24.08.2022 - Studies

"The group" is "visibly in the process of stopping the outflow of funds. And there are now positive effects from the surprisingly strong interest rate increase by the European Central Bank. This relieves Thyssenkrupp somewhat, as pension burdens are thus lower."

It is not known whether Ursula Gather deliberately understated the figures in an interview with the "Rheinische Post" at the end of July or simply had no knowledge of the figures, which the Ruhr group did not present until mid-August. In any case, the head of the Krupp Foundation, a major shareholder of the MDax company, already had an idea of the direction the company was heading. Because the higher interest rates mean one thing above all for a group like thyssenkrupp: balance sheet relief.

The Essen-based company benefits from the fact that it has net cash available after the sale of its lift division a good two years ago and thus does not have to refinance high debts at significantly hig2her interest rates for the time being.

Almost even more important, however, is the balance sheet arithmetic for provisions for employee pensions. Thyssenkrupp provides for just under 96,000 pensioners, and according to the latest annual report, around 158,000 are likely to be added sooner or later.

Since pension liabilities have to be reported at a value discounted at current long-term interest rates, this has only known one direction in recent years: pension provisions have risen with every slide in interest rates.1

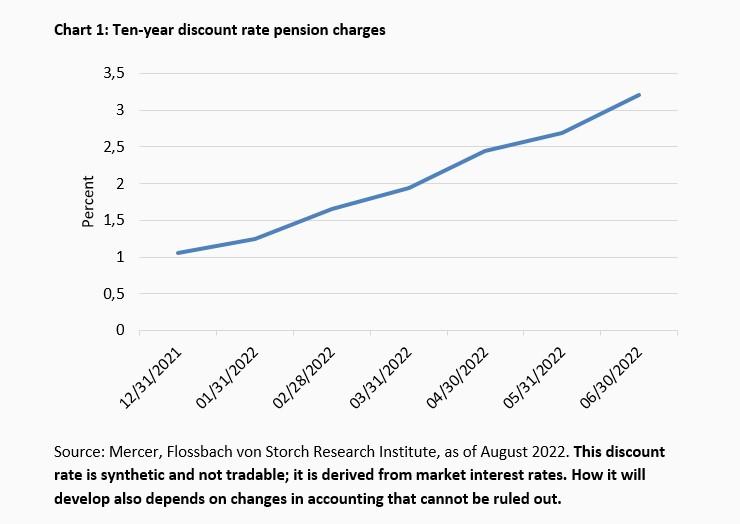

However, the wind has changed this year after interest rates picked up significantly. For example, the ten-year discount rates for pension provisions according to international accounting standards have tripled from 1.06 to 3.21 per cent since the end of 2021 until the end of June this year (Chart 1). Thyssenkrupp and other international companies are guided by such rates in their consolidated financial statements. In contrast, other rates apply to German companies that prepare their balance sheets solely in accordance with the German Commercial Code (HGB) and to individual financial statements prepared in accordance with the HGB.

The effect of higher interest rates is significant. At Thyssenkrupp, for example, the pension burdens in the balance sheet as of 30 June have fallen by almost 1.8 billion euros or 24 percent compared to the end of 2021. This has a positive impact - without taking into account other changes in the balance sheet and profit development.

For example, equity increases when pension costs decrease via the so-called statement of other comprehensive income. Companies prepare this statement for changes in balance sheet items that are not usually reflected in the generally known profit and loss account. In the case of changes in pension provisions, (deferred) taxes are added or deducted when the pension liability decreases.

Ceteris paribus, however, key figures such as the ratio of net financial debt to equity (known as gearing in the jargon) also improve. An important equity ratio such as the price to book value ratio (the proportionate equity to which the shareholder is entitled) should also improve: In this case, it should show a lower value - theoretically assuming a constant stock market price.

Of course, there are numerous other factors that influence the above-mentioned ratios. Shareholders' equity increases with the addition of profits, and decreases, for example, with dividend payments or the repurchase and cancellation of own shares. Price/book values then also change. Gearing increases (= deteriorates) with constant equity and an expansion of debt; it decreases, for example, with the repayment of debt.

The sharp rise in interest rates, however, should in any case be noticeable on the liabilities side of the balance sheet, where companies list their sources of funding from equity, provisions for pensions, for example, and their debts. However, since the majority of companies internationally have no or only low pension burdens, an average view of all members of an index would be less revealing than a concentrated view.

Filtered by companies that reported at least one billion dollars or euros in pension liabilities at the end of 2021, conclusions should be drawn. The reports on the second quarter of this year of the companies of the S&P 500, the Stoxx 600 (converted into euros where necessary, for British or Swedish companies for example) and the German HDax serve as a basis.

Of these, around four-fifths (S&P 500), around half (Stoxx 600) and two-thirds (HDax/100 members) of the companies had reported at the time of the survey, so that the pre-selection comprised around 750 companies (some of which are listed in both the Stoxx 600 and the HDax).

Of these, 59 companies from the S&P 500, 50 from the Stoxx 600 and 22 from the HDax reported pension liabilities of at least one billion euros or dollars at the end of 2021 and also reported these again in the half-yearly financial statements.

In some cases, correspondingly high positions are found at the end of the year, but not every quarterly balance sheet contains information on this again. In any case, 15 per cent of the US companies, around 17 per cent from Europe and 22 per cent of the German companies ultimately fall through the cracks.

This shows: Measured by broad indices, pension burdens play a similar role on the old continent as in the USA, but they play a greater role for companies in Germany.

This is probably due to cultural reasons as well as the comparatively higher number of younger companies in America compared to Germany. Start-ups prefer to entice employees with stock options rather than a company pension.

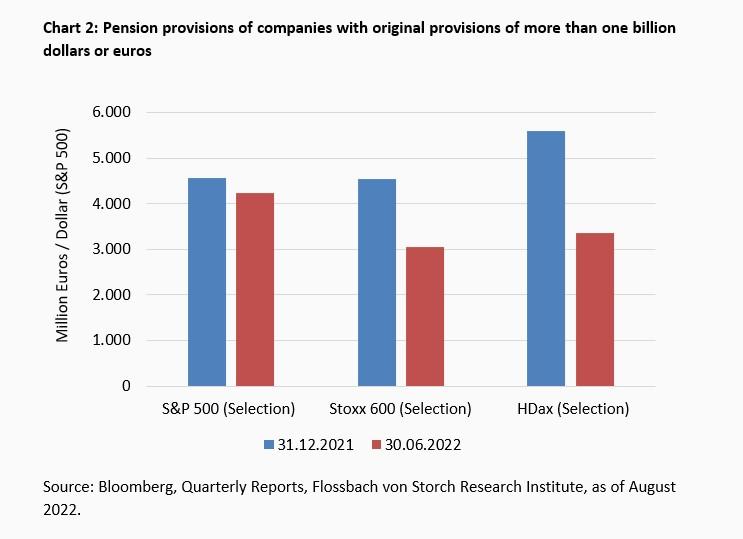

However, the S&P also includes traditional companies with noticeable pension provisions on their balance sheets. At the end of 2021, the average amount of the selected companies' pension liabilities on the balance sheet was 4.56 billion dollars, almost identical (if the current euro-dollar exchange rate of almost 1:1 is taken as a basis) to the selected companies from the Stoxx 600, which at that time had average pension liabilities of 4.55 billion euros. The pension provisions of the HDax companies were a good fifth higher, averaging 5.6 billion euros.

At the most recent quarterly reporting date of 30 June, however, there was a clear change. While at the US companies provisions fell to an average of 4.23 billion dollars, at the European groups they fell to 3.05 billion euros and at the HDax companies to 3.36 billion (Chart 2).

The differences are therefore considerable in some cases. While the provisions of US companies only fell by a good 7 per cent, they fell by almost 33 per cent in Europe and by as much as 40 per cent in the HDax members that fall into the grid.

The difference is primarily explained by the delta in discount rates. While these only increased by around two-thirds in the USA from the end of 2021 to the end of June 2022, they tripled in Europe. Accordingly, the higher leverage lowers the on-balance sheet liabilities more strongly.

However, the discount rate is not the only factor for the amount of the provisions. For example, pension factors or changed mortality tables are included in the calculations. However, these factors are unlikely to have played a role in the short term, so that the interest rate should have clearly dominated as a factor.

The overall effect: within two quarters, the provisions of the 59 US companies have been reduced by a total of 19.5 billion dollars, of the 50 Stoxx 600 companies by about 59 billion euros and of the 22 HDax members by a good 49 billion euros.

If, theoretically, the companies had not made any profits or losses in the period under consideration and at the same time had not made any distributions or share buybacks, and if there were no other factors influencing equity, such as currency changes or price fluctuations in derivatives, then equity would have to have moved significantly upwards. These are theoretical assumptions.

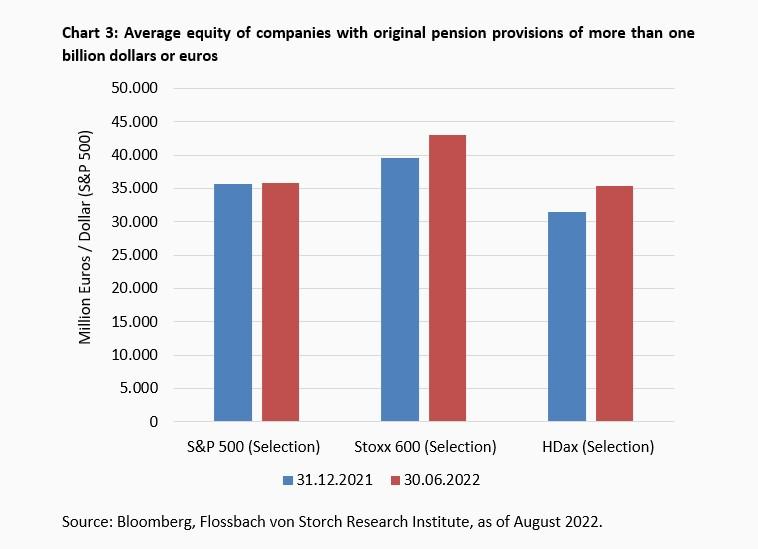

Because in practice, of course, it looks different. Especially for German companies, distributions regularly fall into the second quarter; and US companies are diligent demanders of their own shares. In fact, the equity of US companies has also only gone up by an average of 104 million or a total of a good 6.1 billion dollars. That is an increase of only 0.3 percent (chart 3).

The change in equity capital of the selected Stoxx 600 companies is clearer, with an average increase of almost 3.4 billion and a total of almost 170 billion euros (plus 8.7 percent), which was not only lavish, but also went up by almost a factor of three more than the pure change in pension provisions.

As of 30 June, the 22 selected HDax companies even reported an average increase in equity of almost 3.9 billion euros (plus 12.3 percent) compared to the end of 2021, despite the dividend payment season. Their total equity was a good 85 billion euros higher than at the end of 2021.

Now, it has been shown so far that the reduced pension provisions are apparently reflected positively in equity capital sometimes less (S&P 500 selection), sometimes more (Stoxx 600, HDax selection) - in addition to other factors.

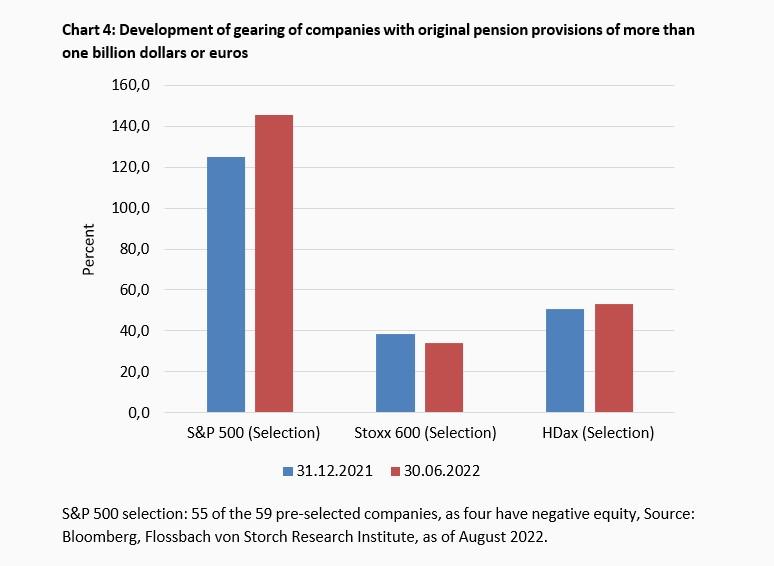

Assuming constant net debt (liquidity), gearing, the ratio of net financial debt to equity, would have to decrease. If this is not the case, then the debt would have increased more than the respective equity capital of the selection.

And indeed, this can be observed in the selected S&P 500 groups and the HDax groups. The gearing rose once from a good 125 to a good 145 percent, and once from just under 51 to just under 53 percent. In the case of the selection from the Stoxx 600, on the other hand, it fell from just under 39 to 34 percent (Figure 4).

A key ratio on the stock exchange is the price-to-book ratio (P/B ratio), which reflects the share (per share) of an investor in the balance sheet equity of his company. Under otherwise unchanged circumstances (no change in the share price over time or on reporting dates), the P/B ratio should decrease, i.e., appear more favourable, if the equity changes positively.

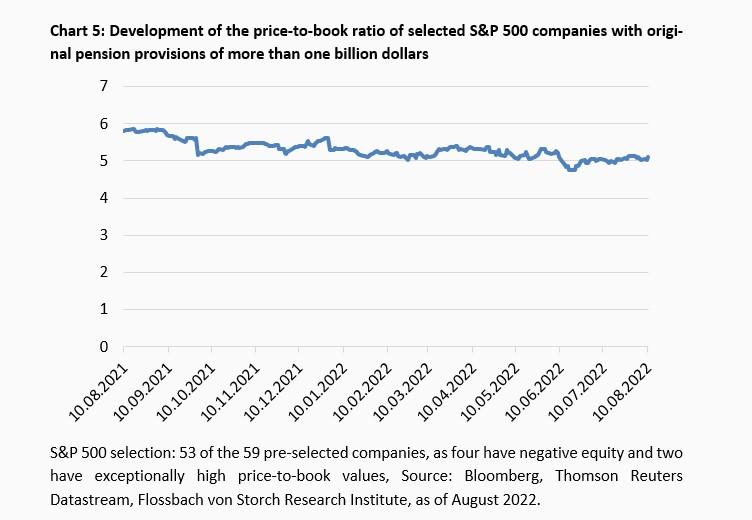

It is true that within two quarters the P/B ratio of the selected S&P 500 companies with high pension burdens has actually fallen, by 6.3 percent from the end of 2021 to the end of June (chart 5).

However, the largest contribution to this was made by a decline in share prices of almost six percent, which is not surprising given the very low average growth in equity capital.

In contrast, the increase in equity capital of the selected Stoxx 600 companies contributed almost exactly 40 percent to the development of the P/B ratio. Here, too, falling share prices did the rest. Over the two quarters, the P/B ratio fell by a total of 22 percent (chart 6).

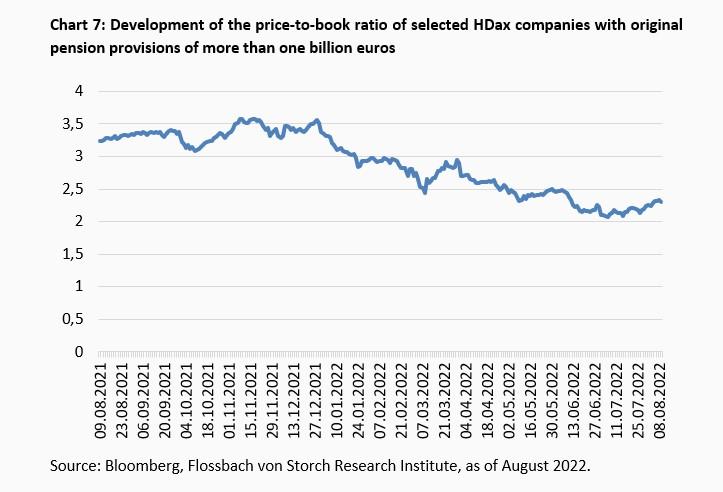

The prices of the selected HDax companies on the stock exchange were under even greater pressure. They lost a good quarter of their value over the period under review. Plus, the increase in equity of more than twelve percent, the average price-to-book ratio fell by more than 37 percent from New Year's Eve 2021 to the end of June (chart 7).

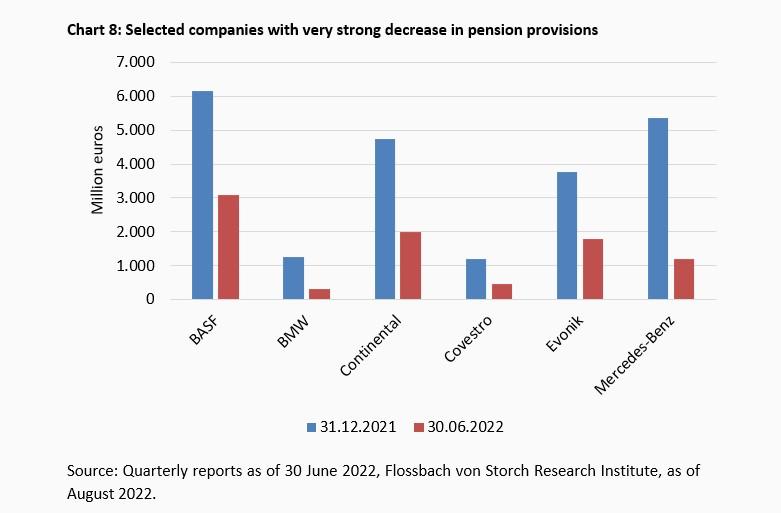

For some companies, pension liabilities have fallen by around or even more than half within two quarters (chart 8).

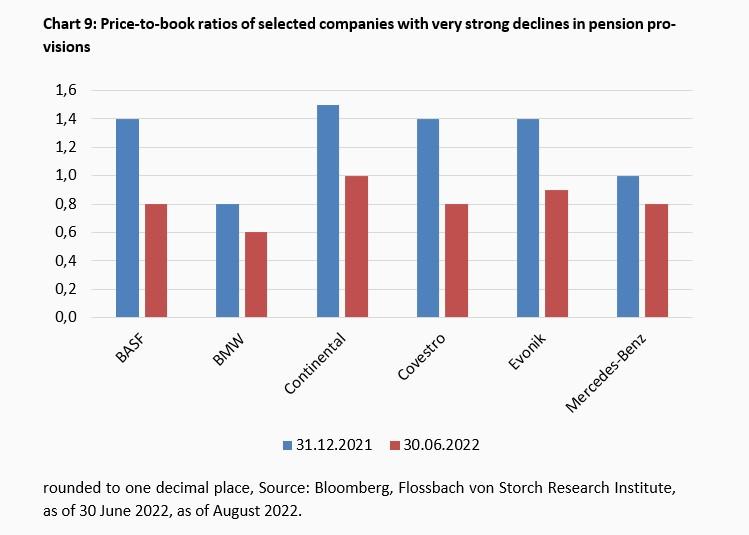

At the same time, share prices fell; equity capital, on the other hand, increased. The effect: the P/B ratio fell to 1.0 or below as of 30 June (chart 9).

The generally significant rise in interest rates has already had a clear impact on companies' balance sheets - for example, in the "heavy" liability item of pension provisions for some companies.

While the higher interest rate level makes refinancing more expensive and could possibly cause one or the other position on the assets side to totter due to overly positive interest rate expectations and result in write-downs that burden equity, the opposite happens with pension provisions - and directly. Their equivalent value in the balance sheet also decreases, but in this case, equity is strengthened with the release of provisions.

For companies with a high exposure to pension provisions, this development is also understandable. In addition to price losses, this explains to a large extent the declining price-to-book ratios of European companies in particular in the course of this year.

On average, these companies also recently reported a lower ratio of net financial debt to equity than at the end of 2021 and, measured against this, are in a much better position than their US counterparts.

Overall, an examination from this balance sheet perspective can be a first approach for a more in-depth analysis of the stock market perspective of individual companies in times of increased interest rates.

1https://www.flossbachvonstorch-researchinstitute.com/en/studies/in-the-interest-rate-trap-dax-30-pension-gap-at-historic-level-1/

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch SE. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch SE remains solely with Flossbach von Storch SE. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch SE.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch SE.

© 2024 Flossbach von Storch. All rights reserved.

Christof Schürmann

Senior Research Analyst

At the Institute since 2022. The graduate in business administration (FH), previously worked as a journalist and deputy head of "Money" at WirtschaftsWoche. The trained banker and book author ("Die Bilanztrickser") taught balance sheet research part-time at the private university BiTS in Iserlohn.

All articles by Christof Schürmann