24.10.2023 - Studies

A 26-minute bike ride to the university auditorium, a fifteen-minute train ride to the Ruhr Stadium and only a few steps to the famous, only slightly infamous "Bermuda Triangle", the city's party mile: the flat in Annastraße in Bochum is ideal for students - and affordable at first glance. The landlord wants exactly 399.91 euros, cold for exactly 52.55 square metres.

The landlord is Vonovia and is not only based in the Ruhr metropolis, but also sponsors the well-known football stadium on Castroper Straße and the local physical education club. This VfL even plays in the first league once again - and is also known to non-football fans at the latest since the setting of Herbert Grönemeyer's work "4630 Bochum".

The ancillary costs that Vonovia charges for the flat deep in the west are also first-class. In Annastrasse, they are exactly as high as the basic rent. That makes a total of 798.82 euros warm - and is better paid by a two-person flat-sharing community than by a hermit-studiosus.

Perhaps it would make more sense for prospective academics to buy one of the properties for sale that Vonovia is also offering. This would be feasible from 58,000 to 163,000 euros, but many of the 42 Vonovia properties for sale in Bochum are rented and explicitly intended for so-called "capital investors". So the average student is rather out of the question.

But what the examples show is this: For Germany's largest housing group with its 618,516 managed flats, 548,080 of which are owned, business is often granular. This ties up capacities at a time when letting is problem-free (Vonovia's vacancy rate is only 2.2 percent), but everything else is more complicated than it has been for a long time. Keywords: energy-efficient refurbishment, rising interest rates, buyers' strike, expropriation fantasies. And that doesn't just apply to Vonovia.

Anyone who wants to look at the status quo and prospects of the German real estate market will find valuable information at listed groups such as Vonovia precisely because of this complex situation, as their transparency is the greatest compared to the numerous closed real estate companies or funds. But even here, an overview is not easy.

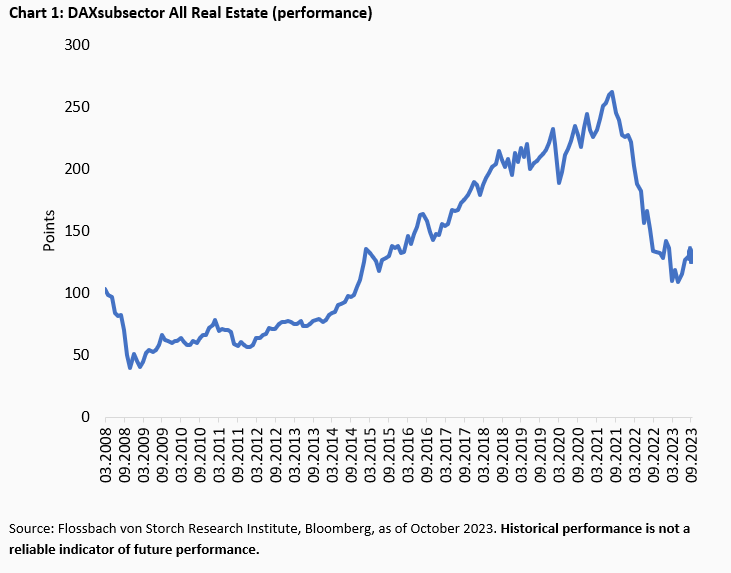

The majority of listed companies are included in the DAXsubsector All Real Estate. Its performance does not necessarily reflect the state of the German housing market, but of course the assessment of investors in residential, office and retail real estate.

Unsurprisingly, the performance of the index reflects the boom and bust of the German real estate market. After a peak value increase including dividends of more than 500 percent from its financial crisis low in 2008, the index has crashed by up to 60 percent since its high a good two years ago. The index has thus erased most of its previous gains and is currently only about a quarter higher than at its start in spring 2008 (chart 1).

However, anyone who wants to describe the state of the market on the basis of its index members encounters difficulties. For example, Deutsche Wohnen, which is known throughout Germany for the expropriation efforts against it, is in the index. However, the free float is only a good 13 percent, the large remainder with competitor Vonovia, which fully consolidates the subsidiary in its balance sheet. Corrections to the index are therefore necessary

In order to avoid double counting of debt, equity or fixed assets in the analysis, companies whose balance sheet items are absorbed into another group must inevitably be omitted, such as Grand City Properties (share 59 percent) or WCM (share of TLG Immobilien: 97.61 percent), which belong to Berlin's Aroundtown. TLG, in turn, will also be merged into Aroundtown (82.39 percent share). In addition, companies such as the auctioneer Deutsche Grundstücksauktionen belong to the index but do not play a role in this stocktaking.

Another problem is that not all companies have current or audited balance sheets. The lack of an audit certificate is not an exclusion criterion for this overview - but it does mean that the figures may be somewhat different (probably less favourable) than they appear in the aggregate.

The German financial supervisory authority Bafin identified several accounting errors during its audit of the 2019 consolidated financial statements of the German Adler Real Estate, a subsidiary of the Adler Group (shareholding 96.9 percent). Among other things, the balance sheet total was overstated by 3.9 billion euros and the overall result by 543 million euros.1

To avoid distortions, small real estate companies with low turnover and less than 500 million euros in gross debt, some of whose data is incomplete or outdated, were also not included. In the end, 16 of 31 index companies remain. These represent around 93 to 94 percent of the revenues and debts of all index companies, taking into account balance sheet consolidations. They are therefore representative.

The aforementioned reciprocal links alone show: Within the industry, people know each other. The fact that they may also help each other is shown by a current 140-page dossier that reports comprehensively on German real estate companies and their alleged practices and that is currently "circulating in the executive suites of the real estate groups and being read carefully", according to an industry observer.

The dossier meticulously lists how value increases were achieved with transactions within the industry in the past - often very quickly, and by moving properties from one company to the next, according to the tenor. In this way, book profits were made in order to improve equity and assets and to make debt ratios appear in a better light for the purpose of obtaining loans. Numerous networks are described and how capital was raised through "equity stories". "Greed" was the dominant theme of the protagonists.

The author is anonymous. By all appearances, it is an insider who is now unpacking his many years of knowledge, which is not unusual in times of low tide. If, on the other hand, business is running like clockwork for everyone, critical insider reports are an exception.

The dossier is about many well-known companies, about round-trip deals also with smaller, unknown companies; it is about celebrities from the boardrooms and politics, and it is described how well-known big banks allegedly made money - for example, when issuing bonds. The remuneration for this was "higher than usual". There is also talk of "self-selling": Cases in which the controlling shareholders on the buyer and seller side are said to have been "almost identical". Offshore transactions also play a role, according to the report.

Some of the cases described there are known from the press. This summer, for example, the Berlin Regional Court partially granted an application by shareholder protectors. A Cologne law firm is now allowed to examine business relations in which the Austrian Cevdet Caner and Adler Real Estate are alleged to have been involved.2

And at the end of June, the public prosecutor's office in Frankfurt and the Federal Criminal Police Office searched more than 20 properties of Adler Real Estate. Among other things, it is said to be about the suspicion of false accounting and market manipulation. Adler Real Estate confirmed the investigation.3

Of course, the presumption of innocence applies to all accusations and descriptions as long as the opposite is not proven. Nor should anyone take this as a recommendation to act in shares, bonds or other securities of the companies mentioned. This requires an intensive examination of the circumstances and figures.

After the Adler Group was unable to find an auditor for the 2022 consolidated financial statements for more than a year, the real estate company has now found several audit firms for the entire group for the "risky mandate" (F.A.Z) in mid-October.

The 140-page report mentions Vonovia's connection to Adler. Here, too, it is public knowledge: Vonovia became the largest shareholder in the Adler Group in 2022 when the Bochum-based company secured a 20.5 percent stake in its competitor by way of a pledge. Originally, there were considerations that Vonovia could even take over the Adler Group completely. However, Vonovia CEO Rolf Buch rejected this idea in the summer of 2022. "The markets have changed, which is why the original idea of taking over the Adler Group is definitely off the table for us," Buch told the financial news agency dpa-AFX at the beginning of August 2022. The Dax company currently still holds 15.88 percent of the Adler Group.4

The real estate deals described in the dossier reach into the present, but some of them date back more than ten years. It is often impossible to reconstruct the cases without internal information, and the sheer mass of the cases allows for random sampling at best. However, since there are parallels to cases that have already been made public, this allows conclusions to be drawn.

And since the real estate industry in general, and also in Germany, is susceptible to not entirely clean practices and money, it can at least be assumed that the problems of unaudited balance sheets and sometimes not very up-to-date figures are more systemic than anecdotal.

In any case, there is no other sector where these deficiencies are so obvious. The extent to which the numerous earlier, possibly dubious deals described in the dossier could lead to surprising devaluations is a matter of speculation. Especially since the information does not necessarily stand up to scrutiny.

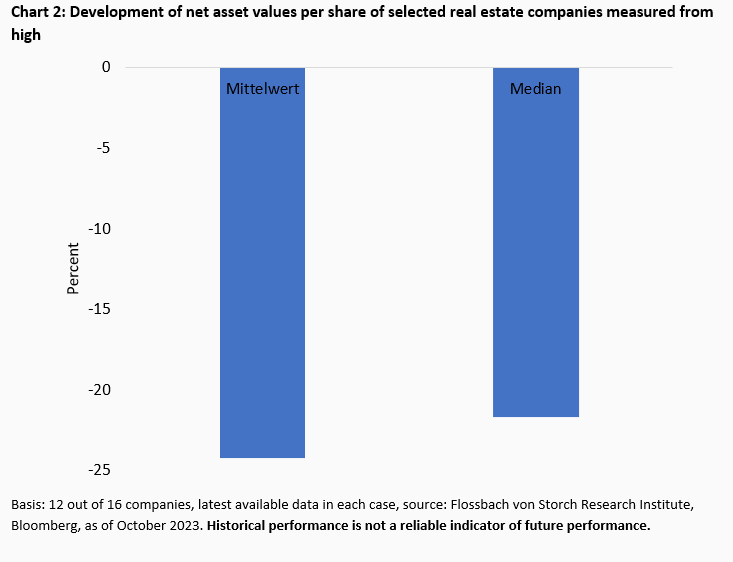

But even the publicly available data show how much pressure the industry is under. Net asset values per share, for example, have fallen by more than a fifth from their high (chart 2).

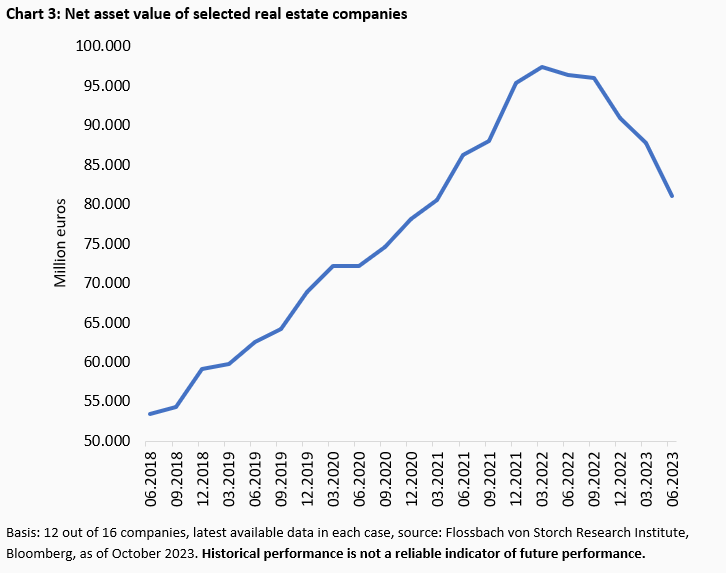

The absolute net asset value (NAV) has developed almost in parallel. This market value of all real estate, participations and other assets less liabilities shown in the balance sheet is still significantly above the level of five years ago (chart 3).

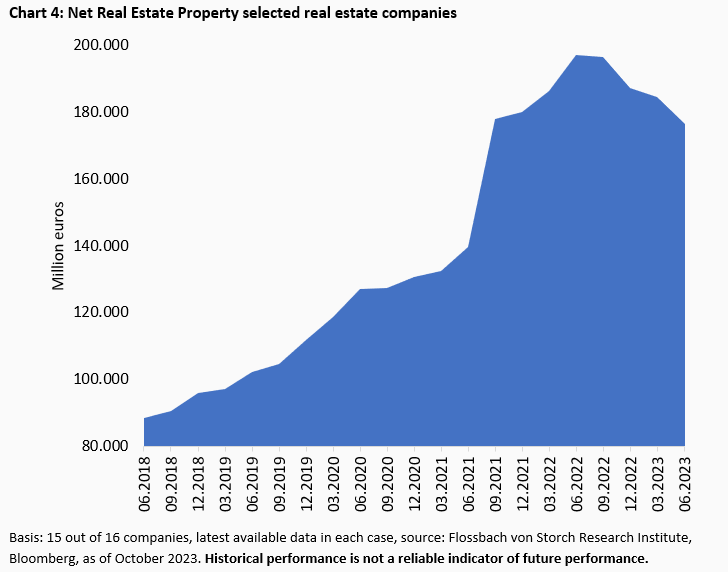

Another substance indicator, the net real estate property (fixed assets after depreciation), is also shrinking. Within two years, it has declined by a good 20 billion euros (chart 4).

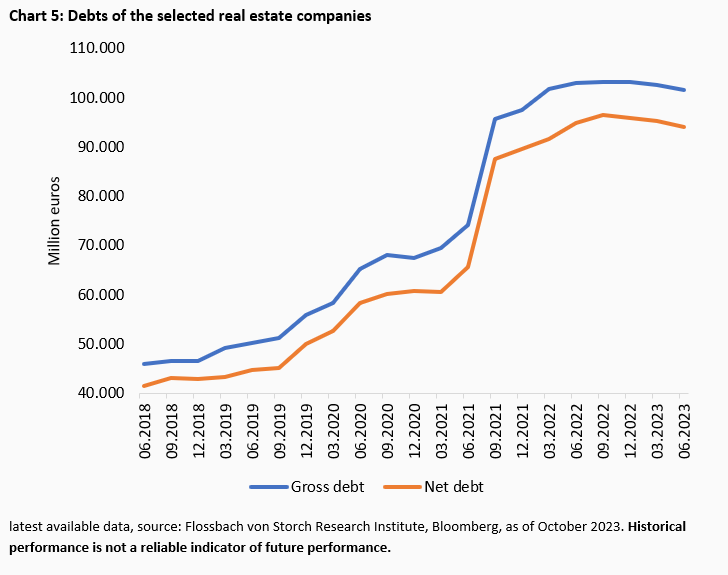

Debt, on the other hand, remains at a high level, well over twice as high as five years ago (chart 5).

High debts are probably more threatening in no other industry than in the real estate sector. Because revenues can only be increased slowly and within limits due to long-term contracts or legal requirements in residential real estate.

The Adler Group, for example, just had to offer 21 percent interest or interest replacement for new debt over two years. The 191 million euro bond, which is rated CCC+, is a so-called "payment-in-kind" (PIK) bond, which has priority in the debt hierarchy over almost all other liabilities of the company. PIK means that investors do not receive the interest in cash but in the form of additional bonds.

By way of comparison: In January 2021, an interest coupon of 2.25 per cent was enough for the Adler Group to collect €800 million from investors for a security with a term of eight years. The individual interest rates have thus increased almost tenfold with a quartered maturity.

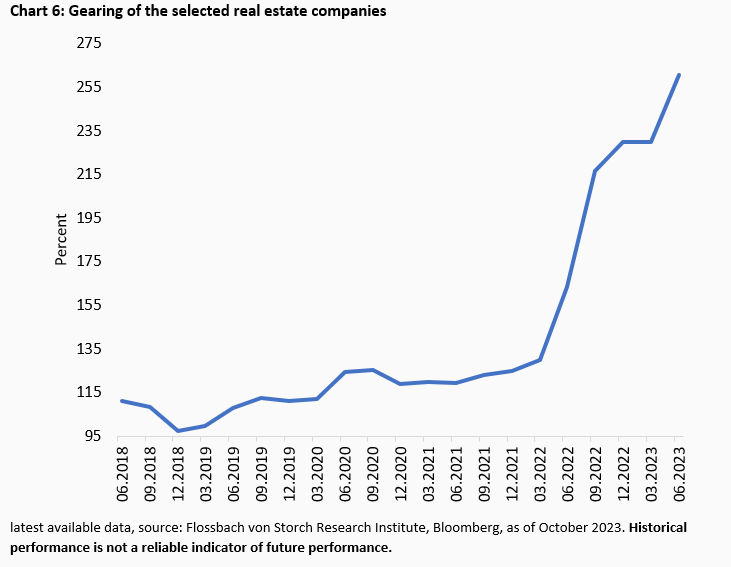

Even if not always so dramatically, all real estate groups are disproportionately affected by the rise in interest rates. Even a blue-chip company like Vonovia, a member of the Dax, would have to offer around five percent interest for twelve months or three years based on the current market level of its bonds, and even more for longer maturities. In contrast, securities from BMW or Siemens, also members of the Dax, yield around or more than one percentage point per year less. A better credit rating could reduce future interest charges. But this is unrealistic for the real estate companies - measured against the status quo. A glance at the so-called gearing, the ratio of debt to equity, shows that this has risen massively since spring 2022 (chart 6).

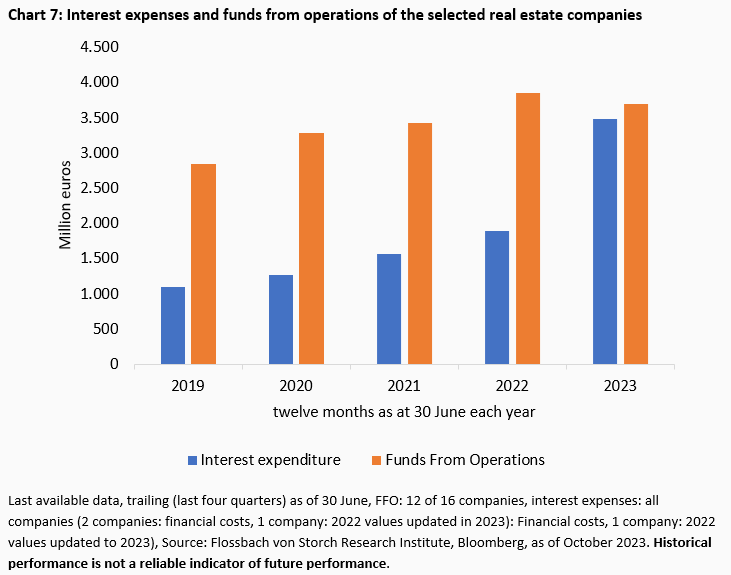

Interest expenses are also already rising alarmingly, while income from funds from operations (FFO) has recently declined slightly (chart 7).

FFO is considered the core indicator for assessing the operating business development (cash flow) at real estate companies. FFO stands for earnings before depreciation, taxes, profits from sales and development projects.

Another metric investors look at is loan-to-value (LTV). LTV is a measure often used by lenders to assess the risk of a loan. In the real estate sector, it corresponds to the ratio between the loan amount and the value of the property in a mortgage or security agreement. Those who privately finance a property know a similar ratio: the mortgage lending value.

Among the selected companies, the LTV was most recently 47.5 percent (both mean and median, basis: 13 out of 16 groups). This is not yet too alarming. However, values of 70 percent and above are considered very high. To qualify as a German REIT (Real Estate Investment Trust), the LTV must be below 55 percent. It should be mentioned that the companies calculate this ratio themselves and the method is not uniform.

Further price reductions in the real estate market would put pressure on LTVs and other ratios such as gearing. There is a lot to be said for this. For example, the sentiment of German real estate financiers, as determined by the analysis company Bulwiengesa, fell to a record low in the third quarter of 2023. The business climate in the sector surveyed by the ifo Institute also fell in September to minus 54.8 points, the lowest level since the survey began in 1991, as the Munich-based economic researchers announced in mid-October.

Financing expectations are assessed somewhat better. However, the German Real Estate Finance Index (DIFI) published in October is still deep in negative territory at minus 33.5 points (plus 4.8 points). However, the increase in the DIFI is purely hopeful: it is based exclusively on a less pessimistic outlook for the coming six months.

It is easy to see from the published profit and balance sheet data that German real estate companies are under massive pressure on average. And this despite the fact that the increased interest rates are far from having fully unfolded.

The prediction that one or the other balance sheet will prove to be no longer additionally resilient and that there could therefore be bankruptcies is not a bold one. Especially since there is probably still one or two skeletons in the closet within the industry - media reports and the somewhat mysterious insider dossier point to this.

In addition, no one can rule out the possibility of a major housing crisis spilling over to banks and savings banks. Particularly in commercial real estate, there are high-volume exposures.5 The big crisis in the real estate market is probably far from over.

1 According to Bafin, Adler Real Estate should not have fully consolidated the subsidiary Ado Properties in the consolidated financial statements, but it did. Full consolidation is not permissible because groups may only fully consolidate associated companies in their annual financial statements if a situation of control exists. The indirect shareholding of 33.25 percent of Adler Real Estate in Ado Properties had not been sufficient for this in the overall view of the agreements concluded until 31 December 2019. The Adler Group had announced that it would appeal the decision. https://www.bafin.de/SharedDocs/Veroeffentlichungen/DE/Pressemitteilung/2022/pm_2022_11_16_ADLER_Real_Estate.html

3 https://www.tagesschau.de/wirtschaft/unternehmen/adler-durchsuchung-staatsanwaltschaft-100.html

4 https://www.adler-group.com/investors/aktie-anleihen/aktieninformationen

22.03.2023 - Economics, Politics & Philosophy

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.

Christof Schürmann

Senior Research Analyst

At the Institute since 2022. The graduate in business administration (FH), previously worked as a journalist and deputy head of "Money" at WirtschaftsWoche. The trained banker and book author ("Die Bilanztrickser") taught balance sheet research part-time at the private university BiTS in Iserlohn.

All articles by Christof Schürmann