed, for which doctors know no cure and from which no one seems safe, is a powerful narrative. A further spread of the virus could also bring public life to a standstill in our country and cause a worldwide recession.

The argumentation sounds plausible, films suggest how realistic such a scenario seems to be, and the news and social media ensure the appropriate distribution. The narrative about the virus ultimately spreads like a virus itself.

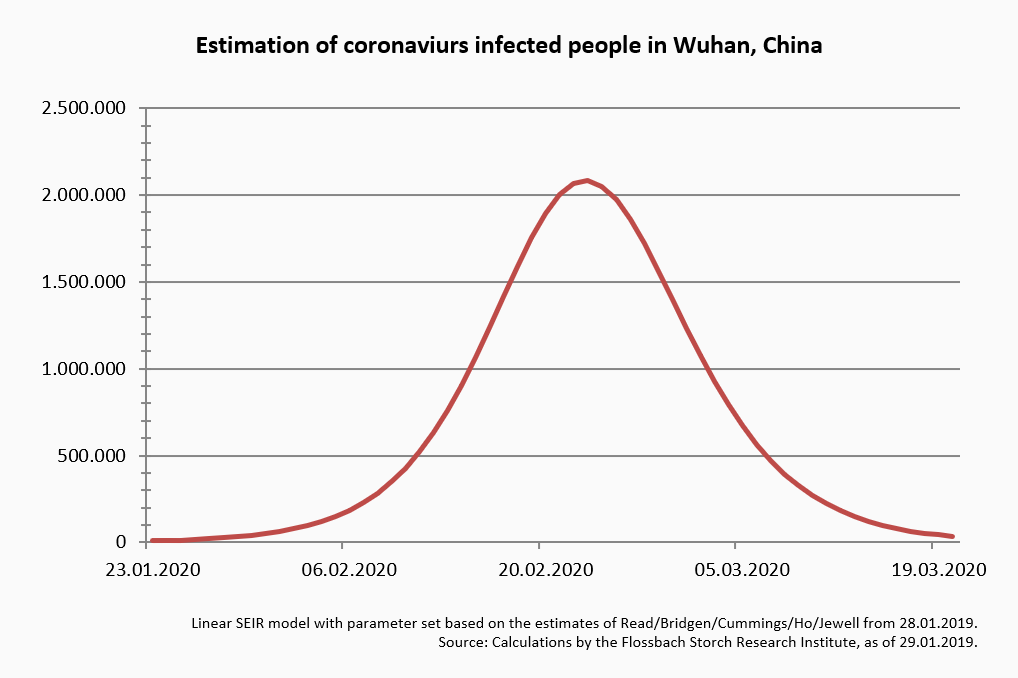

The question arises now as to how long the narrative will continue to have an influence on the stock markets. The further development of the pandemic is decisive for this, as it is the source of media reports. In order to predict the spread of a viral disease, so-called SEIR models can be used and estimated based on the already observed infection rate, incubation period and recovery rate. The model predicts the peak of the pandemic for the end of February. A rapid decline afterwards could then be expected.1

However, it should be noted that model-based forecasts must be treated with caution. Model accuracy and the data base have a high influence on the result and can quickly lead to misjudgements. Preventive measures such as travel restrictions and reduced contact with fellow citizens can also significantly reduce the number of new infections.

Stock markets also reacted strongly to the SARS outbreak in Hong Kong in spring 2003, which was much more likely to be fatal. From February to April 2003, the Hang Seng Index fell by six percent. However, by early summer of that year, when the pandemic appeared to be abating and the media reported significantly less, the Hang Seng Index was already eight percent higher than before the outbreak became known.

The assumption that the coronavirus narrative will also only have a temporary influence on the stock markets does not seem to be far-reaching. In comparison, the wave of influenza in 2017/2018 has cost more than thirty times as many lives in Germany alone as the SARS virus has cost worldwide.2 However, there was no sign of any impact on the stock markets - after all, the corresponding narrative was also missing.

1 Parameter set for the estimation of the SEIR model is taken from Read/Bridgen/Cummings/Ho/Jewell (2020): "Novel Coronavirus 2019-nCoV: Early estimation of epidemiological parameters and epidemic predictions", medRxiv, accessed 28.01.2020.

2 The SARS virus caused the death of 774 people worldwide, while the flu wave in Germany in 2017/2018 claimed around 25,100 lives; cf. WHO and aerzteblatt.de, access: 29.01.2020.

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch SE. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch SE remains solely with Flossbach von Storch SE. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch SE.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch SE.

© 2024 Flossbach von Storch. All rights reserved.