21.02.2024 - Comments

The inflation rate peaked in the US and the eurozone in June and October 2022 respectively. It quickly declined thereafter and is now much lower, but still above the 2% inflation target. What should central banks do now? In line with James Carville's famous admonition to Bill Clinton “It's the economy, stupid!”, the Fed's and ECB's monetary policy today could be: “It's the productivity, stupid!”

At the beginning of 2021, inflation rates in the USA and shortly after in the eurozone surged past 3% for the first time in a decade. With vaccines available and pandemic restrictions easing, consumers eager to spend their savings encountered ongoing global supply chain bottlenecks. Thus, a high demand met a limited supply, allowing for the absorption of the substantial monetary expansion through price increases.1

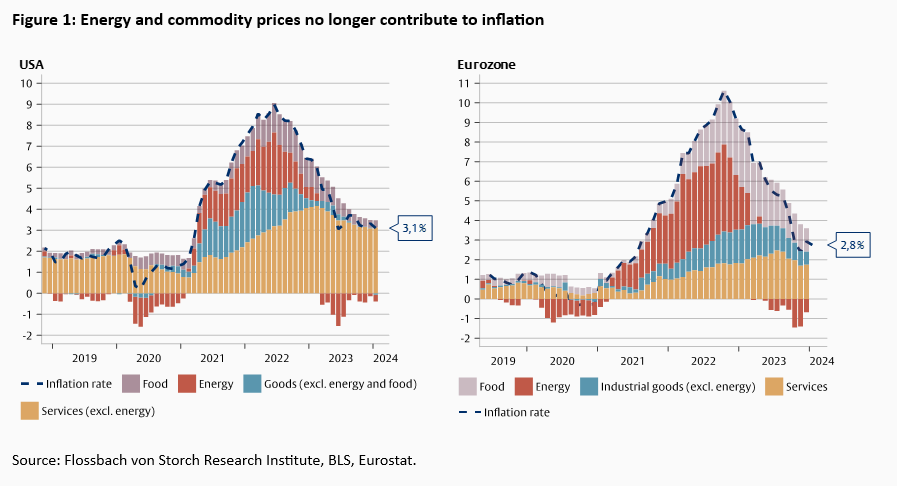

Initially, goods and energy prices drove inflation, which later extended into the service sector (Fig. 1). The outbreak of war in Ukraine in early 2022 and the subsequent sanctions against Russia exacerbated the inflationary impact of energy and food prices, especially in the eurozone. Meanwhile, the inflation contribution from services steadily increased. Today, the rate of price increases for energy and goods has normalized, and inflationary pressure mainly resides within the service sector.

Price increases in the service sector closely relate to wage development. Since services tend to be more labor-intensive than manufacturing, wages are the largest cost factor for service companies. Rising wages incentivize companies to either increase prices or improve productivity to maintain profits, making rising wages inflationary depending on productivity growth.

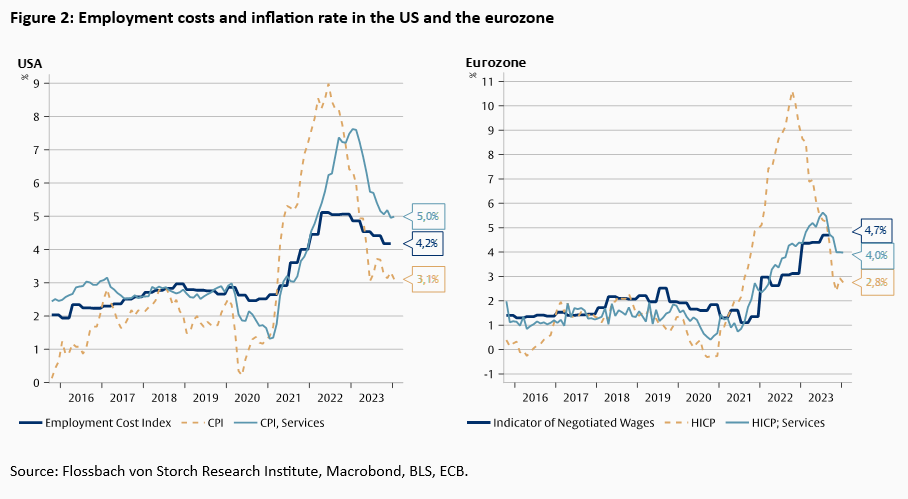

While wages in the US and the eurozone have shown similar trends, their productivity growth diverges. In 2022, wage costs in the US grew by more than 5%, and by the end of 2023, by 4.2% year-over-year, significantly above the pre-pandemic rate of 3% (Fig 2). In the eurozone, wages had risen by 4.7% by the end of 2023, also faster than before the pandemic. Service prices increased at the same time. Productivity, measured as real GDP per employed person, increased by 15% in the USA since 2012 but stagnated in the eurozone (Fig 3). The modest productivity gain of 2% in the eurozone until 2019 has reversed in recent years.

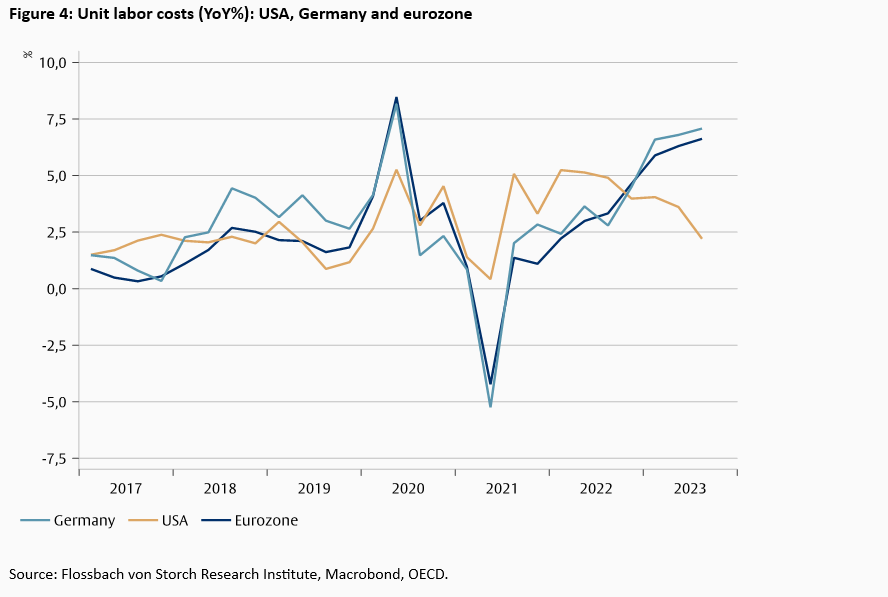

The slower productivity growth in the eurozone leads to higher inflationary pressure than in the US, as unit labor costs rise faster (Fig 4). If wages increase more quickly than productivity, companies face higher costs to produce the same amount of goods or services. To compensate, they raise their product prices. In the US, unit labor cost growth has been declining since early 2022, while it continues to rise in the eurozone. With several wage negotiations pending in eurozone countries, wage cost pressure is likely to increase further. Without compensatory productivity growth, inflationary pressure in the eurozone is expected to remain high.

Due to stagnant productivity, wage increases in the eurozone are more inflationary than in the US. The ECB seems to be aware of this relationship. In its last interest rate decision, ECB President Christine Lagarde emphasized the importance of wage development for the upcoming rate decisions. Unless there's a significant economic downturn to reduce labor costs, the ECB will need to keep its benchmark interest rates higher for longer. Given the lower inflationary pressure, the Fed might consider rate cuts sooner, though not as quickly or sharply as the markets might hope.

1 See Duarte, Pablo (2023) “Someday inflation will also be "transitory”, Comment, Flossbach von Storch Research Institute.

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.