27.02.2024 - Studies

Due to a series of geopolitical events, the main global economic blocks are now affected by the process of geoeconomic fragmentation that reshapes global trade and investment flows.

International economic fragmentation was once seen as a natural by-product of intensifying global trade flows and international re-organization of production. The process implied that “segments (production blocks) are located in different geographical areas, perhaps in different countries, and that they may be undertaken by different firms.”1 The fathers of the concept also noted that “[a]n important advantage of fragmentation is that it allows production blocks to be moved around so that components are produced in the best possible location.”2

The current meaning of fragmentation has changed radically. Today experts in the field speak about geoeconomic fragmentation to refer to “a policy-driven reversal of global economic integration often guided by strategic considerations”.3

This paper documents the recent developments in geoeconomic fragmentation in the three major economic blocks – the EU, the US, and China – across the two main economic dimensions – trade and foreign direct investment flows.

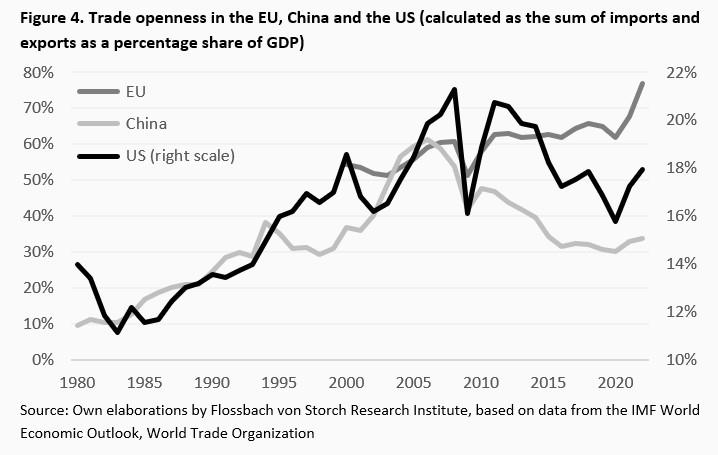

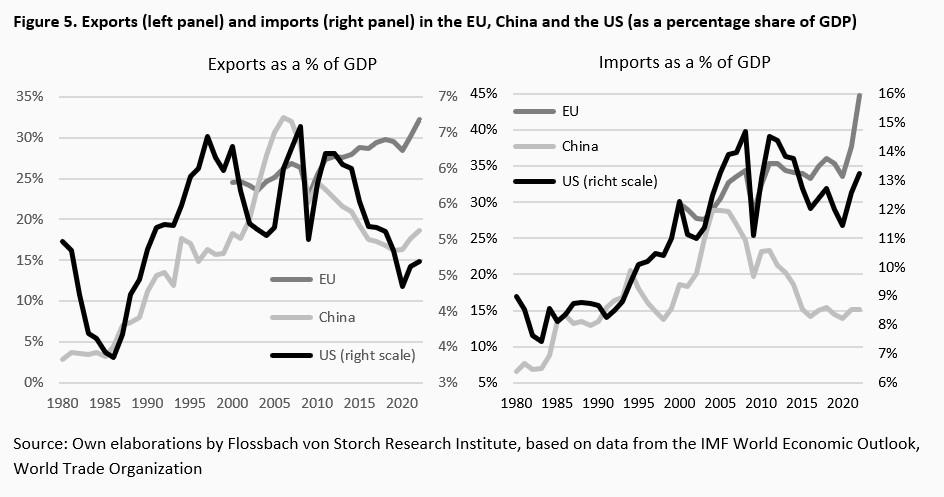

The first discernible fractures in the global economy began to surface in the aftermath of the 2007/2008 great financial crisis. Both cross-border trade and investment flows were strongly affected by the underlying financial and economic turmoil (Fig. 1).

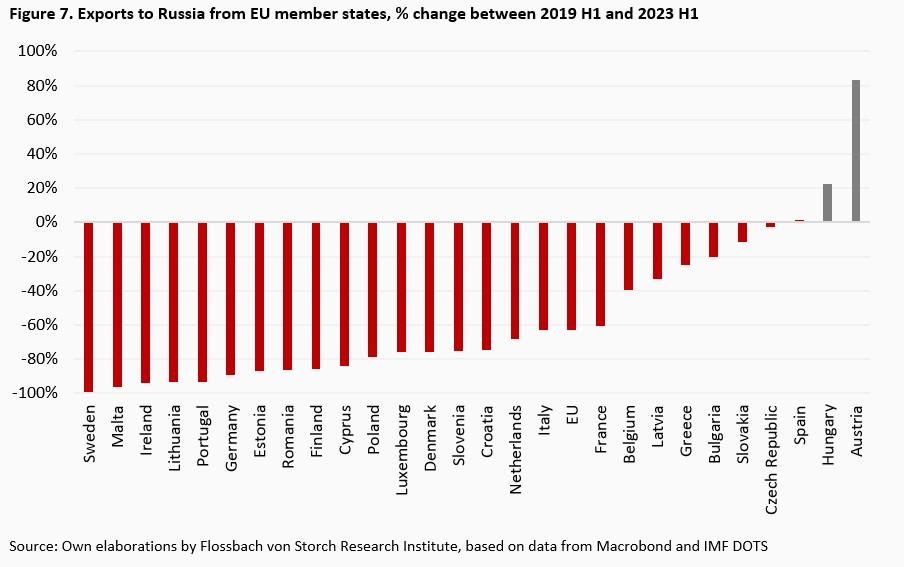

But these trend reversals have been significantly reinforced by a series of more recent events, predominantly rooted in geopolitics. A pivotal role in sparking economic cracks to the global economic order played the Brexit vote, the US-China trade dispute, the COVID-19 pandemic, and Russia’s invasion of Ukraine.

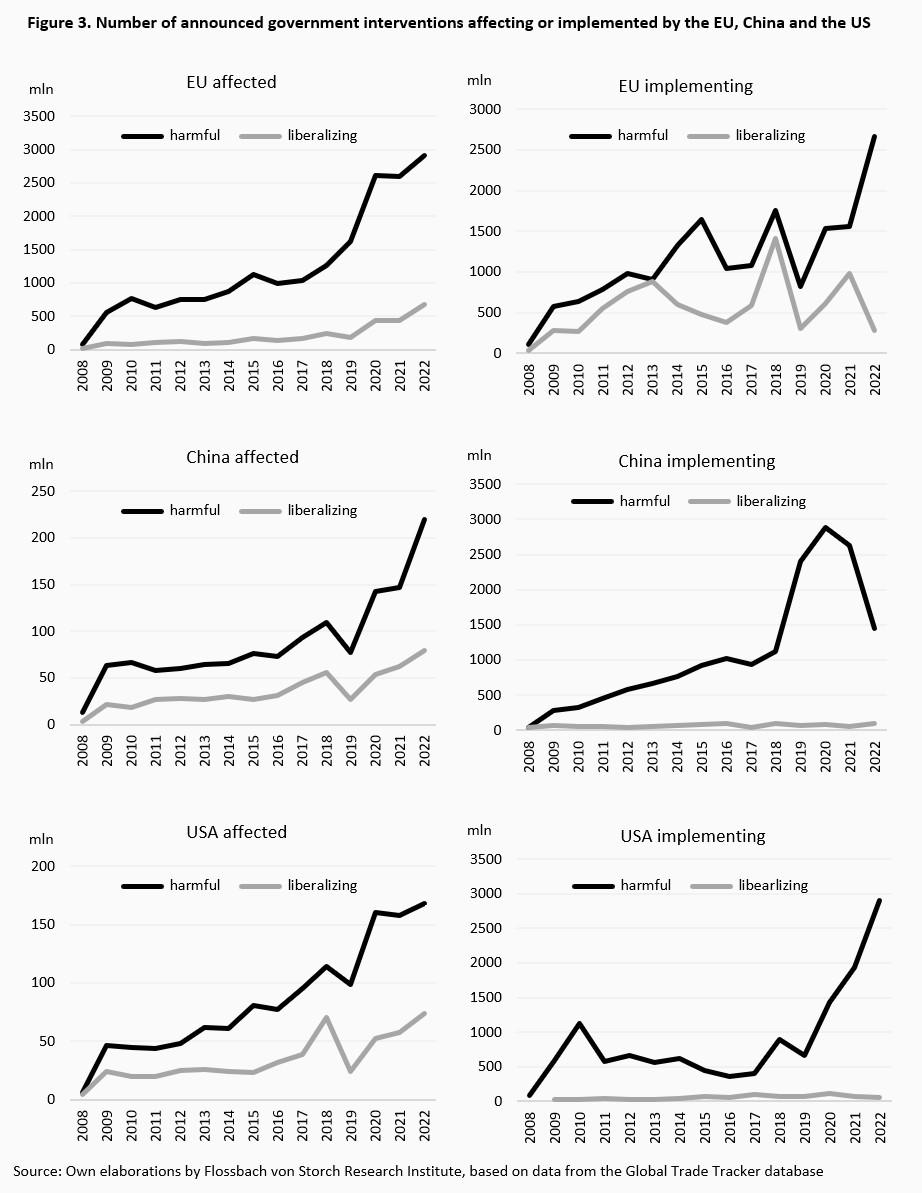

The involvement in policy interventionism of the three main economic blocks, the EU, China and the US, has been strong and intensifying. However, whereas the EU is more intensively affected by harmful interventions of others than it imposes against others, the opposite is true for China and the US. For both countries, the number of harmful measures implemented exceeds the number of measures affecting them by a large margin. In the United States, there has been a notable surge in protectionist interventions, particularly evident since Donald Trump assumed the presidency in 2017, but the trend continued under the Biden Administration (Fig. 3).

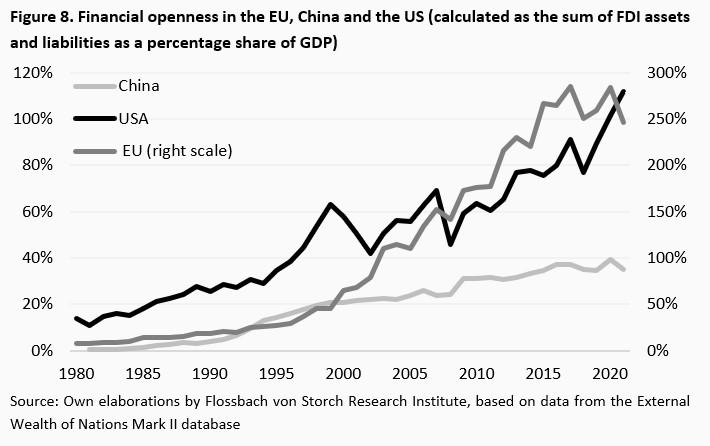

The setback in cross-border long-term financial investment activity in the three economic blocks is less pronounced than for trade relations, although the evidence for the EU is telling (Fig. 8). Since 2017, the degree of financial openness – measured as the sum of FDI assets and liabilities as a percentage share of GDP – has moved sidewards, likely driven by policy efforts aimed at limiting investment that could jeopardize security or public order. But also in China, there has been a slowdown in financial openness, the timing of which broadly corresponds with the EU’s experience. More precisely, the FDI stock of liabilities as a percentage of GDP reached its peak of 26% in 2009, moved sideward until 2016, and declined subsequently to 20% at the end of 2021 (Fig. 9).

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.

Agnieszka Gehringer

Senior Research Analyst

Agnieszka Gehringer joined the institute in 2015. She studied economics at the University of Rome “La Sapienza” and later earned a PhD in economics of complexity at the University of Turin. Since November 2019 she has been a professor of Economics at the Cologne University of Applied Sciences and since July 2016 a lecturer at the University of Göttingen. She has published several articles in academic journals and is an advisor to the EU.

All articles by Agnieszka Gehringer