26.06.2019 - Studies

According to the standard textbook view, a negative impact of “trade wars” on growth occurs mainly through lower trade volumes, higher domestic prices and thus lower consumption and investment. Looking at the US data, there is some evidence for these direct effects, but they are small. More serious is the collateral damage of the “trade war” on confidence.

Direct effects of the US-China trade war

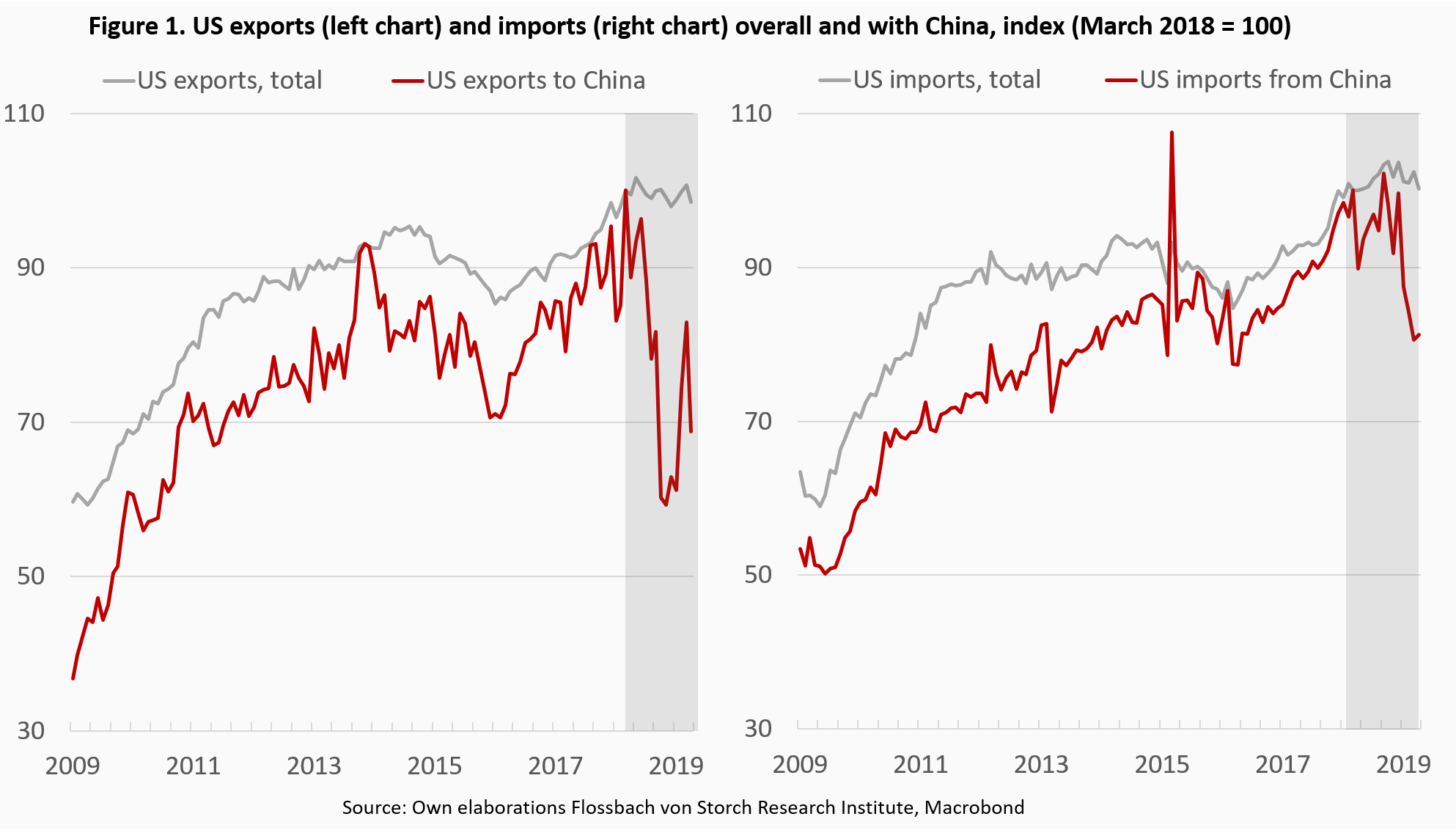

Trade flows between the US and China have slowed significantly since the “trade war” began in early 2018. However, this had only a minor impact on overall US trade flows (exports and imports), which remained relatively stable over the same period (Fig. 1). Finally, the direct growth impact from the change in trade flows is negligible, as the contribution of net exports to GDP growth is relatively small.1

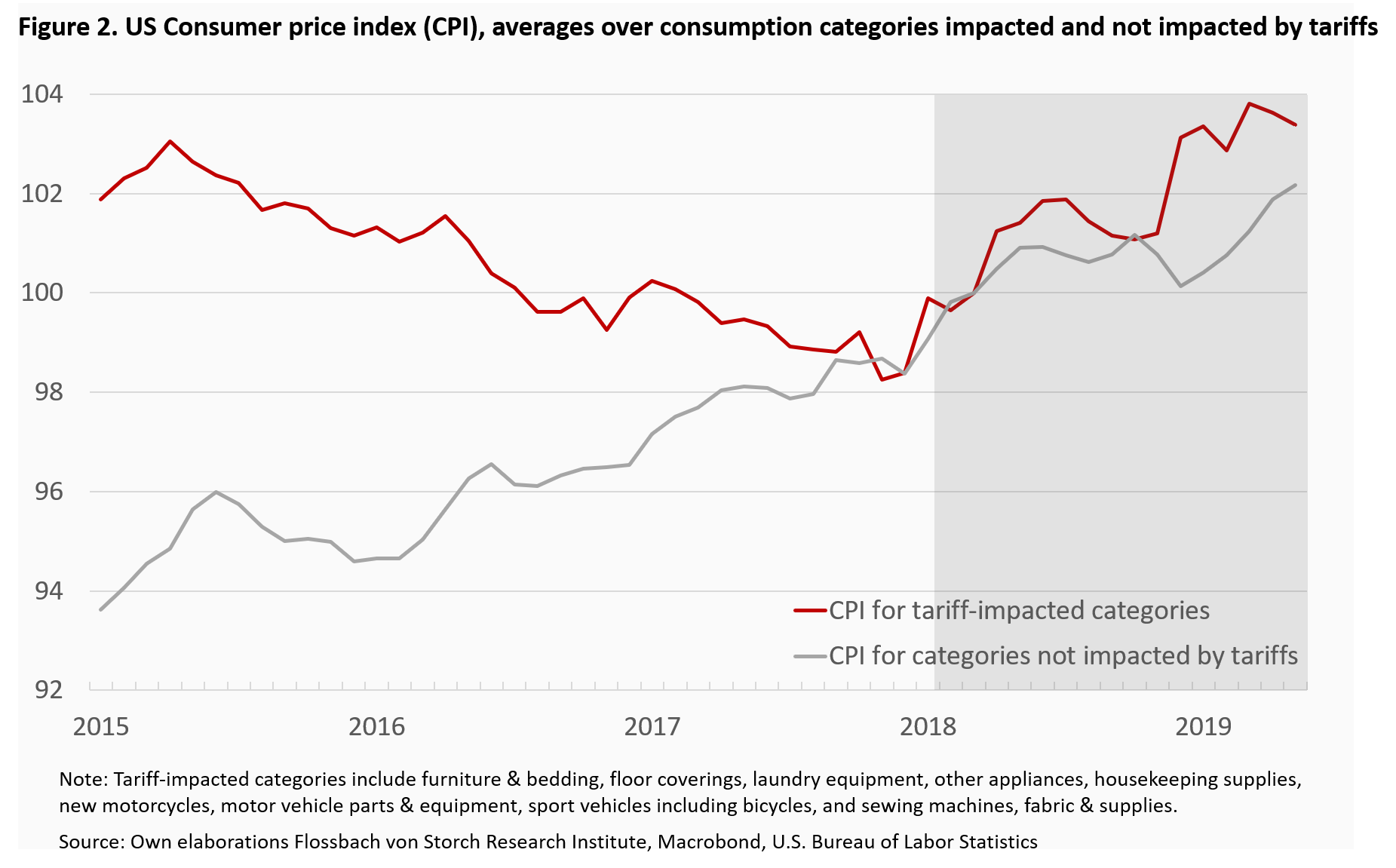

There is also some evidence suggesting that domestic prices on products affected by trade tariffs increased faster than on all other product categories (Fig. 2). However, the effect is not sizeable, reflecting the negligible cumulative weight of 2.4% that the tariff-impacted products have in the consumption basket underlying the consumer price index (CPI) in the US.2

Collateral effects of the US-China trade war

Besides the direct effects, the trade war impacts economic growth through indirect channels. Their precise measurement is difficult, as it often takes time for them to unfold. But the available evidence is already serious.

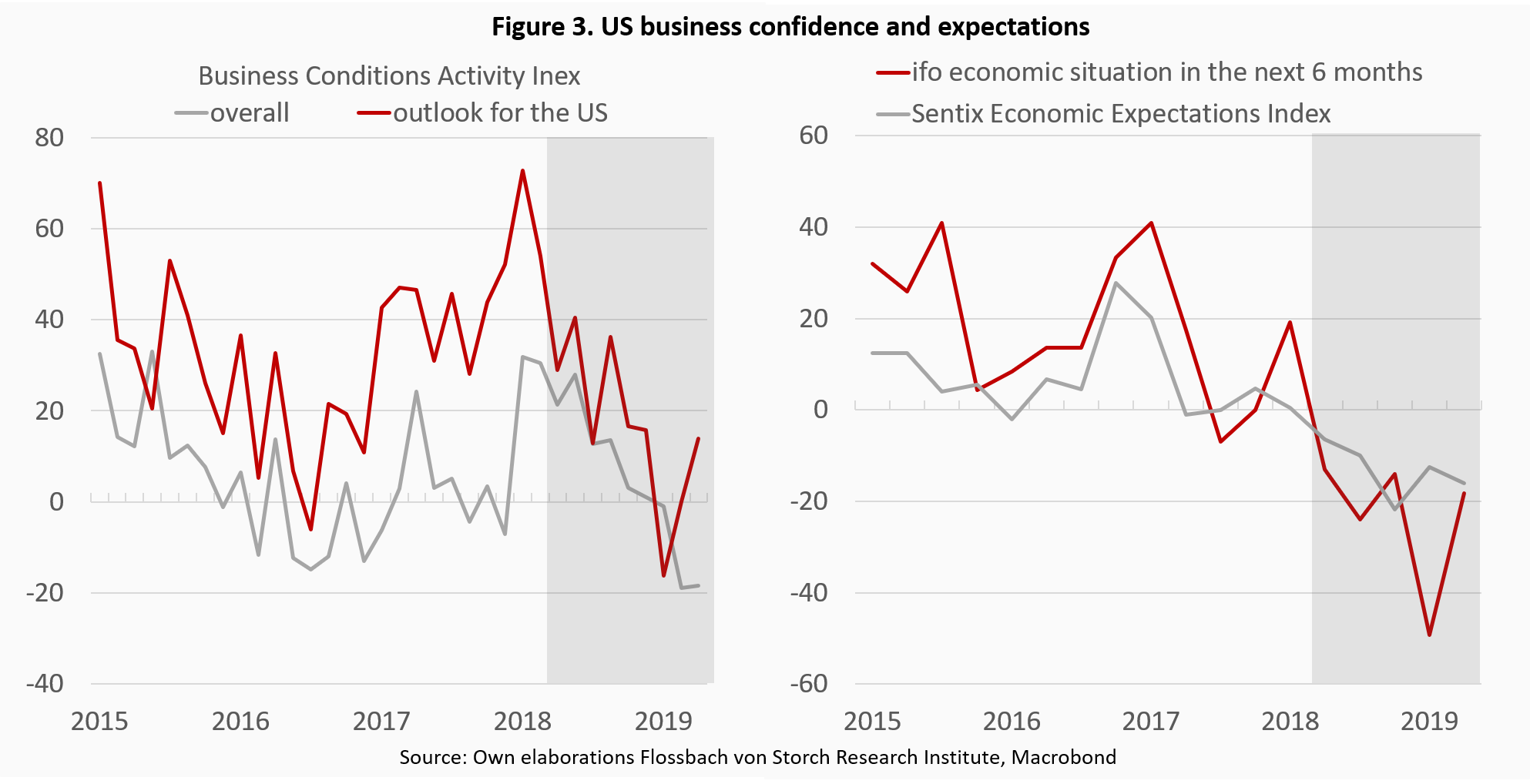

The indicators measuring the confidence of US businesses are sending worsening signals across the board. The Business Conditions Activity Index of the Federal Reserve Bank of Chicago, the Sentix Economic Expectations Index and the ifo index measuring the economic situation of the US economy in the next 6 months have weakened since March 2018 (Fig. 3). Moreover, given strong international trade dependences, negative spillovers have also reached businesses abroad in US and China trading partner countries.

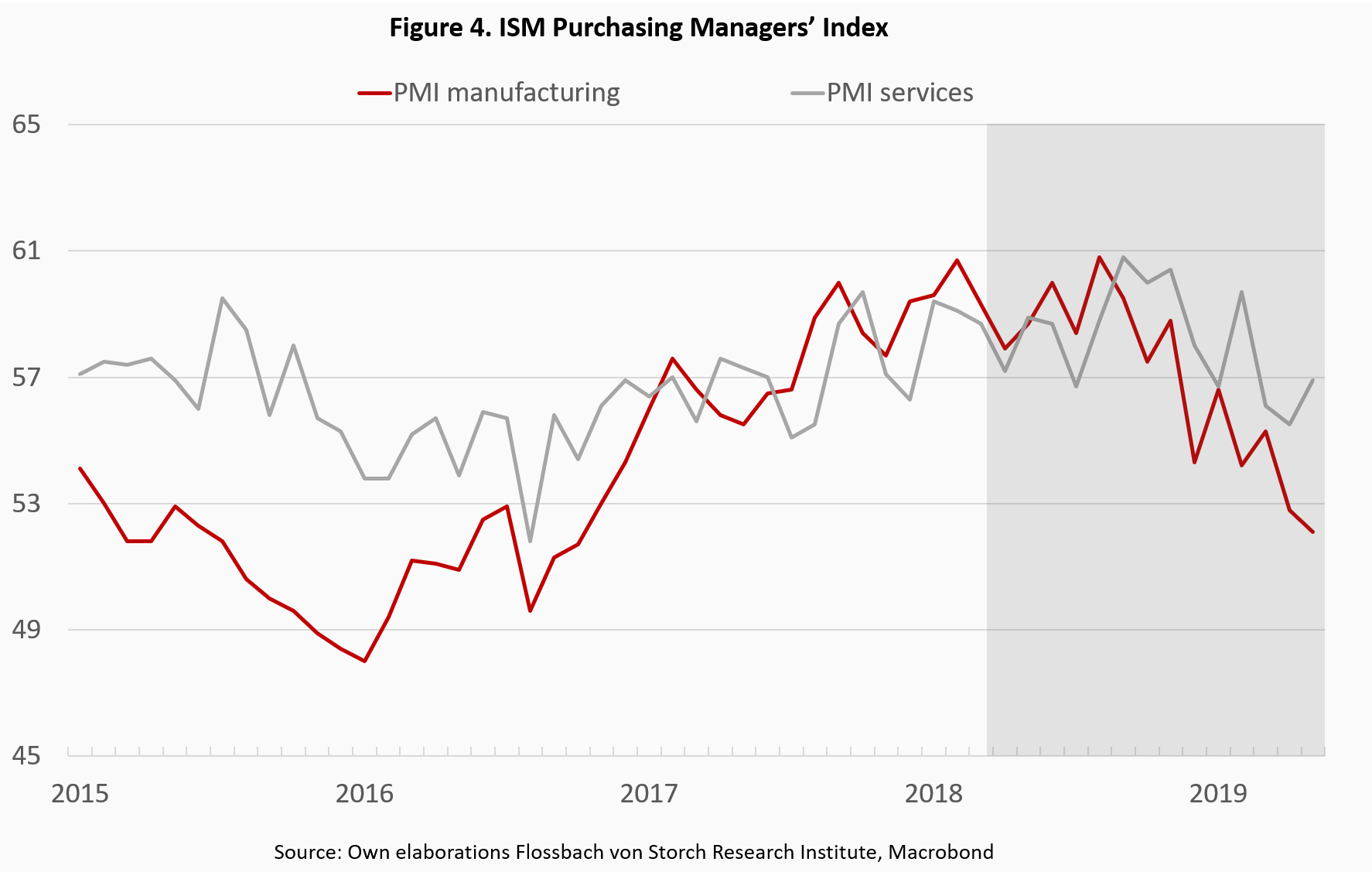

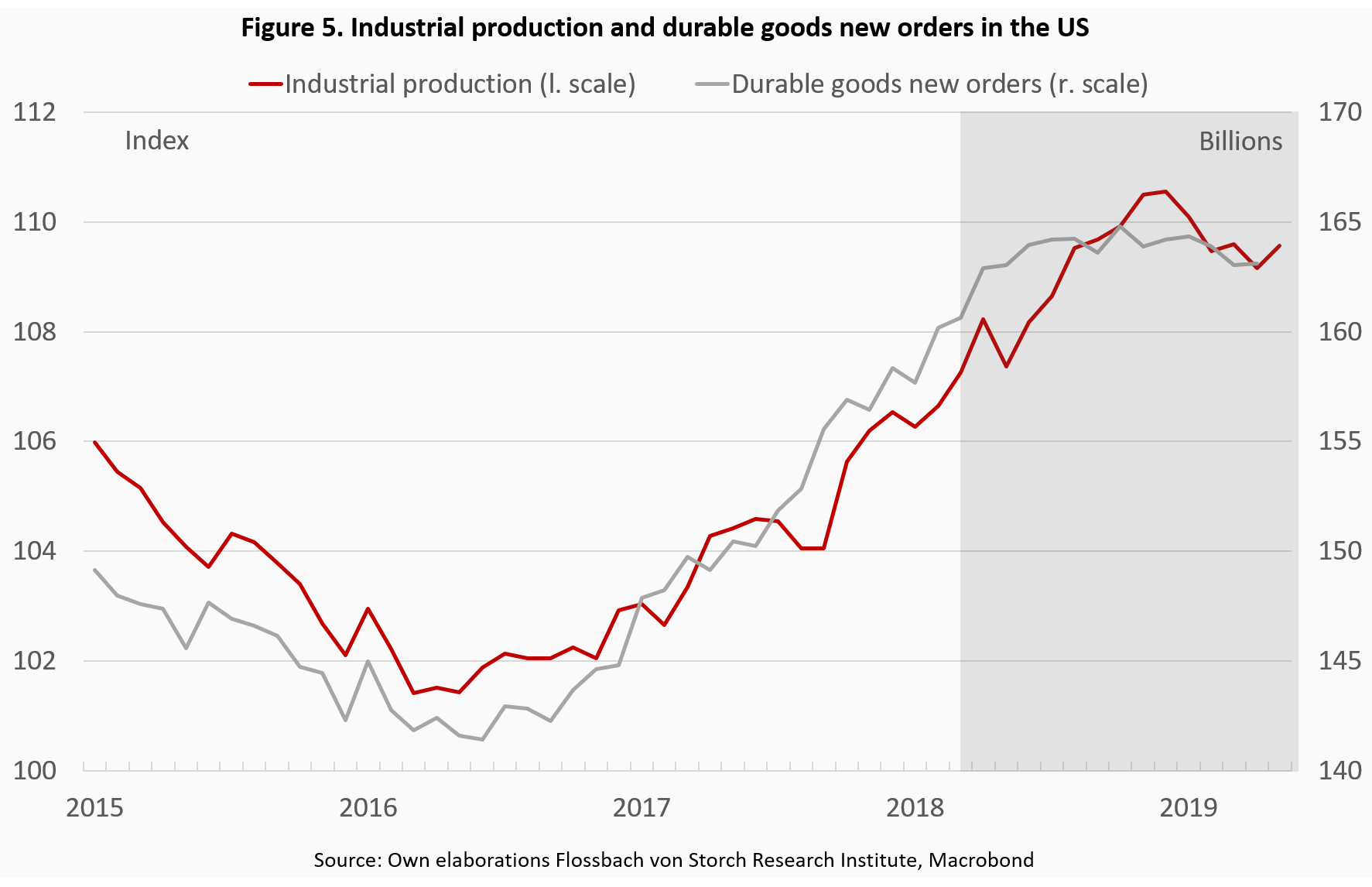

Caution towards the future, which has been emerging for several quarters now, is already reflected in management decisions on a broad front. The Purchasing Managers Index for the manufacturing and service sector has been on a downward trend since mid-2018 (Fig. 4). US industrial production and new orders in capital goods have also fallen since the end of 2018 (Fig. 5).

Caution required

There is growing evidence that trade tensions are now having negative effects on the US economy. In view of the approaching presidential campaign in the US, it should be in president Trump’s interest to reach a “beautiful deal” on trade at the upcoming G20 summit.

However, uncertainties remain. First, other factors, such as new Iran sanctions and more general geopolitical tensions, are likely to add fuel to the fire and counter any relief on trade front. Second, a trade deal would have to signal lasting peace so as to achieve a reversal in economic expectations. Finally, it is unsure to which extent the Chinese government would eventually be willing to cooperate on a deal that would primarily serve to support Trump’s poll results. After all, trade wars may not be so easy to win as President Trump believes.

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.

Agnieszka Gehringer

Senior Research Analyst

Agnieszka Gehringer joined the institute in 2015. She studied economics at the University of Rome “La Sapienza” and later earned a PhD in economics of complexity at the University of Turin. Since November 2019 she has been a professor of Economics at the Cologne University of Applied Sciences and since July 2016 a lecturer at the University of Göttingen. She has published several articles in academic journals and is an advisor to the EU.

All articles by Agnieszka Gehringer