05.12.2022 - Studies

Inflation has been rising faster than is tolerable for central banks for at least a year and a half. The central banks of the largest industrialized countries were forced to tighten their monetary policy to counter inflationary pressure, initially considered to be temporary. In recent weeks, a drop in the inflation rate in the U.S. triggered euphoria in financial markets as hopes were raised the Fed would decelerate its pace of monetary tightening. But, is inflation really falling or are we merely observing a base effect because inflation rose so quickly last year?

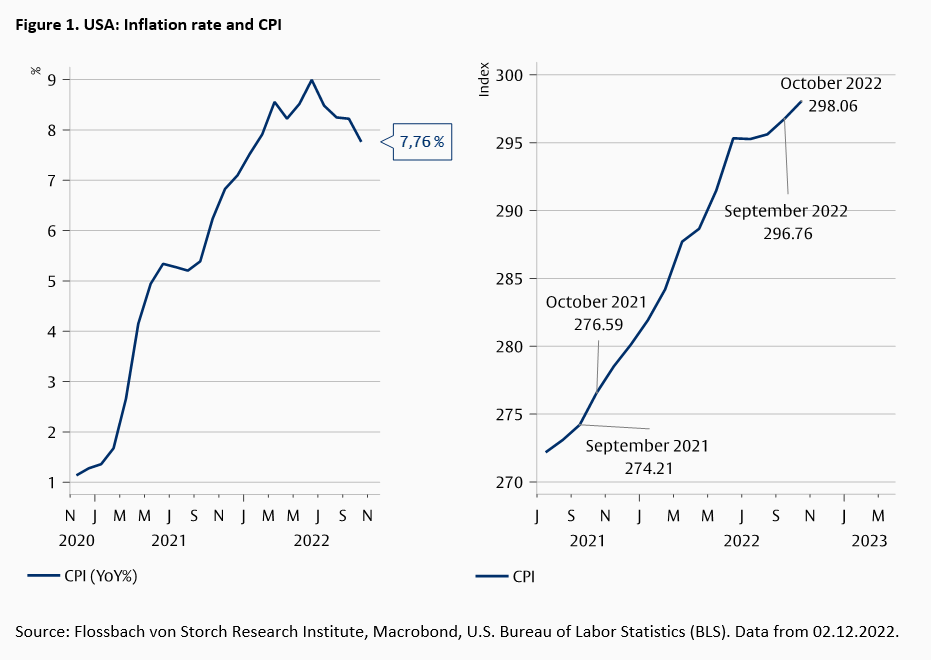

Inflation is defined as the change in a consumer price index compared to the same month in the previous year (YoY%). In the U.S., for example, inflation in October 2022 was 7.8%, the percentage change in the Consumer Price Index (CPI) from October 2021 (276.59) to October 2022 (298.06) (Fig. 1).

Changes in the inflation rate therefore reflect not only the current inflation dynamics, but also the inflation dynamics twelve months in the past. The inflation rate in the U.S. fell from 8.2% in September to 7.8% in October, a change of -0.4 percentage points. This change is the result of the difference between two monthly rates of change: +0.44% between September and October 2022 and +0.84% between September and October 2021 (0.44% - 0.84% = -0.4%). Because CPI increased less between September and October 2022 than between the same months of the previous year, the inflation rate decreased.1 The base effect thus accounted for a decline in the inflation rate.

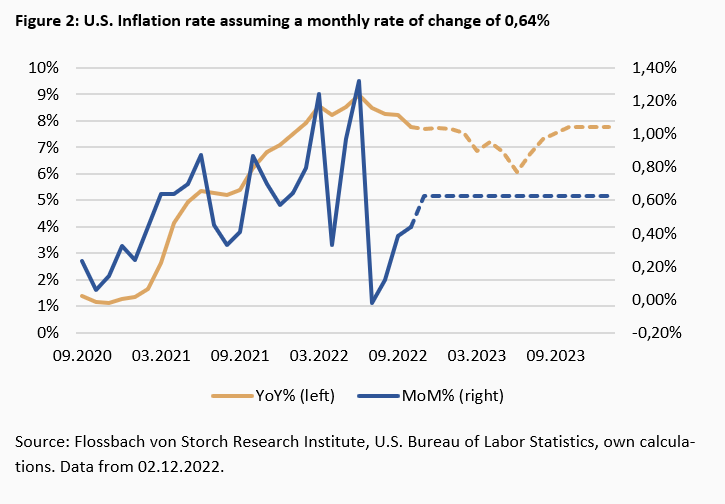

Since, by definition, the movements of the inflation rate today depend on the dynamics of the previous year, it is possible to see a falling inflation rate even if inflationary pressures remain constant from one month to the next. Consider an example as an illustration: the October 2022 inflation rate in the U.S. was 7.8%. The monthly change in the CPI was therefore 0.62% on average. Assuming the CPI maintains its momentum and changes by 0.62% each month starting in November 2022, the inflation rate (YoY%) would initially continue to decline (Fig. 2). This decline would be the base effect. Starting in July 2023, the inflation rate would rise again because the monthly changes this time would be higher than the changes in the same months of the previous year. The inflation rate would reach the annual level of 7.8% from October 2023.

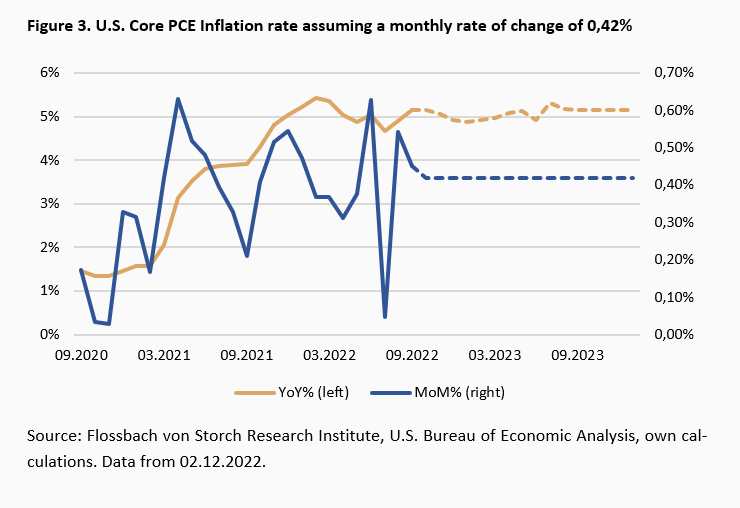

The base effect of the Fed's preferred core PCE inflation rate is smaller. If the index were to change monthly as it did on average over the past 12 months (0.42%), the core inflation rate would slightly fall due to the base effect and then rise again to the actual inflation rate of 5.2% (Fig. 3).

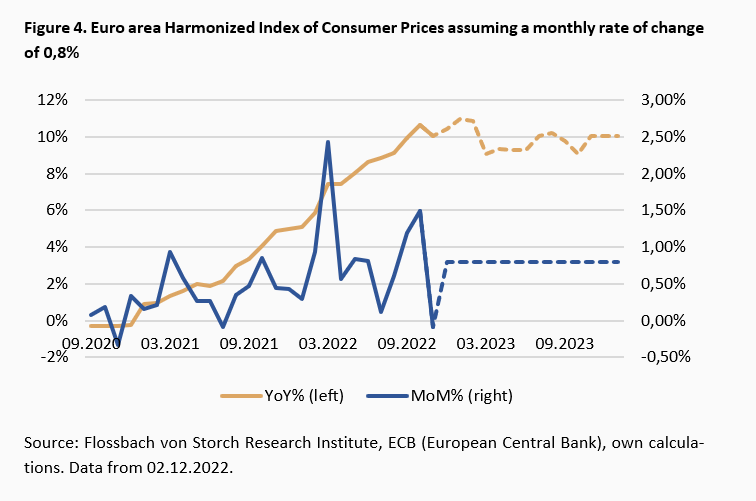

A base effect peak in inflation is likely still ahead in the euro area. Assuming monthly rates of change in the HICP would remain as high as 0.8% on average since November 2021, inflation in the euro area would initially continue to rise up to 11% through January 2023 and then fall slightly, thanks to the base effect. The peak in the inflation rate may therefore be an artifact.

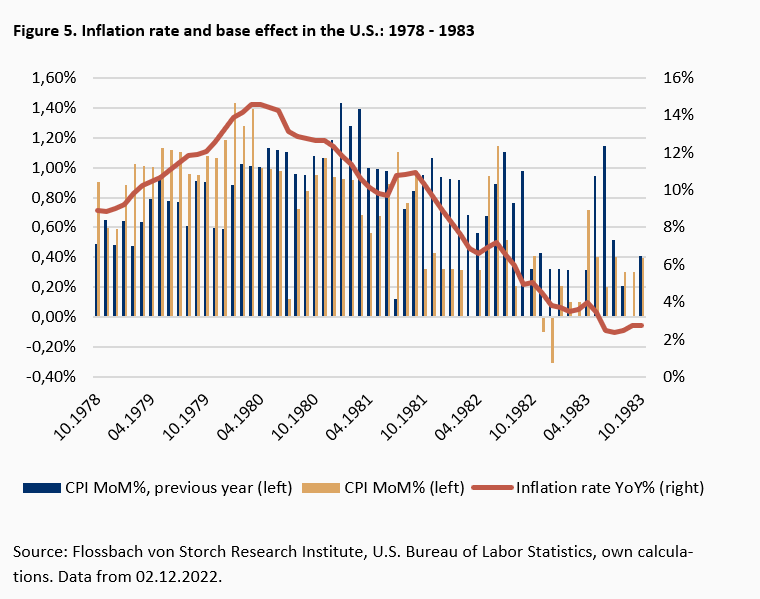

As mentioned above, the change in the annual inflation rate can be defined as the difference between the monthly change in the price index in the current year and the monthly change in the same month of the previous year. For the decrease in the inflation rate not to be an artifact, the monthly rates of change must be declining in trend. This was the case in the U.S. between 1978 and 1983 (Fig. 5). If the monthly change (yellow bars in Fig. 5) was larger than in the same month of the previous year (blue bars), there was a negative base effect. As a general pattern, if the blue bars were larger than the yellow bars, the annual rate of inflation decreased. The annual rates of change in the CPI increased until the trend reversed from March 1980. In part, this was the result of the base effect, because the monthly changes were larger in 1979 than in 1980. Crucially, however, monthly inflation rates tended to decline as inflationary pressures decreased.

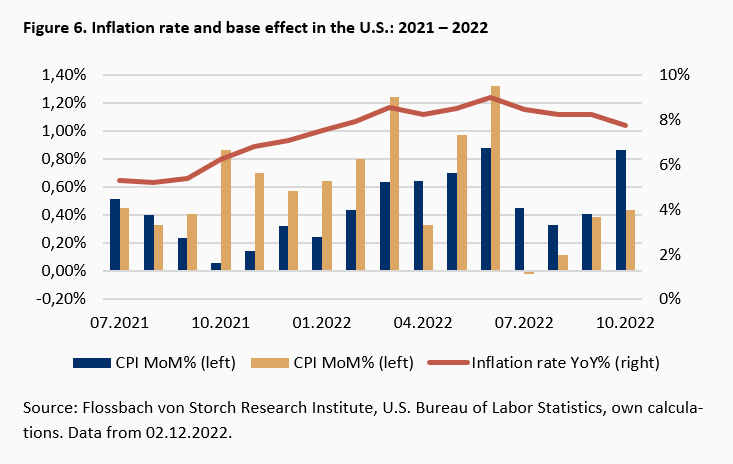

Today, the question is whether the recent peak in the annual inflation rate was mainly caused by the base effect. From July 2022 monthly changes in the CPI have been much lower than in the previous year, albeit with an upward trend (Fig. 6).

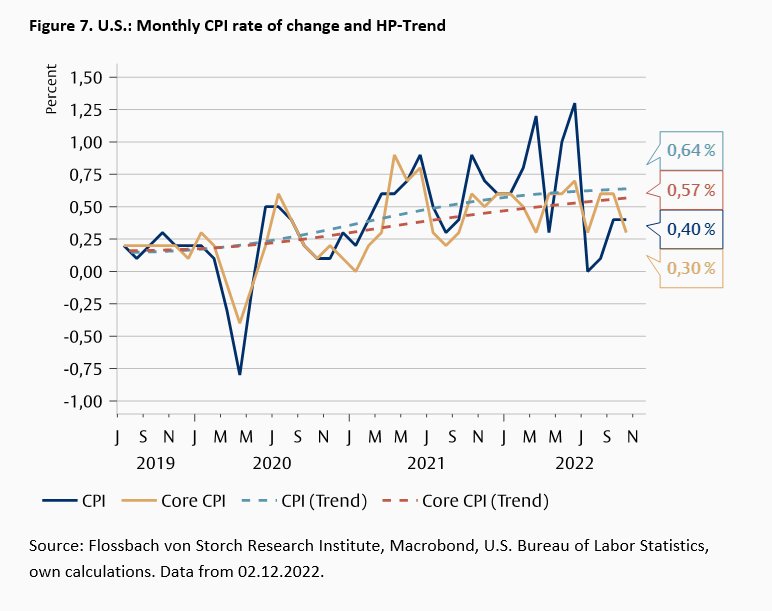

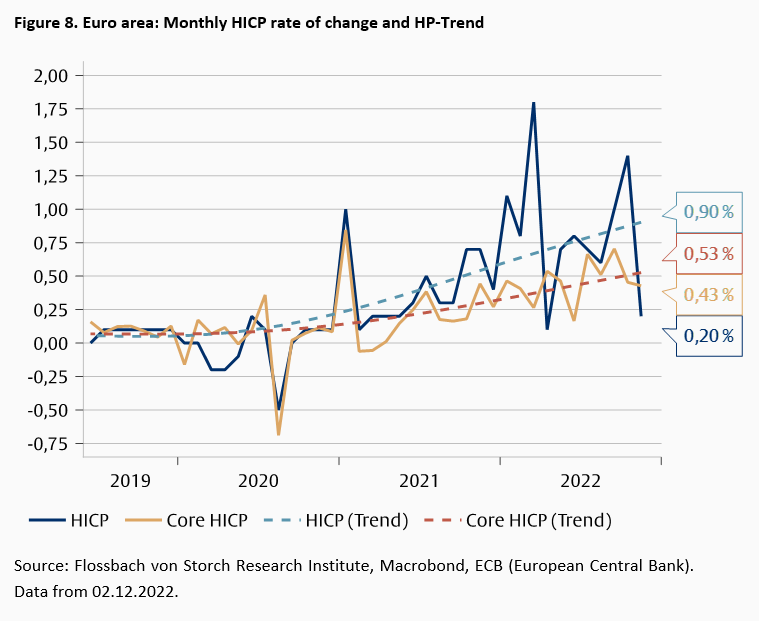

Furthermore, the monthly rates of change of both the overall CPI and the core CPI (excluding energy and food) in the U.S. do not show a decreasing trend yet (fig. 7). The same applies to the euro area, where the trend in the monthly rates of change of the core index is only slightly below the trend in the U.S., but the trend of the overall index is much higher (fig. 8).

The inflation rate is usually defined as the change in a consumer price index compared with the same month of the previous year. Changes in the inflation rate therefore incorporate, by definition, both the inflation dynamics of the previous month and the dynamics of the same month in the previous year. If in one month the consumer price index increases less than it increased in the same month of the previous year, the inflation rate decreases. This allows the annual inflation rate to decrease, even if the inflation in the current month is the average of the last 12 months. Therefore, it is possible for the inflation rate to reach a peak without the inflation dynamics having weakened. If this is the case, the inflation rate rises again after a few months.

The recent decline in the inflation rate in the US shows a significant drop in the monthly rates of change of CPI in July. Since then, however, the monthly changes have been rising again. Therefore, the base effect has played an important role so far. The decisive factor for the future will be whether the Fed's monetary policy measures have really decelerated the inflation dynamic – the trend of monthly changes. This cannot yet be seen in the trend of monthly rates of change. In the eurozone, the trend of monthly inflation rates is still rising, and a peak in inflation has probably not yet been reached. When it does, it will be necessary to examine the extent to which the decrease in the inflation rate is driven by the base effect or is due to a fundamental change in inflation dynamics.

1 Since percentage changes can be approximated by the difference of the natural logarithms, the change in the inflation rate πt can be expressed as: πt - πt-1 = ln(CPIt) - ln(CPIt-1) -[ln(CPIt-12) - ln(CPIt-13)]

09.03.2021 - Macroeconomics

by Pablo Duarte

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch SE. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch SE remains solely with Flossbach von Storch SE. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch SE.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch SE.

© 2024 Flossbach von Storch. All rights reserved.

Pablo Duarte

Senior Research Analyst

Pablo Duarte joined the institute in 2020. He earned a PhD in economics from Leipzig University and was a visiting researcher at New York University. He studied economics at Leipzig University and Universidad del Rosario (Colombia). Pablo Duarte’s research interests include international macroeconomics and economic policy.

All articles by Pablo Duarte