17.01.2023 - Studies

A company listed on the stock market creates value for its investors if the company pays dividends, buys back shares or the share price rises with a yield that is higher than the yield on the German government bond. If, on the other hand, the yield is lower or the price falls, value is destroyed for investors.

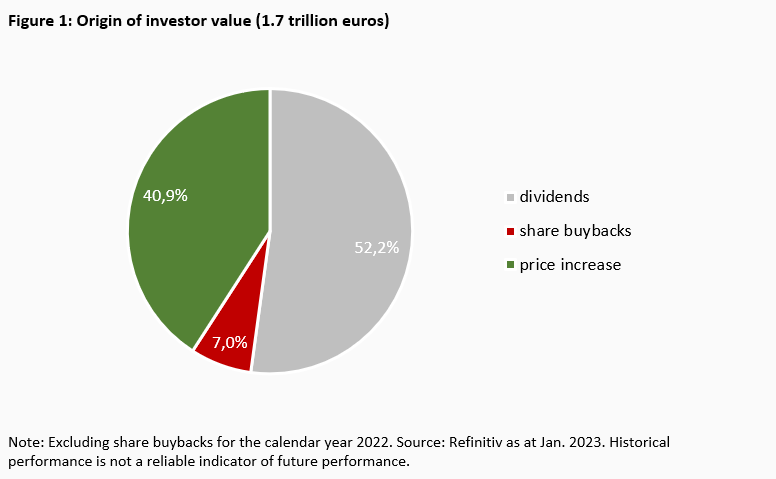

Over the past 20 years, value totalling 1,7 trillion euros has been created for investors on the German stock market. Half (52%) of this was generated through dividends and 7% through distributions via share buybacks. The remaining 41% is attributable to share price increases, which can be explained by higher valuations, profit increases and inflation. In calendar year 2022, almost 400 billion euros of investor value was destroyed by falling prices due to higher interest rates and fears of recession.

The value created over the past 20 years is largely attributable to a small number of shares. Twelve stocks already account for half of the value created. The total value created is already achieved with 118 shares, although there were over 1,000 investable shares in the period. This means that 88% of all investable German equities in the aggregate of all investors made no contribution to value creation, as they created as much value as they destroyed.

The greatest value creation for investors is accounted for by the shares of Siemens, SAP, Allianz, Mercedes-Benz Group and Deutsche Telekom, each totalling over 75 billion euros. Among the biggest value destroyers are the shares of Commerzbank and Hypo Real Estate. The negative frontrunner is the Deutsche Bank share.

The reason for the concentrated value creation on the stock market is the uneven distribution of market capitalisation, as there are few large but many small stocks. The left skew in the distribution of share returns increases the inequality, so that there are few companies whose shares create high value for investors.

For investors, this means that great caution is required when selecting stocks, as there are many long-term value destroyers among the stocks and a few stocks are responsible for a very high proportion of value creation. The selection of shares in a portfolio must therefore be scrutinised regularly. As the investment volume increases, it becomes increasingly difficult for investors to find a sufficient number of value-creating stocks.

This study is a continuation of our study "The risk of the single share" and is methodologically based on the work of Bessembinder (2018).1

The data basis of the study is formed by all publicly traded shares of German companies listed in the Prime Standard or General Standard on the German stock exchange in the period from January 2003 to December 2022. The composition of the CDAX at the end of each month of the period under review is used to identify the individual shares. All information was collected using Refinitiv Datastream.

The starting date of the observation period was January 2003, as this allows the development of the shares to be analysed from a low point on the market. The fall in share prices due to the collapse of the Neuer Markt is not part of the period under review. The individual share time series begin either in January 2003 or with the month in which they were included in the CDAX. In order to minimise the survivorship bias2, all stocks are tracked on Refinitiv Datastream until delisting or until the last available month, even if they are no longer listed on the CDAX.

The data set comprises 142,165 monthly observations, covering 1,013 different shares. On average, there are 140 months per share, i.e. just under twelve years. In January 2003, the data set comprises 739 shares and in December 2022 only 390 shares. Only for 264 shares do the observations cover the entire period in the data set.

For each observation, the total return index (indexed price increase including fully reinvested dividends) and the market capitalisation are calculated at the beginning and end of each month. For shares that disappear from the database within a month, the last available daily value is calculated and set to the end of the month in question so that the development up to the time of delisting is taken into account.

To ensure data quality, all extreme values are compared with the Bloomberg database and corrected if necessary.3 No winsorising4 or truncation of the edges of the distributions is carried out.

In addition, the yield to maturity on German government bonds with a remaining term of one month is used. For months in which no security with a correspondingly short residual term is available, the yield on German government bonds with a residual term of three months is used instead.

The return Rt on a share in month t is calculated as the relative change in the total return index from the end of the previous month t-1 to the end of month t. In this way, dividends are fully included in the return without deduction of taxes.

The calculation of value creation follows the approach of Bessembinder (2018). The value created for investors by a share corresponds to the increase in value for all investors within a month, which exceeds that of a German government bond. Mathematically, the value creation Wt of a share is calculated as the multiplication of the market capitalisation at the beginning of the month Mt-1 by the difference between the share yield Rt and the yield of the short-term federal bond rt .

Wt = M t-1 • (Rt - rt )

If the yield on a share is below the yield on the short-term federal bond, Wt is negative, which corresponds to a destruction of value. The total value creation of a security corresponds to the sum of the value created by all monthly observations of the security.

The value creation Wt includes all dividend payments as well as share buybacks within a month t, as the return Rt is based on the Total Return Index. In the following month, the market capitalisation has fallen accordingly due to past share buybacks and dividend payments, meaning that future returns can no longer influence past value creation.

Market capitalisation and returns are considered in nominal terms and are not adjusted for inflation. As all dividends and share buybacks are recognised as value creation within a month and the future return has no influence on past value creation, it is possible for a share to show positive value creation over a long period of time, even if the share price has recently fallen to a historic low.

There is an inaccuracy in the calculation of the value created as the payment of a dividend or the buyback of shares does not usually take place exclusively on the last trading day of a month. The value created is therefore over- or underestimated by the amount of the dividend or share buy-back multiplied by the excess return from the reporting date to the end of the month.

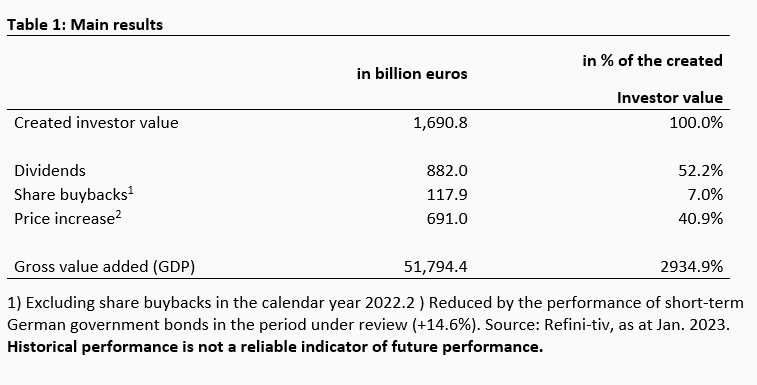

The value created for investors on the German stock market since 2003 amounts to 1.7 trillion euros (1,690.8 billion euros, see Table 1). To get a feel for the size of this figure, it can be put in relation to other figures.

The gross value added in Germany measured by the national accounts for the same period totalled 51.79 trillion euros.5 The investor value created on the capital markets therefore amounts to 3.3% of the nominal value added of all goods and services in the German economy over the same period. However, there is no direct relationship between the two figures, as the value created for investors reflects changes in the expectation of future profits in addition to capital distributions, while gross value added indicates the actual transactions over a period of time.

The total of all dividends paid out in the period amounts to EUR 882.0 billion, i.e. half (52.2%) of the value created. A further 117.9 billion euros (7.0%) was paid out to investors via share buybacks.[1] Direct transactions between investors and companies thus account for 59.2% of the value created. The remaining 691.0 billion euros, or less than half (40.9%), is attributable to the increase in the price of shares (capital gains), adjusted for the cumulative yield on the short-term Federal bond.

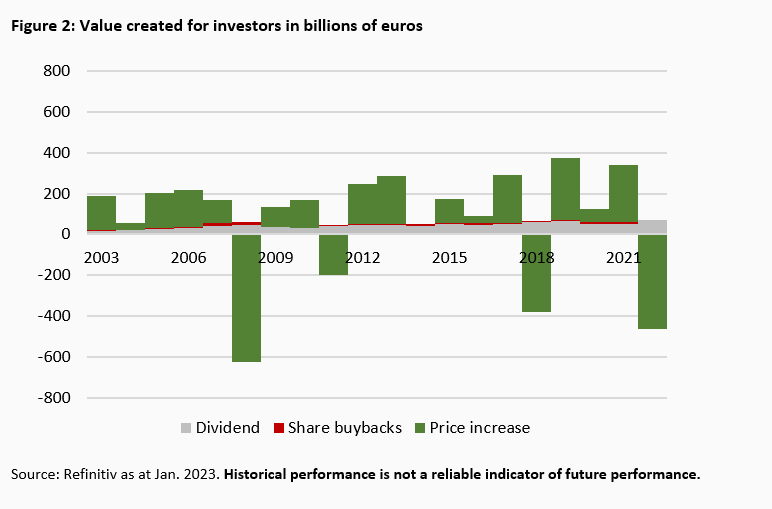

In 16 of the 20 years analysed, value was created for investors on the German stock market (Figure 2). The years of positive value creation show an upward trend. The highest value created was achieved in 2019 at €375.4 billion. The upward trend is driven by various factors. On the one hand, the German economy grew by +2.9% annually in terms of nominal GDP during the period. The CDAX rose at an annualised rate of +8.8% in the same period. In addition to economic growth, value creation for investors benefited from asset price inflation. The European Central Bank's expansive monetary policy in the wake of the financial and euro crisis has led to an increase in newly created funds flowing into the capital markets, particularly equity markets, from 2014 onwards, causing share prices to rise without changing profit expectations due to higher valuations. For investors, this led to value creation, albeit temporary in some cases. Prices and valuations did not fall until 2022, as money was gradually withdrawn from the equity market.

Over the last 20 years, there has only been an aggregate destruction of value in four years (2008, 2011, 2018 and 2022), which was particularly ‑high in 2008 at ‑EUR 561.7 billion due to the falling prices during the financial crisis. ‑For 2022, the value destruction amounted to €-393.9bn, making it the second highest in the statistics. The fall in prices accounted for a loss in value of 464.5 billion euros, which was cushioned by distributions totalling 70.5 billion euros. Higher interest rates and the associated fears of a recession are the main reasons for the loss in value in 2022. Fears of a global slowdown in growth prospects and the increase in key interest rates in the USA were the main reasons for the value destruction in 2018.

The sharp fall in share prices in the wake of the outbreak of the coronavirus pandemic in 2020 led to a temporary loss in value of around € 450 billion in the first quarter of the year. However, as share prices had already recovered by the middle of the year, the value created for investors in the 2020 calendar year was a positive €122.3 billion.

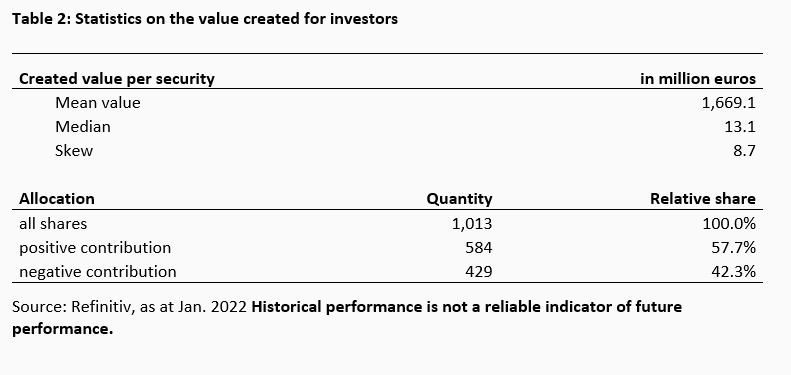

The average value created for investors per share was EUR 1.7 billion (EUR 1,669.1 million). The distribution of the value created varies greatly for the individual shares. The median value created per share is just 13.1 million euros, i.e. only a fraction of the mean value. In fact, only 57.7%, i.e. around six out of ten shares, create value in the long-term. In the period under review, 42.3% of the shares lost value for their investors. This indicates a high left skew in the distribution.

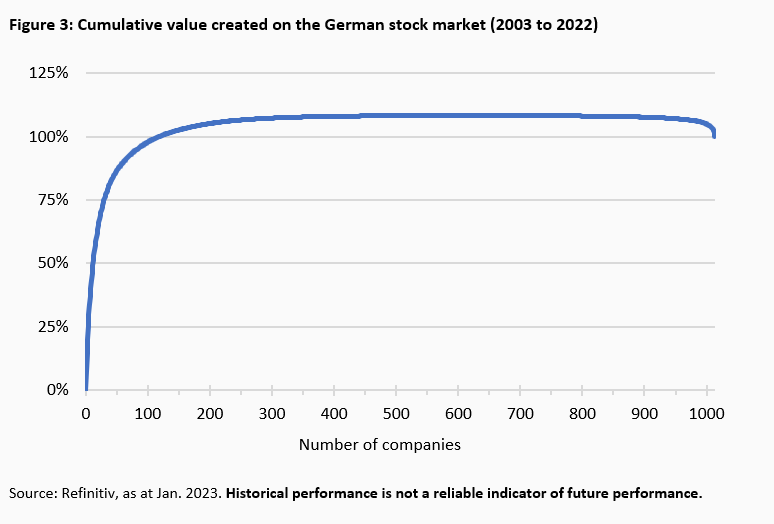

The distribution of value creation is best illustrated by the following graph (Figure 3). All shares are plotted on the horizontal axis in descending order of value creation. The first share has the highest value created in the period, the last share the lowest, which corresponds to the highest value destruction.

The graph of sorted cumulative value creation initially rises sharply, but flattens out sharply at around 100 shares, forming a flat plateau without a visible peak. The high point is reached at the 585th share. With the next 428 shares, the graph initially flattens out slightly. The decline is particularly strong for the last 10 shares. The high point of the chart is 108.6% or 1,836.5 billion euros. The total destruction in value therefore corresponds to 145.7 billion euros.7

Figure 3 illustrates how extremely concentrated the value created for investors on the German capital market is. Just a few shares account for a large part of the total value created for investors. Half of the value created is already accounted for by the first twelve shares. The full value creation, which corresponds to the 1.7 trillion euros discussed, is already achieved with the 116th share. Investing in the remaining 897 shares does not create any added value for investors compared to investing in a short-term federal bond. Although half of these 897 shares make a positive contribution to value creation, the other half equalise this by destroying value. This means that 89% of all shares on the German capital market taken together do not create any added value for investors.

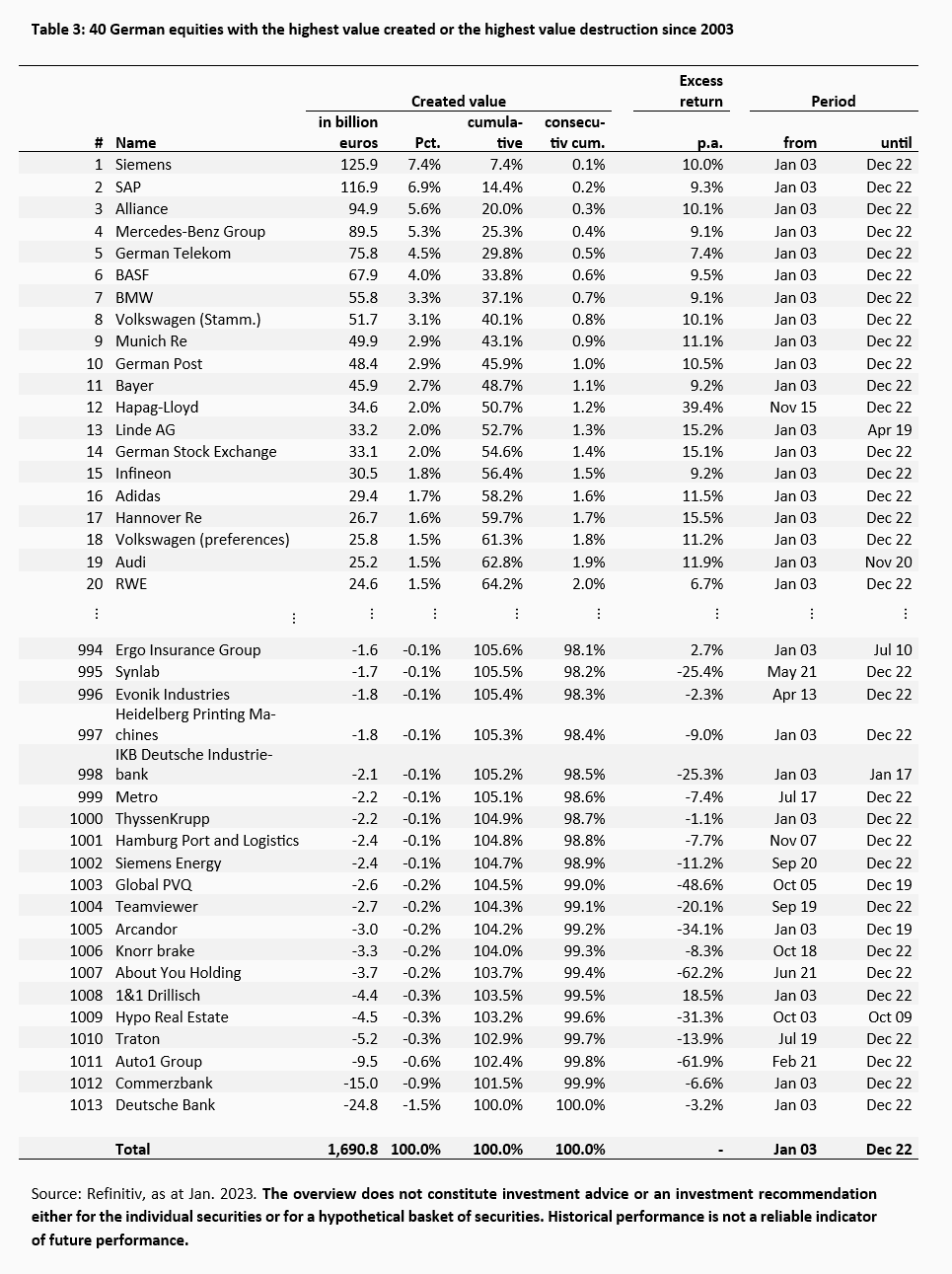

Table 3 below lists the 20 shares with the highest value created and the highest value destruction. As expected, the top 20 include the names of the largest German companies. 17 of the 20 companies have been listed on the stock exchange for the entire 20 years. The sectors are diversified, so that the value created for investors is not attributable to the growth of individual sectors. Column 5 (cumulative) corresponds to the graph in Figure 3, which shows in more detail how extreme the concentration of value creation is. The first three shares (Siemens, SAP and Allianz) already account for 20% of total value creation. To achieve 40% of total value creation, five more stocks are needed and 60% is achieved with a further nine stocks.

The value destroyed for investors over the last 20 years is also concentrated on a small number of stocks, although the concentration is somewhat less pronounced. The value destruction of the last three stocks (Deutsche Bank, Commerzbank, Auto1 Group) roughly corresponds to the value destruction of the other 17 stocks listed. Banks are particularly frequently represented among them. This includes shares of banks (Deutsche Bank and Commerzbank) that are still in business as well as a bank that is now insolvent or no longer listed (Hypo Real Estate, IKB Deutsche Industriebank). The largest loss in value in the last 20 years is attributable to the Deutsche Bank share at -24.8 billion euros.

With the shares of About You Holding, Siemens Energy, Synlab, Team Viewer and Traton, the biggest value destroyers also include companies that have only been listed on the German stock exchange for less than two and a half years. The most recent, prominent insolvency case of Wirecard AG can be found in 938th place. Although Wirecard investors have lost over 23 billion euros in value since the share price peaked in August 2018, this is offset by the share price increases and dividend payments of previous years. In total, the aggregate value destruction caused by Wirecard shares amounts to just under a quarter of a billion euros.

It should be noted that the value created for investors on the German equity market is concentrated on a small number of shares. Almost half of all shares do not create any value compared to an investment in a German government bond. The total value creation is already achieved with 116 shares, as the aggregate increase in value of the remaining shares is just as high as an investment in a German government bond.

The value created for investors on equity markets is the product of the market capitalisation of shares and their excess return. This section argues that the combination of the natural distribution of market capitalisation and the left-skewed return distribution of shares leads to concentrated value creation for investors .

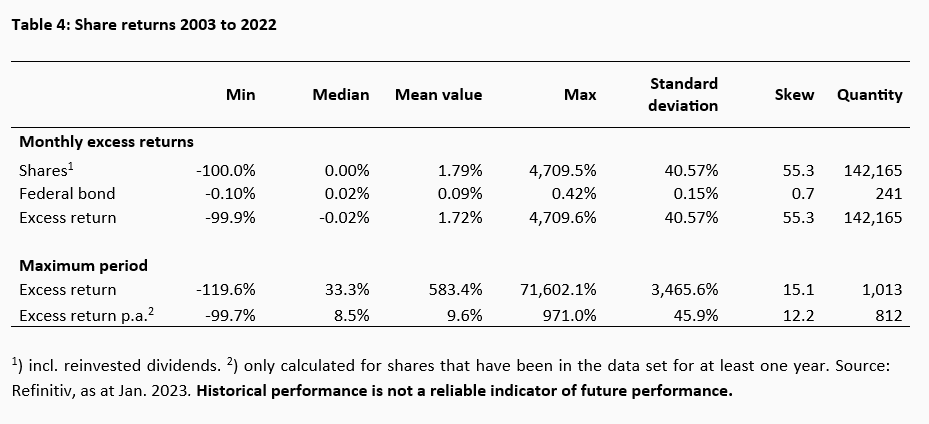

Value is created for investors if the shares they hold generate a return (including reinvested dividends) that is higher than the return on the short-term German government bond. The short-term monthly returns of German equities show a considerable left skew (Table 4). The mean value of the return distribution is significantly higher than the median. Low returns therefore occur more frequently than high returns. The lowest possible return is by definition ‑100%, while the highest return is above 4,000%. The positive skewness coefficient also confirms this statement.

The distribution of yields on short-term government bonds is also skewed to the left. However, the skewness is significantly less pronounced, which is additionally demonstrated by the comparison of median and mean, or minimum and maximum.

The monthly excess return is the difference between the two left-skewed distributions. As the left skew of the monthly equity return is almost 80 times the distribution of the German government bond, the reason for the left skew of the excess return is to be found in the distribution of the monthly equity return, as the skew cannot be equalised by subtracting the two returns from each other.

Next, the distribution of market capitalisation is examined. If the market capitalisation of the shares were evenly distributed over a certain interval at the beginning of the observation period, the distribution of market capitalisation would become left-skewed over time. The left-skewed distribution of returns would result in individual shares developing a significantly higher market capitalisation than others. The resulting investor value would show a high concentration on a few shares due to the skewed distribution of market capitalisation.

Contrary to the above consideration, the empirical distribution of market capitalisation is not evenly distributed. At any point in time, some companies have already had the opportunity to grow over a longer period of time and thus build up a high market capitalisation of their shares. As companies are constantly being bought up or shrinking due to economic failure or even insolvency, there is no point in time when there is an even or concentrated distribution of market capitalisation.

Since the long-term excess returns of a share cannot be considered independently of its market capitalisation due to the path dependency caused by a serial autocorrelation and macroeconomic or sector-specific development, it must still be analysed whether the left skewness of the excess returns compensates for or reinforces the skewness of the market capitalisation.

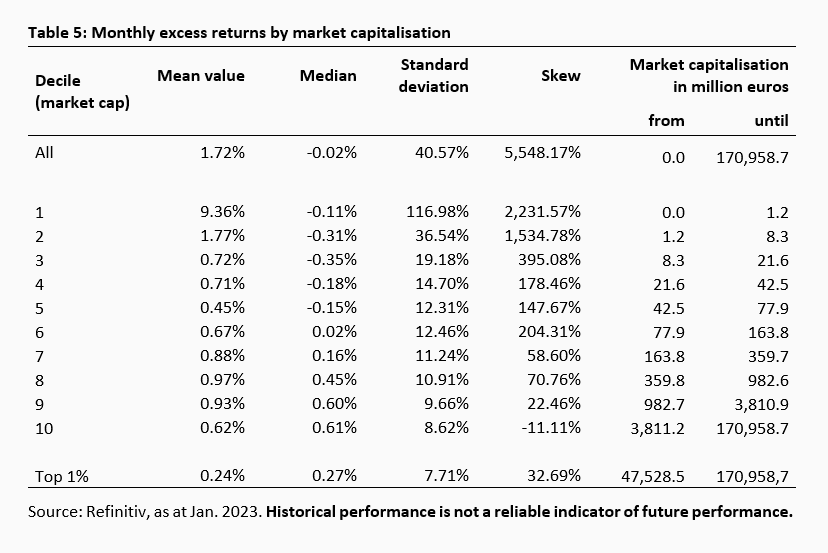

As market capitalisation increases, the skewness in the distribution of excess returns decreases (Table 5). Small stocks generate selectively higher returns than large stocks, as the liquidity of small stocks is often so low that individual purchases already lead to price jumps. With the 10% largest shares, the skewness coefficient becomes negative, which indicates a right skew. For these shares, the rapid growth potential of the companies behind them is often exhausted and there are occasionally major economic setbacks. At the same time, however, the largest 1% of shares show a significant left skew in the distribution of their excess returns. This means that stocks that already have a high market capitalisation are more likely to have high returns than stocks with a slightly lower market capitalisation. This in turn means that the market capitalisation of a few stocks rises very sharply. A small number of shares therefore make a significant contribution to value creation.

The total value created for investors is calculated as the absolute sum of the value created by the individual stocks. Although many small shares generate a high investor value in relation to their own market capitalisation, the value is low in absolute terms. For example, in November 2022, 96% of all shares are needed to reach half of the total market capitalisation. The remaining 4%, behind which there are only 14 shares, make up the remaining 50%. The average excess return of the smaller shares is 16.1% in November 2022, while the return of the largest shares is only 8.6%. The value created is roughly the same for the two groups, but is divided between just 14 shares for the larger shares and 373 shares for the smaller shares. As a result of the compound interest effect, the gap in market capitalisation widens and value creation becomes increasingly concentrated.

A final reason that reinforces the concentration of value creation is the inflation that has occurred over the period. At the end of 2022, 233% more money was circulating in the eurozone than at the beginning of 2003, measured in terms of the M2 money supply. The price level measured by the Federal Statistical Office's consumer price index rose by 48.7% during this period, and by as much as 65.4% measured by the Flossbach von Storch asset price index8. Due to the loss of purchasing power of the euro, a significant proportion of the investor value created is attributable to the younger years and increases concentration.

1 Bessembinder (2018): "Do stocks outperform Treasury bills?" in Journal of Financial Economics, 129 and Immenkötter (2021): "The risk of the individual share", Flossbach von Storch Research Institute.

2 Survivorship bias occurs when time series are truncated before events such as insolvency.

3 Examples of database errors are incorrect positioning of the decimal separator or an insufficient number of decimal places for very small values.

4 Winsorising refers to the transformation of individual data points in order to reduce the influence of outliers on estimates.

5 GDP for Q4-2022 was estimated based on the Bundesbank's growth estimate of +1.8% compared to the same quarter of the previous year.

6 Share buybacks in 2022 were not taken into account in the analysis.

7 Difference between the high of EUR 1,908.6 billion and total value creation of EUR 1,742.1 billion.

8 Based on the longest available period Q1-2005 to Q3-2022, https://www.flossbachvonstorch-researchinstitute.com/de/studien/q3-2022-erster-preisverfall-seit-13-jahren/

03.03.2021 - Companies

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.

Philipp Immenkötter

Senior Research Analyst

Philipp Immenkötter joined the institute in 2014. He earned a degree in business mathematics and a PhD in finance while studying at the University of Cologne. He was a visiting scholar at the University of Pittsburgh. Philipp Immenkötter’s research entails company analysis as well as asset price inflation. He also lectures at the University of Cologne.

All articles by Philipp Immenkötter