31.01.2023 - Studies

"The values that guide our decision-making are set out in our Credo. Simply put, our Credo challenges us to put the needs and well-being of the people we serve first." This value proposition was coined by Robert Wood Johnson, co-founder of a well-known pharmaceutical and consumer goods company. He believed "that our first responsibility is to the patients, doctors and nurses, mothers and fathers, and everyone else who uses our products and services. To meet their needs, everything we do must be of high quality. We must constantly strive to create value, reduce our costs and maintain reasonable prices".

In addition, his company has a "responsibility towards our employees who work for us worldwide. We must create an inclusive work environment where each person must be seen as an individual. We must respect their diversity and dignity and recognise their merits". And "we must keep the property we are allowed to use in good condition, protecting the environment and natural resources".

Many people may have come across such an agenda in a similar form in recent months or years. Quite a few companies now focus on their commitment to nature and society in addition to disdainful earnings figures or the listing of assets and sources of capital. Whether this is of their own accord or due to political pressure remains to be seen.

But the credo that Robert Wood Johnson formulated for his company Johnson & Johnson did not come from a new political agenda or the green-social wave of this century, but dates back to 1943; long before anyone had heard of "Corporate Social Responsibility" (CSR) or "Environmental, Social and Governance" (ESG).

Johnson & Johnson has not always been able to live up to its own high standards, however - at least when measured by the billions of dollars in fines the company has had to pay in recent years following lawsuits alleging significant side effects from some of its medicines.

On the one hand, this proves that aspirations and reality are not so easy to reconcile. And it also shows that shareholders and other stakeholders should take a close look at the extent to which companies actually live up to their standards.

Johnson & Johnson is nevertheless fortunate today to have been a first mover in CSR. The company, which is listed in the elite Dow Jones Industrial Average, explicitly refers to the credo of its co-founder in its "ESG Disclosure Index" - in connection with current requirements that the Norwegian Sovereign Wealth Fund places on companies worldwide in its individual guidelines. The Norwegians are one of the largest equity investors in the world with their fund currently worth around 1.2 trillion euros - and can therefore set their own rules.

While sovereign wealth funds or other large investors have enough capital behind them to demand information from companies that goes beyond the usual annual report, the taxonomy of the European Union (EU) is now pushing deep into the ESG reporting of almost all companies. The EU wants to establish a mandatory assessment of "environmental sustainability" of economic activities valid for all companies slightly larger than a local business with perhaps a few dozen employees.

Thus, at the end of November 2022, the Council of the EU approved a decisive directive on sustainability reporting. This Corporate Sustainability Reporting Directive (CSRD) has been in force since 5 January 2023. Within 18 months, the EU member states must now transpose this directive into national law.

This decision has implications, globally.

Companies will thus be required to publish detailed ESG reporting soon. "The new rules will make more companies accountable for their impact on society and move towards an economic model that benefits people and the environment. Data on environmental and social footprint will be publicly available to all who care," said Czech Industry and Trade Minister Jozef Síkela - the Czech Republic held the EU Presidency until the end of 2022.1

For the year 2024, companies and financial institutions are to apply the new sustainability reporting for the first time. The CSRD replaces the previous directive on non-financial reporting by companies (Non Financial Reporting Directive/NFRD).

In addition to more transparency in terms of social culture and corporate governance, the goal is to disclose detailed progress in decarbonisation: keyword 1.5 degree target according to the Paris Climate Agreement. There is a three-stage plan for this. First, the CSRD applies to companies that are already subject to the NFRD.

With the NFRD, the EU introduced reporting requirements for "public interest entities" on 1 January 2017. Since then, companies, banks and insurance companies with more than 500 employees are obliged to disclose "transparent and responsible business conduct and sustainable growth" and to comment on "social responsibility". "Information on sustainability, such as social and environmental factors" should since then be disclosed by companies "in order to highlight threats to sustainability and to strengthen the confidence of investors and consumers."2

Around 11,700 companies have so far fallen under this NFRD reporting obligation, which are now to report for the first time in 2025 for the previous year (2024) in accordance with the new CSRD requirements. On the reporting dates of 1 January 2025 and 1 January 2026, all companies with more than 250 employees, a balance sheet total of 20 million euros and annual revenues of at least 40 million euros are to comply with the CSRD reporting requirements, regardless of whether they are listed on a stock exchange.It is therefore possible for a company to be exempt from consolidated financial reporting, but not from the requirements imposed on consolidated sustainability reporting.

Since (apart from small companies) almost all non-listed companies are also made liable, it can be assumed that this is intended to provide banks with information in order to be able to force them under state banking supervision to guide credit in the sense of green policy. Not explicitly, but nevertheless intentionally, the EU could push green finance further on the part of lenders. Companies that do not meet the requirements well enough could thus run into financing problems.

The following applies: The companies must fulfil at least two of the three criteria mentioned from the number of employees, turnover and balance sheet total. Small and medium-sized enterprises (SMEs) can allow themselves a time-out until 2028. This is provided for by a so-called opt-out.

According to EU estimates, the number of companies subject to reporting requirements will have more than quadrupled by the end of the year. In Germany alone, the number is expected to rise from around 550 to around 15,000 companies, according to the German Accounting Standards Committee (DRSC). In addition, the CSRD covers non-European companies that achieve a net turnover of 150 million euros in the EU and have at least one subsidiary or branch in the EU.

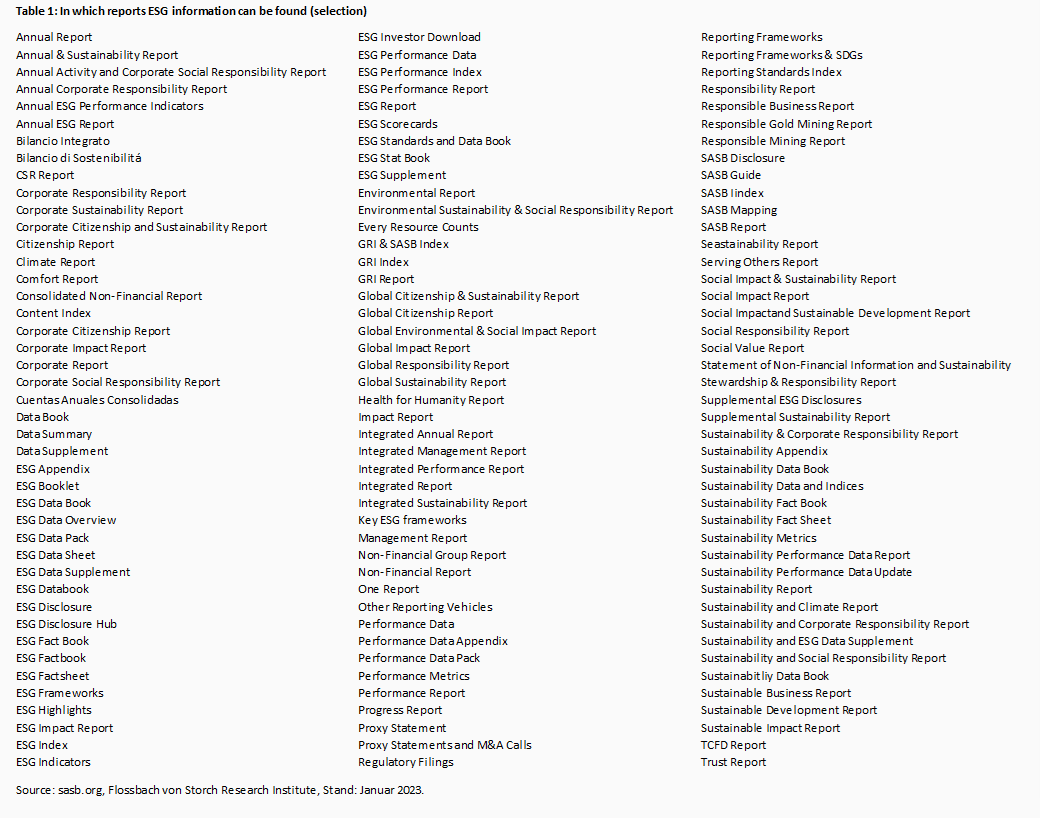

Besides, in theory this could in the best case put a stop to the proliferation of reports that are assigned to the ESG topic complex. In recent years, many companies have started to offer their readers sometimes more, sometimes less extensive reading material on the topics of climate, diversity, social protection and corporate governance.

However, it is not entirely clear where which information is hidden, as the reports in which ESG information is to be found are labelled differently (Table 1).

As can be seen from the labels, a whole range of sustainability initiatives play a role in reporting. In total, there are said to be more than 2000 global, national and regional reporting standards. In this country, for example, the Supply Chain Sourcing Obligations Act, which just came into force on 1 January, is quite well known.

The initiatives are partly complementary, but also partly in competition with each other. Some are already mandatory, others only have a selected circle of users. The addressees can also differ, for example into investors or other stakeholders.3

Johnson & Johnson, for example, links over 45 pages in its table of contents to the requirements of six initiatives: the Global Reporting Initiative (GRI), the Culture of Health for Business Framework (COH48), the Sustainability Accounting Standards Board (SASB) Standards, the Task Force on Climate-related Financial Disclosures (TCFD), the United Nations Global Compact (UNGC) and the Norges Bank Investment Management (NBIM) rules.4

Whether this scope will be sufficient to be able to continue to hold its own in terms of sustainability reporting in Europe and globally cannot yet be said with certainty.

But let's take it one step at a time.

It is important to know that the new CSRD rules of the EU have one thing in common with the NFRD rules they replaced: the concept of "double materiality". According to this, companies must not only indicate which sustainability aspects their business model has, but also assess how their business impacts on people and the environment.

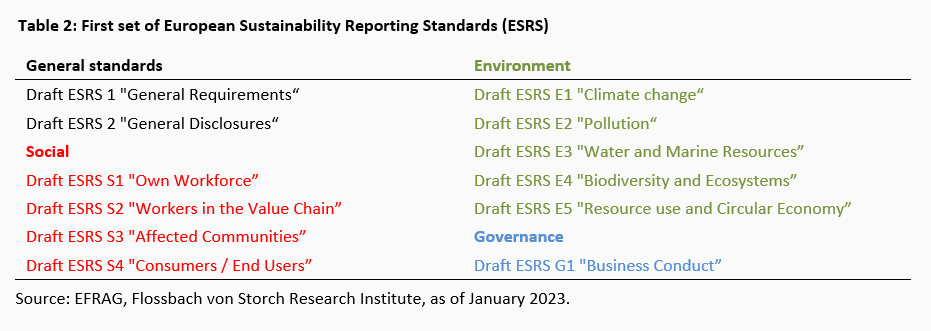

To ensure this, at least that is the EU's idea, a catalogue of detailed rules is now coming into being. To this end, EFRAG (originally European Financial Reporting Advisory Group), a private association based in Belgium on which the EU regularly relies for the technical implementation of accounting directives, has handed over the first set of final drafts for the new ESG reporting to the EU Commission.

These European Sustainability Reporting Standards (ESRS) currently comprise twelve drafts (Table 2).

After a reduction, 1144 disclosure requirements within 84 reporting requirements remain in these standards for the time being.5 Reporting companies are required to present sustainability information for the previous business year in the management report and to make it digitally identifiable (tagging). The possibility of publishing sustainability reports separately, as in the past, will therefore no longer exist according to the plans.

The EU Commission could now revise the content of the ESRS drafts. They should be adopted by 30 June this year at the latest.

It is unlikely to be changed that the EU demands precise information and ratios from the companies. After all, one goal is comparability. En passant, Brussels expects that the compulsion for transparency will ultimately motivate companies in their Net Zero efforts. Almost inevitably, however, this can only be the case if companies can actually represent such efforts credibly in their reports.

The standards or draft standards now available from EFRAG are to be followed by others, as expected by the audit and consulting firm Deloitte, for example. A second set of standards will contain detailed rules for SMEs and non-EU companies. Experts expect sector-specific standards to follow in time.

More or less in parallel, the deliberations of the International Sustainability Standards Board (ISSB), based in Frankfurt, are ongoing. The ISSB is an independent, but in any case private-sector body that develops and adopts the IFRS Sustainability Disclosure Standards (IFRS SDS) under the umbrella of the IFRS Foundation.

The Foundation also includes the International Accounting Standards Board (IASB), which is responsible for the well-known International Financial Reporting Standards (IFRS). The IFRS are accounting rules applied by companies in more than 160 countries. In the EU, the IFRS apply to all capital market-oriented companies for their consolidated financial statements; they are also applied voluntarily by numerous companies.

National and regional standards are to be able to build on the IFRS SDS, i.e. these additional rules for sustainability reporting. The ISSB wants to integrate existing international ESG standards into the framework.

To this end, the IFRS Foundation has now also taken the Sustainability Accounting Standards Board (SASB) under its wing. The SASB is a non-profit organisation that has developed industry-specific standards for the recognition and disclosure of "material" environmental, social and governance impacts for primarily US public companies. However, Deutsche Börse AG, for example, has also been using the SASB since the 2021 reporting year.

The SASB has drafted regulations for eleven sectors and their 77 industries. These are now to be the basis for the new IFRS SDS.

The goal of the IFRS SDS is global recognition, for which the US Securities and Exchange Commission (SEC) in particular would have to be brought on board. The USA is comparatively reserved when it comes to regulations on the ESG topic triad.

So far, there is no independent mandatory sustainability reporting. The SEC only requires companies to provide investors with "material information on ESG-related risks".

The voluntary disclosure strategy is working well. According to the New York-based Governance & Accountability Institute, 92 per cent of S&P 500 companies published sustainability reports for the 2020 financial year.

The average length of the reports was as diverse as the US corporate landscape. According to a study by Harvard University based on 200 sustainability reports from the S&P 500, the average length was 70 pages, ranging from 12 to 243 pages.6

Although sustainability reporting has already gained voluntary acceptance (one might assume also due to investor and social pressure), in June 2021 the US House of Representatives passed a bill entitled ESG Disclosure Simplification Act.7

This legislation would make several ESG-related reports mandatory for listed companies in their SEC filings. However, this has yet to be approved by the US Senate.

Independently of the Simplification Act, there is also a growing trend in the USA towards mandatory sustainability reporting, after the SEC drafted a corresponding regulation relating to greenhouse gas emissions.

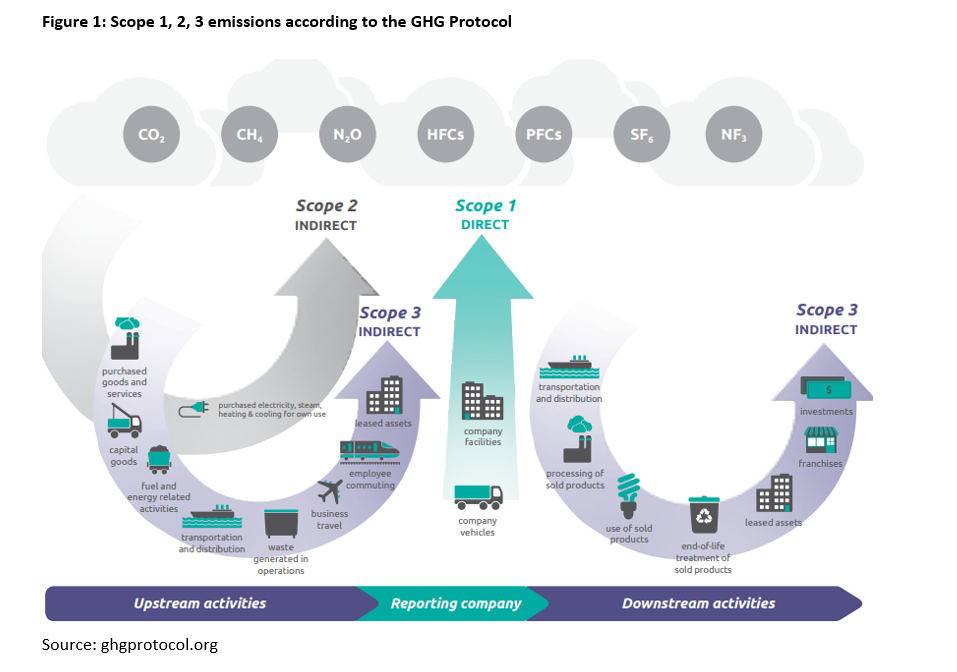

The most widely used international calculation tool, the Greenhouse Gas Protocol (GHG Protocol), divides these emissions into three categories or "scopes" (Figure 1).

Scope 1 is intended to capture the direct release of climate-damaging gases within the company itself. Scope 2 additionally records the indirect release of climate-damaging gases from energy suppliers.

Scope 3 is a controversial issue, as it is also intended to cover the indirect release of climate-damaging gases in upstream and downstream supply chains. Certainly not an easy undertaking: The GHG's Technical Guidance for Calculating Scope 3 Emissions alone is a 152-page guide.

The SEC regulation would require US-listed companies to disclose Scope 1 and Scope 2 emissions, including an audit requirement. In addition, companies would also be required to disclose emissions from their value chain (Scope 3) if they are material, or if companies have emissions targets that include Scope 3.

Regardless of the basic concept, critics fear multiple counting in Scope 3, because if a supplier also has to report, which is likely to be the case quite often, then its emissions would be recorded at least twice. Since companies have numerous cross- and cross-connections among each other, the danger is obvious that in the overall view emissions could be recorded additively and greenhouse gas emissions could be overstated.

In Europe, this danger is already real. Companies will soon have to publish Scope 3 emissions annually; a recalculation is planned every three years, according to EFRAG's draft ESRS.

The drafts of the ESRS that have been presented so far show what companies and ultimately the users of annual reports will have to get involved with. For example, companies are supposed to work with scenario analyses and name which climate changes will trigger their business or how these changes could influence their business.

In general, a company's total energy consumption in absolute terms, energy efficiency improvements, coal, oil and gas activities and the share of renewable energy in the total energy mix are required to be reported. For business "in sectors with high climate impacts", companies are to determine the total energy consumption per net turnover. In addition, there is disclosure of greenhouse gas (GHG) emissions intensity, again measured against net sales.

Companies should report the removal and storage of greenhouse gases from their own activities and the upstream and downstream value chain in metric tonnes of Co2 equivalents. In addition, there should also be information on the amount of GHG reductions or their removal from climate protection projects outside the value chain that a company has initiated, for example, with the purchase of emission credits.

The "potential financial impact of material physical risks" and "the potential financial impact of material transition risks" are to be measured. In addition, companies are to determine how they might be able to take advantage of "material climate-related opportunities".

This is one of the many provisions of the draft ERSR E1 Climate change.

Climate-related physical risks are defined here as risks "arising from the physical impacts of climate change. They typically include acute physical risks arising from specific hazards, especially weather-related events such as storms, floods, fires or heat waves, and chronic physical risks arising from longer-term changes in climate, such as temperature changes, sea level rise, reduced water availability, loss of biodiversity and changes in land and soil productivity".

Companies must also "briefly" explain how the climate scenarios used are consistent with the critical climate-related assumptions in their financial reports. And, important to note: These scenarios and scenario calculations, as well as their sources, should be consistent with state-of-the-art science.8

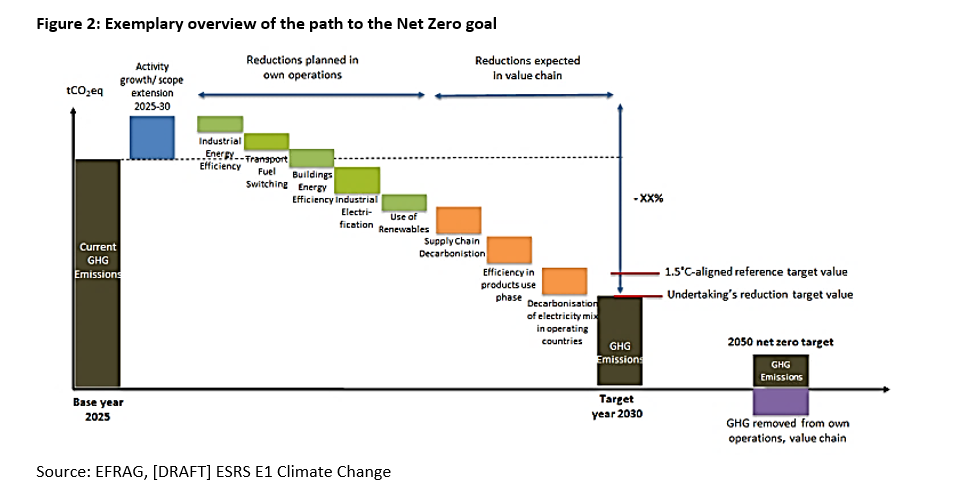

According to the standard, an exemplary overview looks as follows (Figure 2).

However, how all this data and its potential impact on global warming and corporate financial performance can be validly captured and processed is unknown. The ESRS themselves acknowledge that there is currently "no generally accepted method" to "assess or measure how material physical and transition risks may affect the entity's future financial position".

And the disclosure of these impacts would depend "on the company's internal methodology and the exercise of discretion in determining the inputs and assumptions".

What applies to the requirements for climate change may certainly also apply to the rules for business conduct. Here, for example, companies are required to disclose lobbying. The question is where exactly lobbying begins and where it ends.

It should be easier for managers to sign that companies respect human rights. Information on diversity in the company, such as skin colour or gender, should not be a challenge either.

But if oil and gas companies are to report on reserves in conflict areas, or those in the vicinity of "indigenous land", then there are likely to be demarcation problems. Such disclosures are required by the SASB, which are supposed to be the basis of the IFRS SDS rules.

The problem with the IFRS SDS: They have an investor focus and less of an eye on "double materiality". The previous drafts of the ESRS and the IFRS SDS (draft S1 and draft S2 are available here) have common features, for example in that they take into account the framework of the Task Force on Climate-Related Financial Disclosures.

But the ESRS go beyond the IFRS SDS. However, the former will soon be mandatory for companies in any case. Despite consultations between the respective standard setters, there is a danger that there will be at least two comprehensive sets of rules for sustainability reporting in the foreseeable future, which have or should have a guiding character for companies and their addressees.

However, the ISSB recommends that the IFRS SDS should, for example, introduce an exemption that would allow entities to exclude sensitive sustainability information relating to their business in limited circumstances. An example of such an exemption is the launch of a new "sustainable product".

It is still unclear when the IFRS SDS rules will come into force. In addition, the USA could set additional accents in terms of ESG. The additional effort would then not only be on the part of the companies, but of course also on the part of the addressees.

Basically, it should be noted that even the classic IFRS are far from being fully developed; on the contrary, there are major gaps. For example, the rules for the recognition of intangible assets lag far behind the economic reality of many companies. 9

In addition, IFRS (and US Generally Accepted Accounting Principles/US GAAP) lack valid specifications for the income statement. Therefore, companies like to operate with non-IFRS (or non-GAAP) figures. A danger that certainly also exists with the new natural capital accounting. Since CSRD reporting is in future to take place exclusively in the management report - planned in a separate section - it is subject to an external audit obligation. This task is likely to be taken on regularly by the auditor, who has so far already certified the annual report.

Alternatively, the market for sustainability certifiers could grow, whose companies would certainly be happy to give their seal of approval in exchange for an adequate fee, of course. However, this in turn could cause problems for the company's management, in coordination between the supervisory board and the board of directors, for example, on the question of which seals may be presented to the stakeholders as suitable.

There is no doubt that the question arises as to the qualifications of the external auditors on the subject of ESG. Even the usual requirements for the management report are not always met by companies, especially in times of crisis.10 Nevertheless, management reports are regularly waved through by the auditors. In the annual reports examined by the German Financial Reporting Enforcement Panel, which will be discontinued at the end of 2021, management reports were regularly one of the most frequent sources of error.11

It is questionable to what extent auditors can understand, for example, whether a company "generates a good four euros for society" for every euro it generates itself, as a large European chemical company claims in its sustainability reporting.

Can it really be accurately tracked whether a global gold mining company recycles and reuses 79 per cent of its water, as claimed?

And how the pollutant emissions of the products of the automotive industry look in the laboratory, i.e. on paper, and in practice, has been reported on sufficiently in recent years.

In addition, the comparability of companies will almost certainly remain a noble wish. This is already shown by the major shortcomings of ESG ratings.12

"I think investor pressure is one of the strongest motivators for companies to act," former Colorado Oil & Gas Association president Tisha Schuller said last December, according to a report by S&P Global.

Robert Wood Johnson would probably agree: "Our ultimate responsibility is to our shareholders. We must experiment with new ideas. Research must be done, innovative programmes developed, investments made in the future and mistakes paid for."

And perhaps that is why the first prominent major investor is now going its own way again. In December, the US asset manager Vanguard left the climate neutrality initiative Net Zero Asset Managers in a high-profile move. The world's second-largest asset manager, with eight trillion dollars in assets under management, explained that it wanted to preserve its independence by leaving the initiative and that it alone could better assert the interests of its investors. Moreover, a multitude of such initiatives could rather cause confusion.

Even more companies will soon be required to account for their actions in relation to ESG. In particular, they will be required to disclose their individual decarbonisation path transparently in line with ESRS and possibly a different IFRS SDS scheme.

The apostrophe is a global standard. The fact is that even decades of efforts to establish globally uniform accounting rules, at least for capital market-oriented companies, have failed. Based on this experience, it is doubtful whether this will be possible for ESG rules.

Whether the hope associated with the rules to curb greenwashing will be fulfilled is questionable. For externally, the extensive assumptions and information that companies have to fulfil are at best anecdotally verifiable.

And it is also doubtful to what extent enforced transparency will help to achieve the politically formulated 1.5-degree climate target better than on the basis of voluntary disclosures. Companies that have had little to do with transparency in the past will hardly shine in the future when it comes to ESG. At least if sanctions remain the exception, as they have been so far.

Voluntary disclosure would enable companies not to cheat, but to honestly state which assumptions and information based on them are possibly only very rough estimates - or no longer provide any information at all due to a lack of robust data.

In addition, companies may hide risks in the ESG chapter of the management report that investors tend to suspect elsewhere.

A further information overload in annual reports could lead to investors not finding a more useful basis for their investment decisions, as they would like, but a more useless one.

Now, no one has to assume that the (mostly short-term) employed manager always behaves like an honourable businessman. But the general social and political pressure as well as the power of investor money should be great enough to urge most companies to manage well, also in the sense of an efficient, sparing, socially just use of resources - as Robert Wood Johnson once aptly put it.

2https://eur-lex.europa.eu/legal-content/DE/TXT/?uri=celex%3A32014L0095

3 an overview and classification of the relevance for German companies can be found in an essay by Isabel von Keitz, Inge Wulf, January 2023, KoR, pages 27-38

4https://healthforhumanityreport.jnj.com/reporting-hub/esg-disclosure-index-pdf#

6https://corpgov.law.harvard.edu/2021/11/02/the-state-of-u-s-sustainability-reporting/

7https://www.congress.gov/congressional-report/117th-congress/house-report/54/1

8 [DRAFT] ESRS E1 Climate Change, Page 25

9 Christof Schürmann, When tangible assets are missing from the balance sheet, March 2022, https://www.flossbachvonstorch-researchinstitute.com/de/studien/wenn-greifbares-vermoegen-in-der-bilanz-fehlt/

10 See, for example, France Ruhwedel,Thorsten Sellhorn, Julia Lerchenmüller, 2009, Forecast Reporting in Upswing and Crisis: An Empirical Study of DAX Companies.

11 See for example Activity Report 2019, https://www.ey.com/de_de/ifrs-veroeffentlichungen/andere-standards/dpr-taetigkeitsbericht-2019

12 Kai Lehmann, Sustainable? Yes...No...Maybe! On the lack of comparability of ESG ratings, November 2019, https://www.flossbachvonstorch-researchinstitute.com/de/studien/nachhaltig-janeinvielleicht-zur-mangelnden-vergleichbarkeit-von-esg-ratings/

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.

Christof Schürmann

Senior Research Analyst

At the Institute since 2022. The graduate in business administration (FH), previously worked as a journalist and deputy head of "Money" at WirtschaftsWoche. The trained banker and book author ("Die Bilanztrickser") taught balance sheet research part-time at the private university BiTS in Iserlohn.

All articles by Christof Schürmann