09.11.2022 - Studies

![[Translate to English:]](https://www.flossbachvonstorch-researchinstitute.com//fileadmin/_processed_/9/1/csm_china-eu-klein_542a40f3aa.jpg)

Trade relations of the EU are skewed towards a few countries. At least since Russia’s invasion of Ukraine the tight links with China must be regarded as a major source of political and economic risks. Contrary to expectations, closer trade relations with authoritarian regimes not only fail to induce shifts towards more democracy but can also be used by these regimes as a tool to blackmail its trading partners.

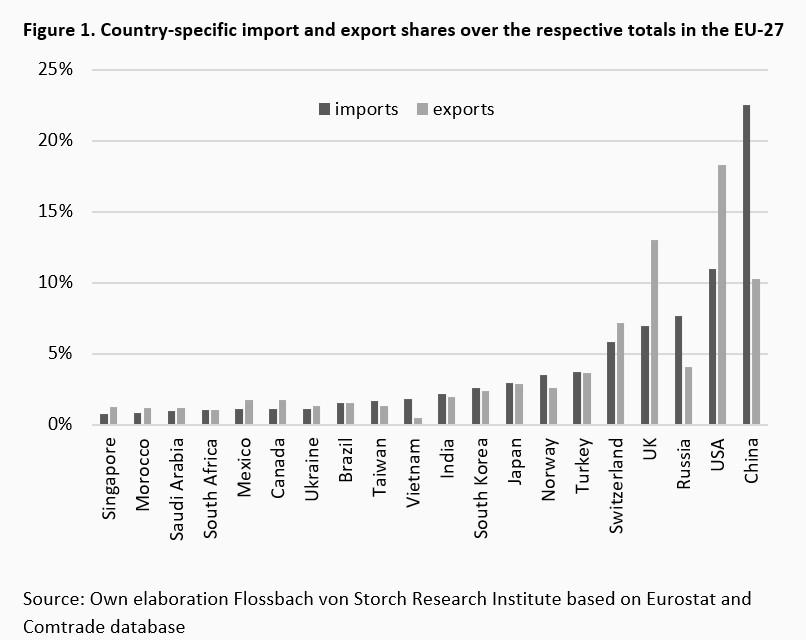

Specifically, currently almost 23% of the total imports of the EU come from China, followed by 11% from the US and around 8% from Russia. On the export side, the highest share of 18% is held by the US, followed by a 13% share of the UK, and 10% share of China (Figure 1).

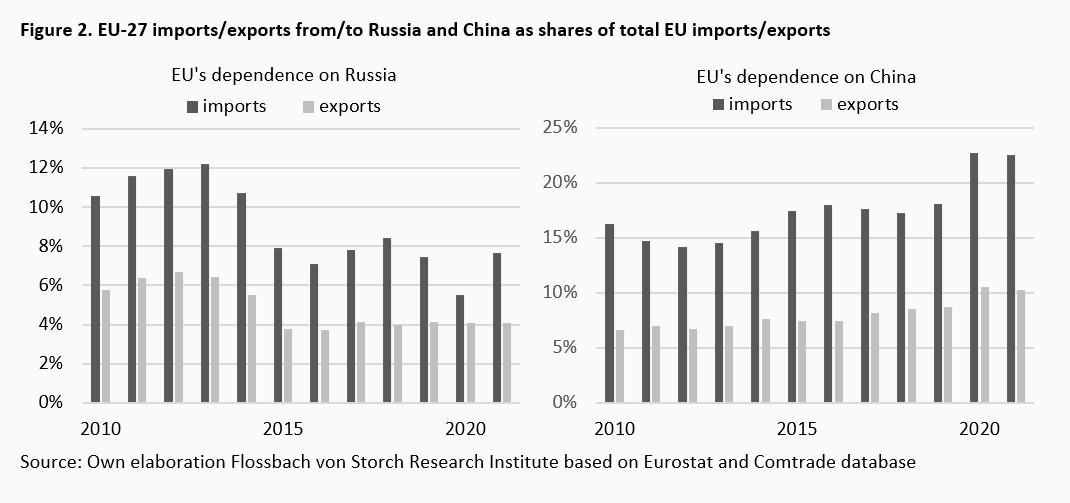

Whereas the EU’s trade dependence on Russia has diminished somewhat in the wake of Russia’s annexation of Crimea in early 2014, trade links with China have continued to intensify, both on the export and import side (Figure 2).

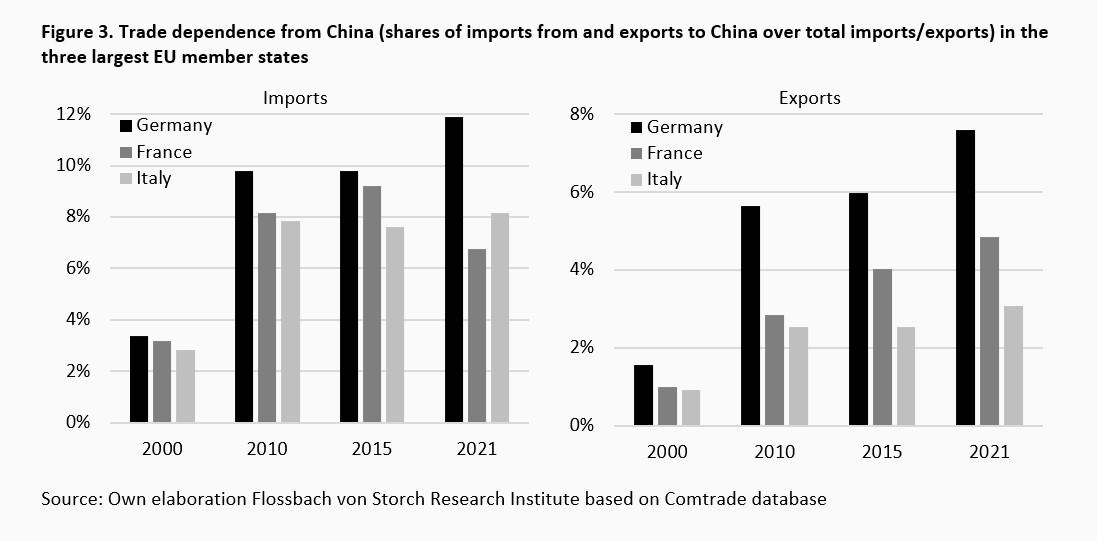

Among the three largest EU members, Germany has the strongest trade links with China, both in terms of imports and exports. The relationship increased significantly over the last two decades, rising from 3.4% to 11.9% for imports and from 1.6% to 7.6% for exports. Both France and Italy increased their trade relations as well compared with the beginning of the new millennium. France’s export dependency on China increased from 1% in 2000 to almost 5% in 2021. At the same time, France has managed to reduce its import dependency from 9.2% in 2015 to 6.7% in 2021, whereas Italy’s respective trade shares moved sidewards over the last decade (Figure 3).

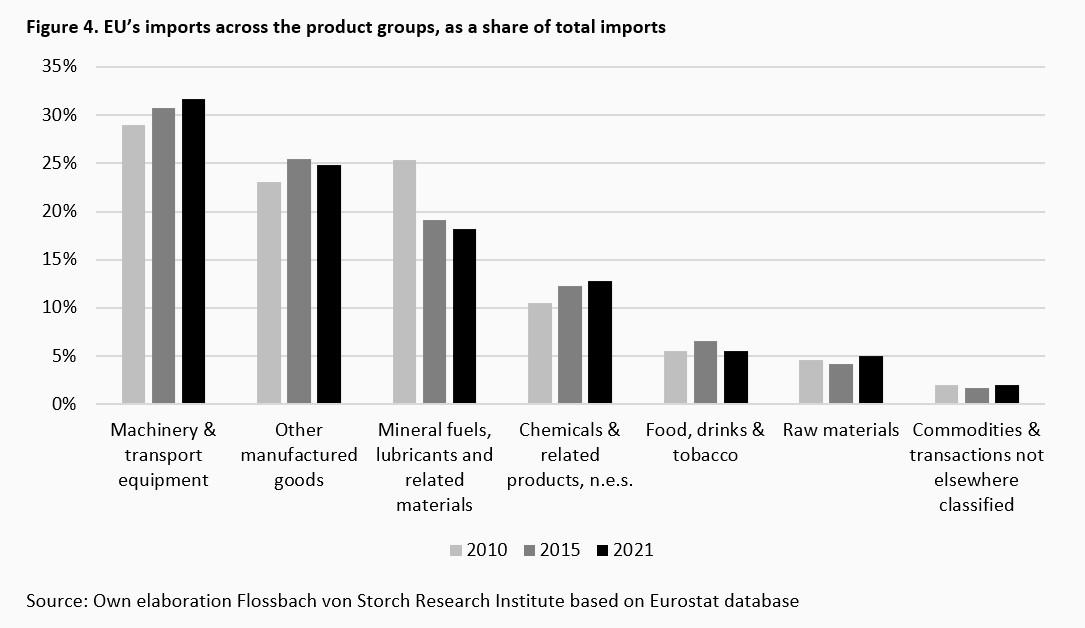

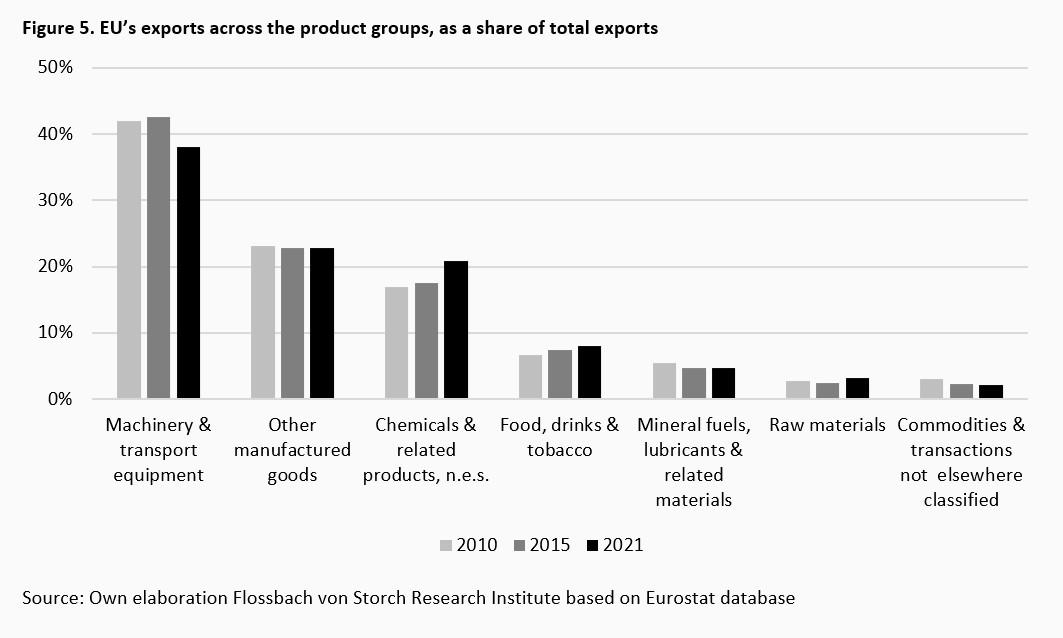

Across the broad product groups, the strongest EU’s foreign trade relations exist for machinery and transport equipment. In 2021, the import share in this product group over EU-wide imports increased from 29% in 2010 to 32% in 2021 (Figure 4). The corresponding export share declined from 42% in 2010 to 38% in 2021 (Figure 5).

For the EU’s imports in almost all product categories reported in Figure 4, China plays a dominant role, reflecting the country’s rise as manufacturing superpower since the 1970s.

Whereas not every trade relation – especially on the import side – is toxic per se, it becomes so if it leads to “strategic dependence”. This is the case if simultaneously three conditions are satisfied:

1) The country/region is a net importer of a good.

2) The country/region imports over 50% of its total imports of the good from a single partner.

3) The partner possesses at least 30% of the global market share for the good in question.1

Under strategic dependence, it is difficult for the country to readily re-direct its imports away from the exporter, which is a dominant player in the global market.

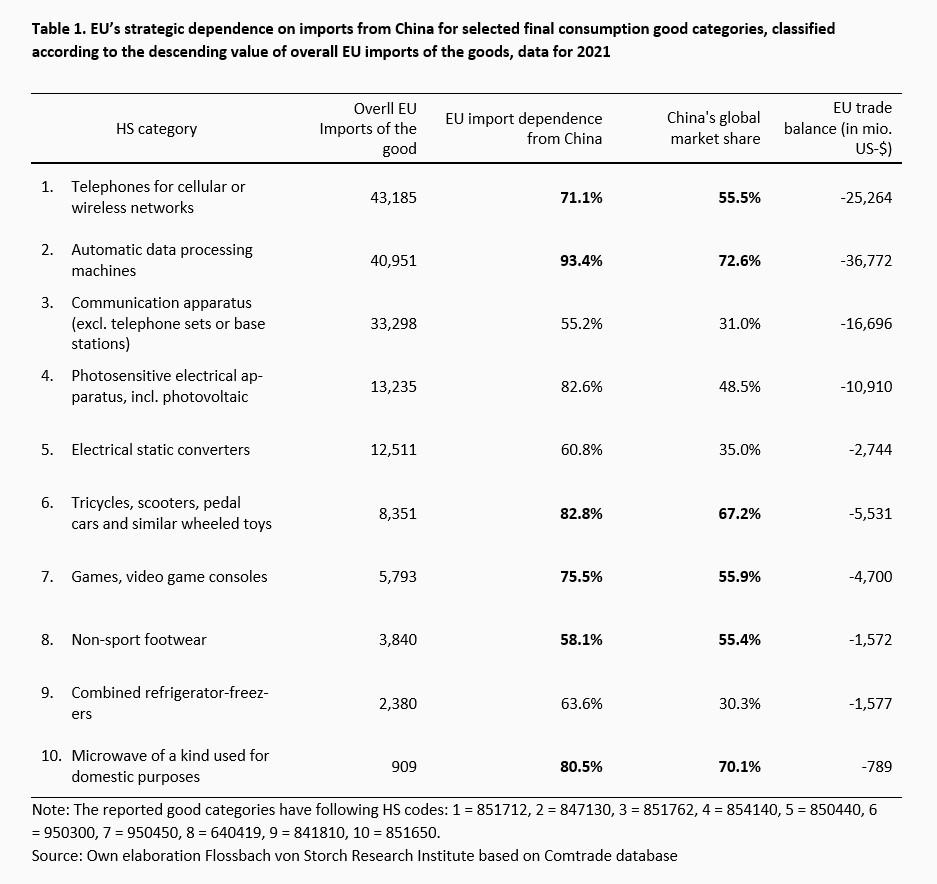

Following this definition, Tables 1 and 2 show strategic import dependences of the EU on China for main categories of final consumption and intermediate goods as of 2021. Both classifications are based on import values for 6-digit Harmonized System (HS) product categories.2 This allows a detailed view at the goods that are traded.

Among the top ten consumer goods, the strongest import dependence exists for important electronic devices. Specifically, in 2021, over 70% of EU overall imports of mobile phones originated from China, with China having almost 56% of global market share in this product category. Analogously for automatic data processing machines, wheeled toys, video games, and non-sport footwear the EU imports 93%, 83%, 76% and 58%, respectively, from China, with the latter possessing over 50% of the respective global market shares (Table 1).

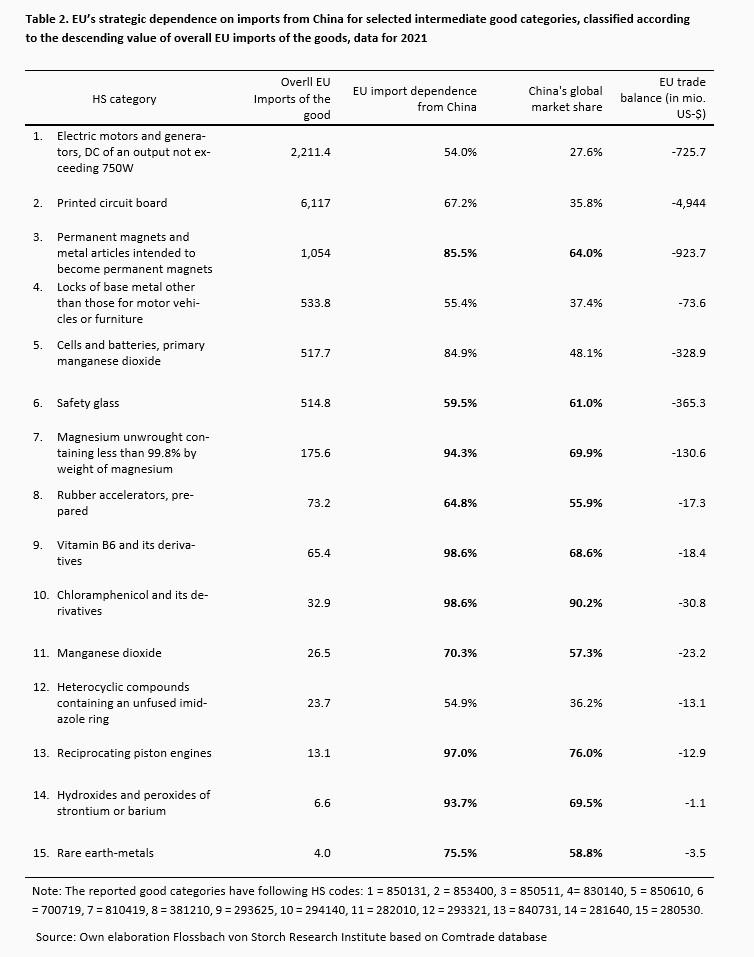

But even more critical should be strategic dependences for intermediate goods. The unavailability of an essential production factor has the potential to disrupt the industrial production directly and indirectly along the supply and value chain. This is especially so if alternative suppliers cannot be easily and timely found.

The EU is particularly dependent in several categories of electrical machinery and equipment and parts thereof, in machinery and mechanical appliances, in base metals, glass, as well as in different categories of organic chemicals and inorganic chemicals (Table 2). Although they are not sophisticated technological goods, many of these products are critical inputs in the upstream production and make the entire industrial processes vulnerable to shocks. For instance, the EU's green energy industry – especially the wind energy sector – is highly dependent on China’s supply of magnetic metals that are essential component for wind turbines as well as modern electric motors. Also, minerals for power electric car batteries are typically mined and refined by Chinese companies.

Given the intensifying geopolitical tensions, the growing economic dependence of the EU – especially on China – leads to the loss of strategic sovereignty. China has already shown in the past that it is willing to use its potential for economic blackmail in the supply of crucial resources. Back in 2009, China boycotted its exports of rare earths that are crucial for computer manufacturing. Under the leadership of Xi Jinping the pressure is likely to intensify.

Reducing underlying dependences should thus be a priority for the EU’s industrial policy. It is primarily a matter of adapting the trade framework and the economic incentives to encourage purposeful structural changes. One meaningful instrument includes the abolition or at least substantial reduction of investment guarantees for business activities in and with China.

Another effective strategy could be the development of new export and import markets through intergovernmental agreements abolishing existing trade barriers and creating attractive investment conditions. The short-term effects of a move away from China could come with losses in efficiency and profits. But diversification should pay off in the mid- to long-term when new capacities are sufficiently developed to take yield form economies of scale and scope.

Diversification would have been emphasised a long time ago if the EU had taken its own very high standards with regards to environmental and social sustainability more seriously. Instead, a myopic strategy put at risk not only sustainability itself but ultimately also the EU’s geopolitical integrity. Since the latter is an essential prerequisite for the former, it would be high time for the EU to rethink its priorities.

1 The definition and measurement of strategic dependence adopted in this study follows the approach of Zenglein, M.J. (2020), Mapping and recalibrating Europe’s economic interdependence with China, Merics, China Monitor, November 18, 2020.

2 The HS is organized into 21 sections, subdivided into 99 chapters (2-digit), 1,244 headings (4-digit) and 5224 subheadings (6-digit).

14.10.2022 - Economics, Politics & Philosophy

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.

Agnieszka Gehringer

Senior Research Analyst

Agnieszka Gehringer joined the institute in 2015. She studied economics at the University of Rome “La Sapienza” and later earned a PhD in economics of complexity at the University of Turin. Since November 2019 she has been a professor of Economics at the Cologne University of Applied Sciences and since July 2016 a lecturer at the University of Göttingen. She has published several articles in academic journals and is an advisor to the EU.

All articles by Agnieszka Gehringer