27.03.2024 - Studies

The automotive industry is a mainstay of the German economy and has taken a leading position on the global markets in recent decades. Throughout history, open competition has been a constant driver of innovation and an important prerequisite for the development of the industry. In the first two parts of our series on the German automotive industry, we showed how international competition has repeatedly challenged the role of German carmakers. Both the American threat in the 1920s and the Japanese threat from the 1970s onwards forced domestic manufacturers to innovate and improve their products and production processes.

Today, Chinese car manufacturers are forcing their way onto the European market with electric cars and advanced digitalisation at relatively low prices. The development of the Chinese automotive industry is part of China's strategic industrial policy and is heavily subsidised by the Chinese state.

Is competition unfair due to this state support and should it therefore be restricted?

It is conceivable that the European treaties could be interpreted in such a way that competition from China could be considered "unfair". In this case, European foreign trade legislation allows for trade defence measures, such as punitive tariffs, to compensate for competitive disadvantages for European companies. In the case of Chinese car imports, however, protective measures for European manufacturers would preserve existing structures, prevent necessary adjustments, such as those previously made in response to competition from the USA and Japan, and reduce the pressure to innovate. This would result in a loss of prosperity for European consumers.

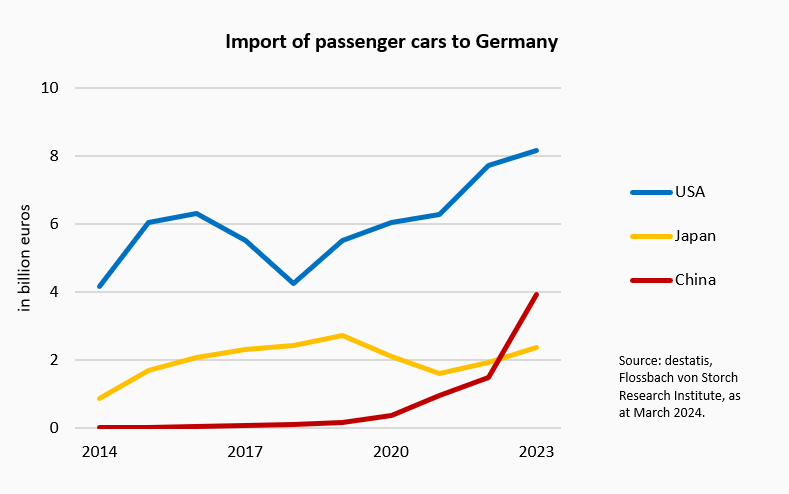

Since 2019, the import of vehicles manufactured in China to Germany has increased rapidly. In 2023, China became Germany's seventh-largest car importing country, overtaking Japan, Korea, Italy and France. From January to November 2023, the value of vehicles imported from China in Germany amounted to EUR 3.7 billion, which represents an increase of 145 per cent compared to the previous year 2022 (EUR 1.5 billion). The reason for the export success of the Chinese car manufacturers is due to the subsidised demand for electromobility. The products of Chinese manufacturers can compete with domestic products in terms of technology and quality but are offered at prices that are significantly lower than what German manufacturers can offer for comparable products.

The development of the Chinese automotive industry is part of China's strategic industrial policy. Since 2009, the development of electromobility has been specifically promoted through research funding, company investments, tax benefits, purchase premiums and concessions for the registration and maintenance of electric cars. There is no certainty about the exact amount of total government spending. According to government sources, only USD 28 billion has been spent since 2009, while other sources (e.g. AlixPartners) estimate that at least USD 57 billion has been spent over a much shorter period of six years.1 The actual amount may well be considerably higher. The manufacturer BYD is estimated to have received at least USD 4.3 billion in subsidies between 2015 and 2020.2 The subsidies in Shanghai even went so far as to make it cost around USD 12,500 to register a car with an internal combustion engine, while an electric car could be registered free of charge.3

German and other European suppliers point to the state subsidisation of the Chinese car industry as an indication of unfair competition to their detriment and derive a claim for protective measures from this. This is perfectly understandable at company and industry level. For the state (at national and EU level), however, the question arises as to whether the economy as a whole would suffer as a result of Chinese car imports.

European consumers benefit directly from cars from China, which are not only cheaper than those produced domestically, but are often of the same quality. The coffers of European countries benefit indirectly when the Chinese state takes over the subsidisation of electric cars, which the European countries would otherwise have to spend on promoting the "drive turnaround" in the automotive sector.

The direct gains for consumers and state coffers could be offset by indirect losses if Chinese manufacturers were to succeed over time in forcing European manufacturers out of the market with subsidised products and securing a monopoly position in the production of electric cars in Europe. In this case, European consumers would pay a monopoly rent to Chinese producers in the long term. Their prosperity would presumably be reduced not only by higher prices for electric cars, but also by the monopolist's reduction in product quality. However, the probability of Chinese manufacturers gaining a monopoly position in the European car market is low. This was clearly demonstrated by developments in the 1920s and 1970s.

The Chinese challenge in the automotive industry is often compared to gaining a monopoly in the production of solar panels. There are fears that European car manufacturers could face the same fate as solar panel manufacturers.

However, there is a significant difference between the two products: solar systems are largely homogeneous goods, while cars are heterogeneous goods. Comparative cost advantages in free trade tend to lead to international specialisation in the production of homogeneous goods. This is not the case with heterogeneous goods. Specialisation takes place within the group of goods, so that the same industry is represented in two trading countries and international exchange takes place within the same group of goods. In economic research, this phenomenon has been the subject of the theory of intra-industrial trade.

The Hungarian American academic Belá Balassa formulated this theory, explaining that the single European market in the 1960s did not lead to specialisation in the production of goods from different industrial sectors, as expected by traditional foreign trade theory. This did not lead to Germany specialising in the production of cars and France specialising in agricultural products and the exchange of foodstuffs and cars between France and Germany. Instead, German and French car manufacturers specialised in satisfying specific customer requirements for this heterogeneous good, so that cars continued to be produced in both countries and German cars were supplied to France and French cars to Germany. The winners were the consumers, who were able to choose from a greater variety of products, and the companies, which were able to generate economies of scale in the manufacture of differentiated products.4

The risk of Chinese electric cars taking market share away from European suppliers is real insofar as European manufacturers of cheap electric cars will have a hard time. However, European customers will benefit, while European manufacturers can find their place in higher-quality products that are better suited to European tastes.

As desirable as it would be to have learned the lessons from history with American and Japanese manufacturers, it is unlikely that this will happen when dealing with the Chinese challenge. The mentality of protectionism and industrial policy has become too deeply entrenched in politics and public opinion. As a result, both the European and Chinese car industries are on the hook for state subsidies and there will probably be a subsidy race in the production of electric cars.

Government subsidies for the German automotive industry are manifold. Companies reporting in accordance with IFRS are obliged to disclose information on the grants and other subsidies they have received from the public sector. However, this does not include various types such as tax relief for consumers and purchase premiums, as they are not paid out to the companies. Nevertheless, they incentivise purchases, which means that government money flows indirectly to companies. Similarly, the state does not treat the costs of maintaining cars with different drive systems in the same way, which also creates purchase incentives and indirectly subsidises them. In a broader sense, this also includes the subsidisation of photovoltaic systems in private households, as they provide an incentive to maintain e-cars more cheaply.

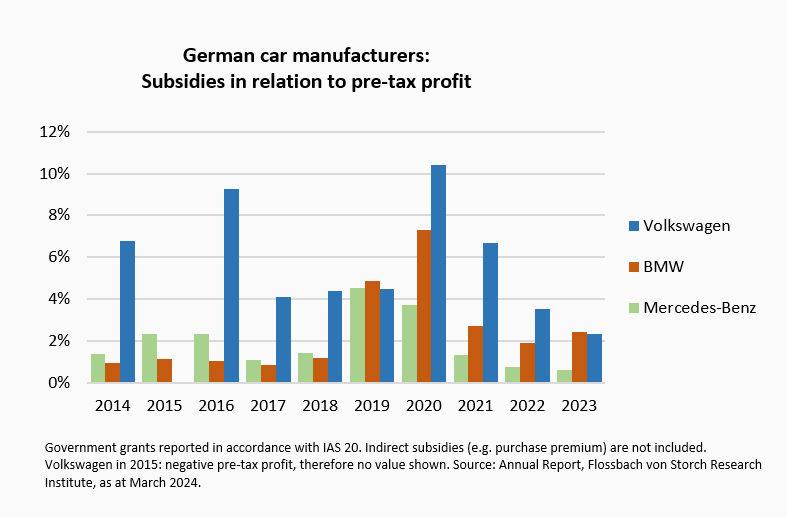

Over the past ten years, the Volkswagen Group has reported receiving subsidies totalling €8 billion, BMW €2.5 billion and the Mercedes Benz Group €1.9 billion.5 This means that the direct subsidies for Volkswagen appear to be on a par with the direct subsidies from the Chinese government for BYD, currently the world's best-selling manufacturer of electric cars.6

In comparison to pre-tax profit, the subsidies, which are also supported by coronavirus aid, even reached over ten per cent of pre-tax profit for BWM and Volkswagen in 2020. For Volkswagen, direct subsidies alone amounted to five per cent or more of pre-tax profit in all the years under review.

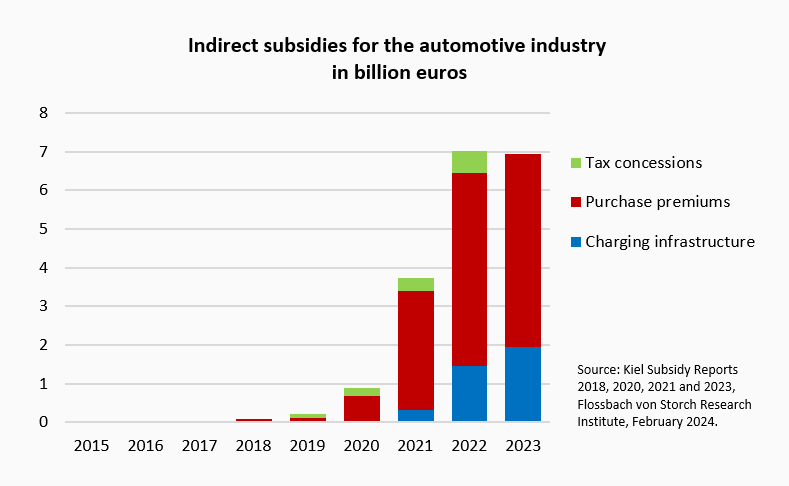

The figures published by the companies only include direct subsidies. Indirect subsidies such as the environmental bonus for the purchase of electric cars and plug-in hybrids are not included in the statistics. However, this type of subsidy from the German government has been very high in recent years.

According to the Kiel subsidy reports, the German state paid subsidies totalling €13.9 billion for the purchase of an electrically powered vehicle from 2016 onwards and invested €3.7 billion in the development of a charging infrastructure. Tax breaks related to the automotive industry have totalled €1.2 billion since 2015. The subsidies have increased particularly sharply since 2021 due to the purchase premiums (environmental bonus).7

In total, the German government subsidies that can be allocated to the automotive industry since 2010 amount to 31 billion euros.8 Combined with subsidies that served upstream and related industries, as well as subsidies paid by other state institutions (e.g. the EU or other EU member states), it can be strongly assumed that, despite possible double counting, the final subsidy amount is significantly higher. At the same time, it should be noted that these funds were not paid out exclusively to German manufacturers, as Chinese manufacturers, for example, were also able to participate in the purchase premium for electric cars.

From an economic perspective, it would be costly for the economy as a whole to protect the European automotive industry from Chinese competition through subsidies or tariffs. The protective measures would preserve existing structures, prevent necessary adjustments, such as those previously made in response to competition from the USA and Japan, and reduce the pressure to innovate. This would result in a loss of prosperity for European consumers.

Concerns about the destruction of the German automotive industry by Chinese manufacturers are unfounded. Even in the 1920s and 1970s, the supposedly overpowering foreign manufacturers took market share from German carmakers and caused consolidation but did not fundamentally jeopardise the German automotive industry.

The right response to the new competition from electric cars from China is to reduce bureaucracy and regulation. Nevertheless, it is unlikely that the European Union will allow competition from the Far East unhindered. The mentality of protectionism and industrial policy has become too deeply entrenched in politics and public opinion. As a result, both the European and Chinese car industries are dependent on state subsidies, and it is likely that there will be a subsidy race in the production of electric cars.

1 Cf. MIIT (Ministry of Industry and Information Technology of the People’s Republic of China) and AlixPartners

2 See Rhodium Group

3 See AlixPartners, 30.12.2021

4 So, the young teacher in Germany could drive a Citroen 2CV at a good price and the seasoned intellectual a Peugeot or Citroen DS21, while the quality-conscious French worker could opt for a VW Beetle and the businessman for a Mercedes.

5 Figures include mandatory disclosures on government grants and other government assistance in accordance with IAS 20. See the companies' annual reports for 2013 to 2022.

6 For the years 2015 to 2020, only the reported subsidies for Volkswagen amount to EUR 4.3 billion and are therefore at a comparable level to the estimated subsidies of USD 4.3 billion for BYD in the same period.

7 See Kiel subsidy report for 2018, 2020, 2021 and 2023. The values contained therein for 2022 and 2023 are only target values, so that the amounts actually paid out may deviate downwards.

8 It should be noted, however, that double counting cannot be ruled out with certainty.

05.12.2023 - Companies

by Philipp ImmenkötterMarius Kleinheyer

15.12.2023 - Companies

by Philipp ImmenkötterMarius Kleinheyer

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.