08.03.2024 - Comments

The European Union is pushing ahead with ESG regulation. It has now presented a new regulation that aims to improve ratings for environmental, social and corporate governance.

Rebellion often begins in the provinces. Whether in a small Gallic village ("All of Gaul? No!") or in a 3,800-soul community in the Swabian Alb. In its latest sustainability report, Berthold Hermle, the mechanical engineering company based in Gosheim near Tuttlingen, states: "The direct share of Hermle's turnover from products and services that was achieved with its own ecologically sustainable economic activities in accordance with the current EU taxonomy is 0%."1

Hermle is a fine speciality machine manufacturer that has been listed on the stock exchange for almost 34 years and regularly has to deal with new ideas from the European Union (EU) due to its presence on the capital market. The EU is said to have issued 4,600 directives by now.2 In 2014, there were still around 1,900.

People in Gosheim obviously don't always agree. For example, with the EU taxonomy. It defines which economic activities the EU considers to be environmentally sustainable and therefore contribute to climate targets from an EU perspective.

Hermle considers the taxonomy to be "only of limited significance". The reason for this is that machine tool manufacturing has not yet been directly included in the list of climate-friendly economic activities compiled by the EU Commission. Hermle considers itself an "enabler" that enables its customers to "make a contribution to achieving the EU's environmental goals by using our machines".

It is possible that a new EU regulation of all things could now provide a remedy and put Hermle in the right light. On behalf of the European Parliament and the European Council, their presidents have just signed off on a 140-page paper "on the transparency and integrity of Environmental, Social and Governance (ESG) rating activities, and amending Regulation (EU) 2019/2088".3

It is therefore about regulating ratings according to the three criteria of environment (E), social (S) and corporate governance (G). These are integrated into the EU taxonomy in order - so the theory goes - to achieve further progress in realising the objectives of the Green Deal.

The member states now have 18 months to transpose the regulation into national law. Hermle, for example, could then have itself assessed in accordance with the regulations.

The EU's aim is to make ESG ratings more transparent, comparable and comprehensible in future.4 This implies that they have not been so far.

Among other things, the detailed regulation allows companies to check the data they use with ESG rating agencies. According to the regulation, ESG ratings are to be issued independently of established credit ratings.5

The regulation incorporates the recently issued ESG accounting rules. ESG rating providers are obliged to take into account what is known as dual materiality. Companies are required to disclose the social impact of their business alongside the potential financial impact.6

The fees for the ratings should be fair, appropriate and transparent. The European Securities and Markets Authority (ESMA) should therefore monitor the providers of ESG ratings. To this end, it is to liaise with the banking supervisory authority EBA, the insurance and pensions supervisory authority EIOPA and the Systemic Risk Board ESRB. It can therefore be assumed that not only the business owners of the ESG model will demand more staff, but also the supervisory authorities.

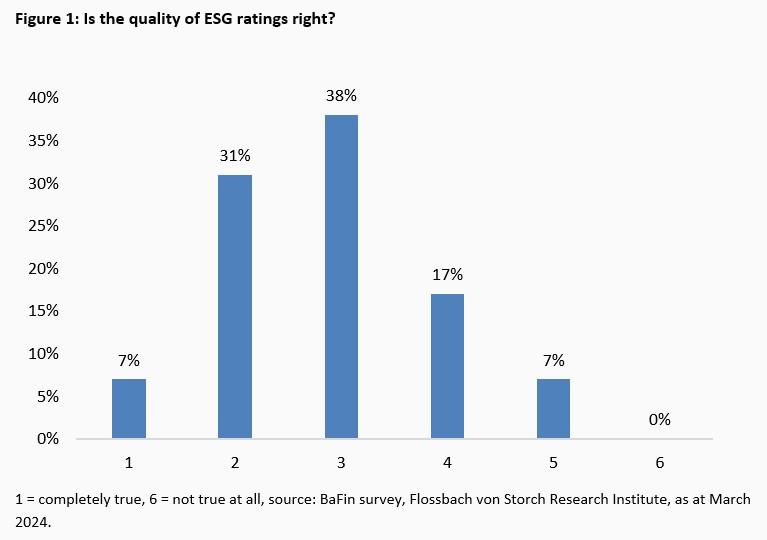

The popularity of ESG topics has already led to the establishment of a large number of rating providers. A study published by the German financial supervisory authority BaFin in mid-February shows that the regulator should keep an eye on fees, concluding that "data and ratings on ESG are expensive and in need of improvement".7

BaFin surveyed 30 German capital management companies (and six ESG rating providers) for its study.8 87 per cent of respondents consider the rating costs to be unreasonably high. In addition, the quality is questioned (Figure 1).

The data on which the ratings are based is also incomplete in some cases and hardly comparable with one another. In addition, they are hardly up-to-date.

This is another reason why the EU is now rushing through the next regulation on ESG. At least that's what it says itself. However, in light of the fact that the originally tough ESG reporting rules have been heavily watered down (companies can opt out and forego ESG disclosures, for example) and the introduction of industry standards has been postponed, a key question arises: to what extent will companies be able to provide consistent and relevant data for transparent and comparable ESG ratings at all?

And even if they do, this does not absolve the investor from doing their homework. Because if they don't, sooner or later they will fall flat on their face. This was demonstrated by the financial crisis at the latest, when investors in droves sank their money or, worse still, that of their customers in securities with a supposed top rating; in securities that could never have been "AAA" according to common sense.

For example, the new ESG rating regulation is driving up effort and costs for companies, making institutional investors' business more expensive and thus their clients' investments more expensive, while the benefits are unclear. Will this additional bureaucracy at least stop climate change?

3 https://data.consilium.europa.eu/doc/document/ST-6255-2024-INIT/en/pdf

5 Regulation Page 21: In order to address risks of conflicts of interests, some activities should be offered from separate legal entities. However, some of these activities could be offered within the same legal entity where the providers have sufficient measures and procedures in place to ensure that each activity is exercised autonomously and to avoid creating potential risks of conflicts of interest in decision-making within its ESG rating activities. Such derogation should not be possible for credit rating activities and for audit and consulting activities.

6 https://www.flossbachvonstorch-researchinstitute.com/de/kommentare/marlboro-man-schlaegt-elon-musk/

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch SE. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch SE remains solely with Flossbach von Storch SE. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch SE.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch SE.

© 2024 Flossbach von Storch. All rights reserved.