10.11.2023 - Comments

The answer to the question of the timing of the next recession in the US is also likely to depend on whether the rivals for the presidency manage to influence the economic cycle in their favour. A recession in the US before the presidential election on 5 November 2024 is likely to benefit the Republican Party in the elections and make it considerably more difficult for incumbent President Joe Biden of the Democratic Party to defend his office. In contrast, an extension of the expansion until after the elections could save Biden's office. The expansive and pro-cyclical fiscal policy of the Biden administration this year (2023)1 and the Democratic Party's demands for the continuation of debt-financed spending programmes are therefore also likely to be aimed at artificially prolonging the current economic cycle in the US or, to put it negatively, delaying an adjustment recession until after the elections.

As the economic stimulus and spending programmes are financed by government debt, the Republicans, with their majority in the House of Representatives, are focusing on limiting further government debt and can refer to the warnings of the International Monetary Fund:

"With the economy operating well above potential and inflation a persistent problem, there is a strong case for greater fiscal restraint in 2023-24. A tighter fiscal stance would lessen the burden on the Federal Reserve in disinflating the economy. A more significant fiscal adjustment will be required over the medium-term to put public debt on a decisively downward path... The sooner this adjustment is put in place, the better."2

If they can force the recession through a restrictive fiscal policy before the elections, this could pave the way for Donald Trump to take the White House.

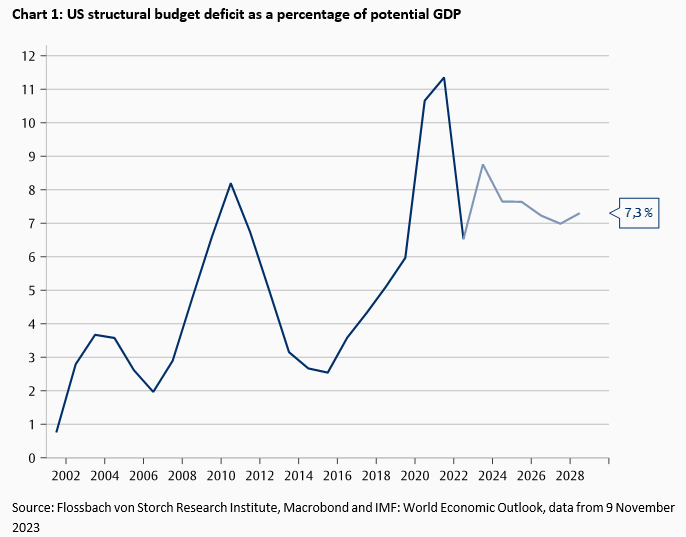

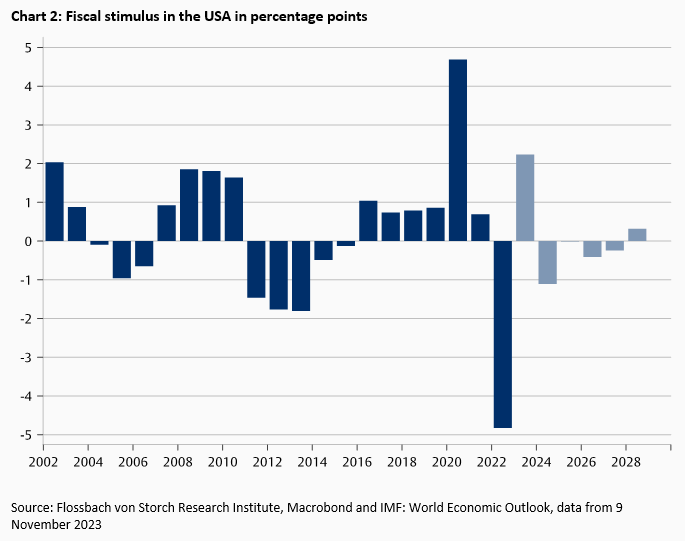

Based on data from the International Monetary Fund, the US structural budget deficit (general government) will rise to 8.8 per cent of estimated GDP in 2023 and fall slightly to around 7.7 per cent in 2024 (see Figure 1).3 While the fiscal impulse that the Biden administration is likely to have generated with its spending policy in 2023 (budget deficit in 2023 as a percentage of GDP minus that of 2022) is probably +2.2, the estimated fiscal impulse in 2024 is likely to reach the negative value of -1.1 (see chart 2).

It is difficult to assess whether the boost from the fiscal stimulus in 2023 will be sufficient to prevent the economy from collapsing before the presidential election on 5 November 2024, as economic development is of course also influenced by other variables, not least the Fed's interest rate policy. As things stand at present, however, the US economy is unlikely to receive a boost in 2024 from further positive fiscal stimulus.

US President Joe Biden would have to add even more debt-financed spending for an economic tailwind created by politics, which he is unlikely to succeed in doing given the Republican majority in the House of Representatives. The current disputes over the US budget could even force US President Biden and the majority of Democrats in the Senate to compromise with the Republicans, which would further increase the negative fiscal stimulus estimated for 2024.

However, there is little agreement within the Republican Party on the extent to which the national debt should be limited. And there is even less agreement within the Republican Party on the compromises that should be made with US President Biden and his Democratic Party in the budget dispute. The deselection of Republican Speaker of the House of Representatives Kevin McCarthy was initiated by the Republican side by radical Republican Congressman Matt Gaetz and justified, among other things, by the fact that McCarthy had gone too far towards Joe Biden on the issue of national debt. However, this accusation by Gaetz, who belongs to a radical group of 10 to a maximum of 15 Republican MPs, was basically directed not only against McCarthy, but also against the large majority of the 222 Republican MPs in the House of Representatives who agreed to both the suspension of the debt ceiling until the end of 2024 and the transition budget agreed until 17 November 2023. From Gaetz's point of view, this looks like electoral support for the Democrats.

However, Kevin McCarthy could only be voted out of office because he and the vast majority of Republicans in the House of Representatives were not helped by the Democrats, with whom compromises on the debt ceiling and the transition budget had previously been agreed. The Democrats also voted in favour of voting out Speaker Kevin McCarthy, although his confirmation in office could possibly have been helpful for a looser fiscal policy in the election year.

Perhaps the Democrats were hoping that they would somehow benefit in the next elections from the chaos caused by Congressman Matt Gaetz's motion to dismiss. However, it remains to be seen whether the negotiations on the budget that will be necessary from 17 November 2023 with McCarthy's successor, the new Speaker Mike Johnson, will be easier and more successful for the Democrats. As the radicals in the Republican party have led their own caucus forward or, from their perspective, driven it forward, the Republicans could now demand even greater compromises on the national debt, which - as mentioned - could further reduce the already negative fiscal impetus for the 2024 election year. As the Republicans would benefit from an economic downturn or even a recession in time for the elections on 5 November 2024, they are likely to feel additionally motivated in their demands for spending and debt restraint for 2024.

Be that as it may, due to many other variables, it remains to be seen whether the efforts of US President Joe Biden and the Democratic Party to postpone an economic slump, let alone a recession, until after the elections, or whether the Republicans' efforts to the contrary will be successful. However, in view of the estimated structural budget deficit for the US up to 2028 (see chart 1), both the Democrats and the Republicans are likely to maintain a structural deficit of between 7 and 8 per cent of gross domestic product in the coming years.

The increase in debt triggered by the expansionary fiscal policy means lower future government debt and spending options in new crises against the backdrop of persistent inflationary pressure and high interest rates. There are already serious warnings that in future crises new aid programmes can only be implemented through renewed monetary financing, accepting new waves of inflation - if at all.4 It is therefore not surprising that the rating agency Fitch lowered the USA's credit rating back in August.

Overcoming the consequences of the high interest rates required to effectively combat inflation is likely to be ahead of the USA, but also ahead of Europe and many other countries. The Fed's interest rate hikes to combat inflation have created an increased need for adjustment in both the financial sector and the real economy. The first effects in the financial sector were already felt this spring in the form of a crisis at regional banks in the USA. It should not be ruled out that further adjustment requirements in other areas of the financial sector will trigger smaller or even larger financial crises in the coming months. As the British financial crisis in autumn 2022, which led to the fall of a government, shows, such crises can break out in places that no one previously suspected.

Adjustment requirements in the financial sector are usually followed by adjustment requirements in the real sector via changed financing conditions. The fact that this causes zombies to disappear from the market and triggers necessary market adjustments and creative destruction is certainly an advantage.

In terms of regulatory policy, however, the question arises as to whether politicians in the US - and this applies equally to the Democrats and the Republicans, but also to the Fed - are at all prepared to allow necessary adjustments and adjustments to the financial and real economy that have been delayed since the financial crisis of 2007/2008. The policies of former (and perhaps future) US President Donald Trump were also not geared towards allowing painful economic adjustments or even an adjustment recession, but rather the exact opposite, as can be seen from the increase in the US structural budget deficit during his term of office from the beginning of 2017 to the beginning of 2021 (see Figure 1). In the current situation, an economic slump, or the onset of a recession before the elections on 5 November 2024 would certainly benefit the Republicans. However, it is doubtful whether the Republicans would really allow a pronounced adjustment recession after winning the elections. Debt-financed economic stimulus and aid programmes for both the financial and the real economy are more likely. The question also arises as to whether the Fed would maintain high interest rates to further combat inflation in the event of a pronounced adjustment recession affecting both the financial sector and the real economy.

As the structural budget deficit and debt levels in the US are historically high, not allowing the necessary painful adjustments in the financial and real sectors would reignite and perpetuate inflation - depending on the extent of the debt-financed rescue programmes in the consumer goods or capital goods sector or both. The US dollar could also come under pressure. In view of the weakness of Europe and Japan, gold in particular could benefit from this.

In terms of regulatory policy, however, it would be desirable for new growth dynamics to emerge through an effective adjustment recession and processes of creative destruction.

But who represents this recovery programme in the USA? A Volcker and a Reagan do not seem to be on the political agenda at the moment, even among the Republicans. And although Jerome Powell has consistently pushed through interest rate hikes to combat inflation, the real challenges in keeping rates on track still lie ahead of him. But perhaps a self-inflicted debt-induced threat to the US dollar is keeping him and the Fed as a whole on a regulatory course. The exorbitant privilege of the US should be worth an adjustment recession.

1 IMF Country Report No. 23/208, May 26, 2023, p. 5: "On a general government basis, fiscal policy is expected to be procyclical in 2023."

2 Ibid., p. 5 and see also pp. 22-25 and Box 6 "Possible Options for Lowering the Federal Debt" on p. 25.

3 I would like to thank my colleague Dr Pablo Duarte for creating the charts.

4 See John H. Cochrane: "What We've Learned About Inflation", in: The Wall Street Journal, August 2, 2023, p. A17.

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.