28.06.2023 - Comments

Despite the normalization of energy and consumer goods prices, inflation remains undefeated. At some point, inflation will come down again, and like everything else in this world, inflation will then also have been "transitory”.

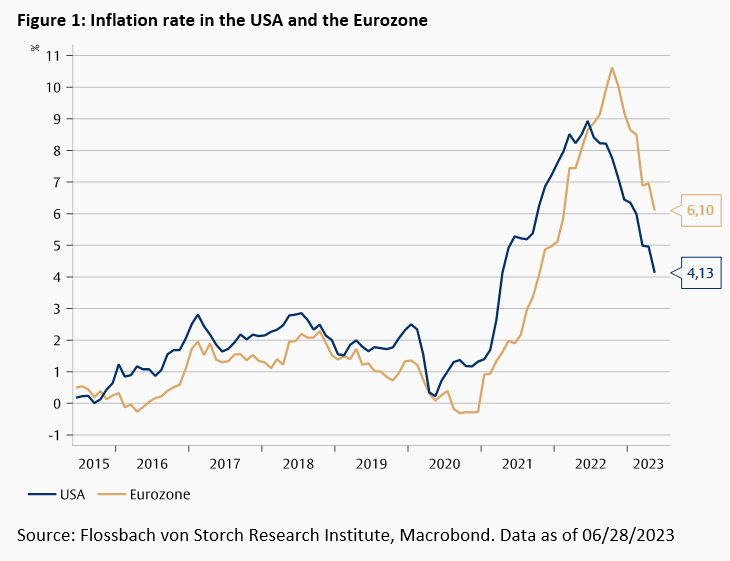

Inflation rates in the U.S. and the euro zone have been falling for several months. Some celebrate this as the final defeat of inflation and see it as confirmation that it was ultimately "transitory." However, this raises two problems. First, it is always possible to find a sufficiently long period of time to call a secular phenomenon "transitory," which ultimately renders the term meaningless. Second, inflationary pressures do not seem to have disappeared completely. In fact, inflation rates could rise again. Inflation will eventually pass again, but probably not anytime soon.

In the USA, inflation surpassed the target rate of 2% at the beginning of 2021, and later on, the euro area also experienced this. At that time, central banks responded with a delay to tighten their highly expansionary monetary policies, as the prevailing narrative suggested that these elevated inflation rates were temporary ("transitory"). The assumption was that inflation rates would naturally decrease once the supply chains, which were previously disrupted by pandemic lockdowns, returned to normal. Everything seemed to be under control.1

But things turned out differently. More than two years later, inflation rates are still noticeably above the 2% target. The US Federal Reserve (Fed) and the European Central Bank (ECB) reacted with considerable delay.

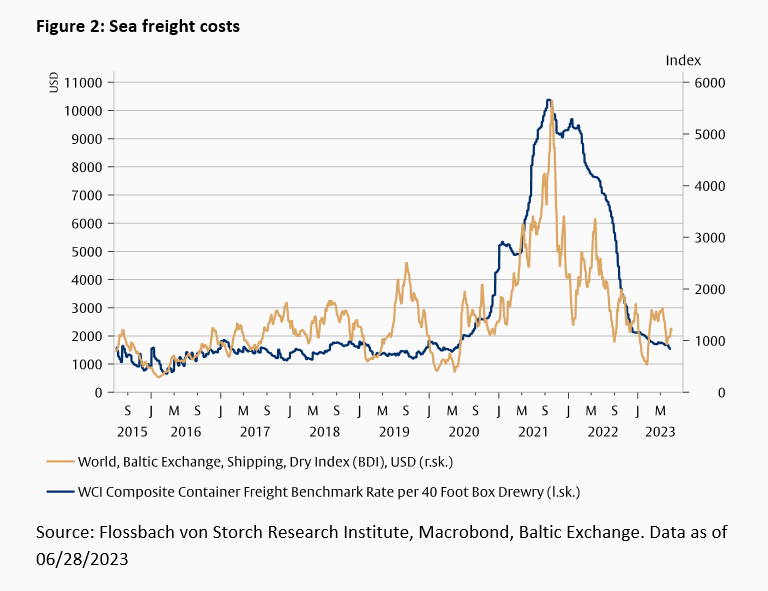

The main contribution to the return of inflation came from the supply side after the pandemic. In both the USA and the euro area, bottlenecks in the supply chains drove up prices for many consumer goods. At the same time, raw material and energy prices also rose. The outbreak of war in Ukraine drove oil and gas prices up even further and inflation rates to levels not seen since the 1970s. These prices have fallen in recent months. The cost of transporting goods, for example, has returned to pre-pandemic levels. As bottlenecks in supply chains have been resolved and energy prices have fallen despite the war, inflationary pressures on the supply side appear to have eased.

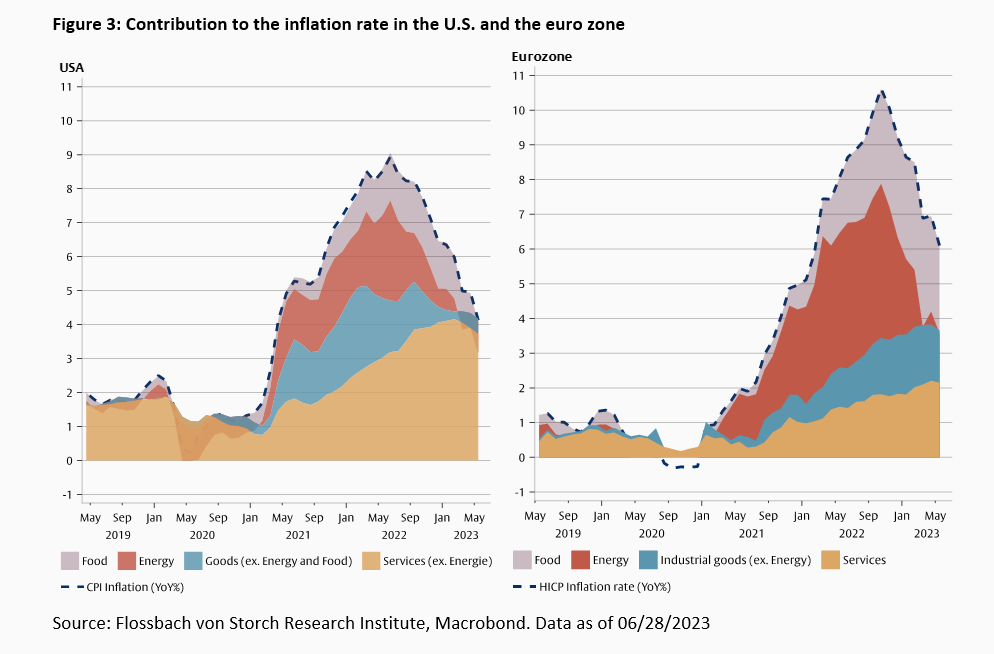

However, the rise in inflation is not limited to commodities and consumer goods. In the US, prices for services have risen steadily and are now the biggest contributors to inflation. In the euro zone, inflationary pressure is increasing in service and food prices. Wages have also been rising faster in both the eurozone and the US. So far, increases in service prices and wages do not appear to be abating. Inflationary pressures have moved from raw materials and consumer goods to services and food.

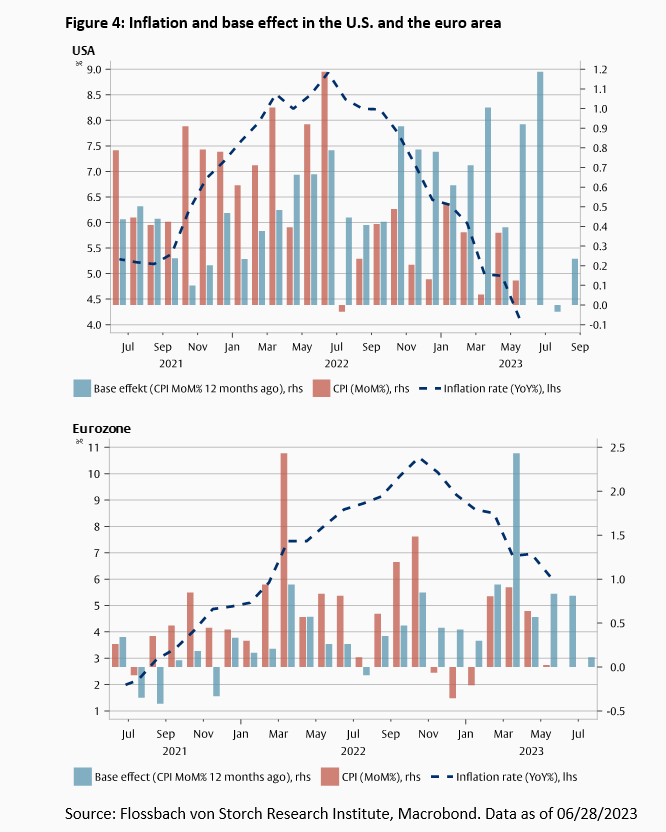

The year-on-year decline in the inflation rate that we have observed in recent months is overstated by the base effect. The year-on-year inflation rate, which is most frequently observed and discussed, also rises or falls depending on how inflation developed in the previous year. The annual inflation rate can remain at the same level only if the price index increases by the same amount each month as it did twelve months ago. In the first half of 2022, there was a sharp increase in the price index as a result of war-related increases in the cost of energy and raw materials. Therefore, a high but less pronounced monthly increase this year will lead to an oversubscribed reduction in the year-on-year inflation rate.

The base effect can be seen in the charts below. The blue line indicates the annual inflation rate. The red bars are the monthly changes in the price index, and the blue bars are the monthly changes in the price index twelve months earlier. The annual inflation rate decreases when the blue bars are larger than the red bars. This also happens when inflation remains above the central banks' target.

Inflationary pressure has persisted since the end of last year (red bars). In the USA and the euro zone, prices have risen at monthly rates averaging 0.3% and 0.4%. The annualized rates were 3.5% and 5.3%. As monthly rates were lower than twelve months ago, the year-on-year inflation rate fell sharply. This decline is overstated by the base effect.

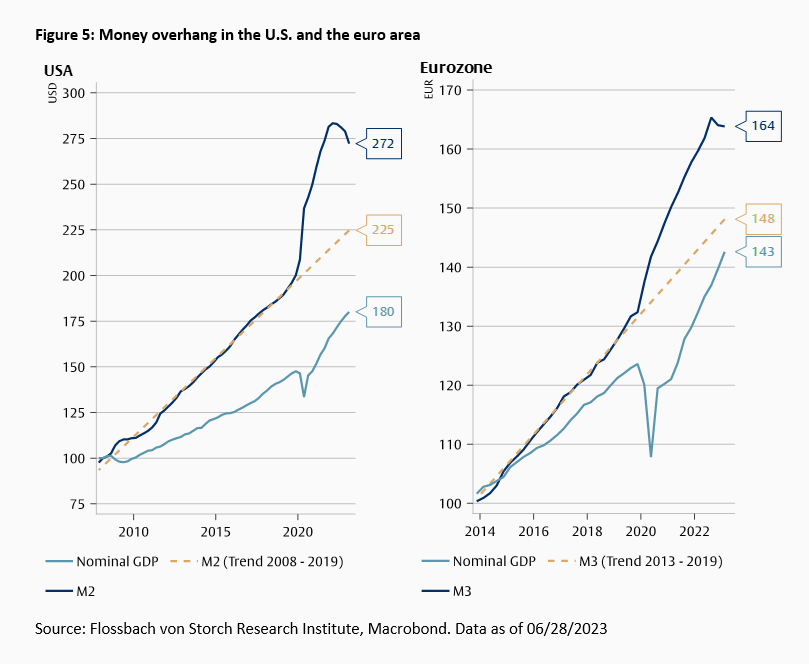

Without monetary expansion, the rise in inflation would not be possible. Without monetary expansion, for example, an increase in energy prices would lead to a readjustment of the demand for energy and other goods in line with the budget constraints of households. Relative prices would adjust, so that some prices would rise and others would fall, but the overall price level would remain stable. Aggressive monetary expansion at the beginning of the pandemic in 2020 created the monetary space that allowed inflation to rise thereafter. As people were isolated in their homes and supply chains were disrupted, and services in particular failed, this money accumulated in bank accounts. As the pandemic ended, the forced savings found their way into consumer demand. Since supply could not grow as fast as demand, prices began to fill the monetary space created by central banks. The reduction in the money supply started late and is still happening slowly. This means that prices still have monetary space to rise further.

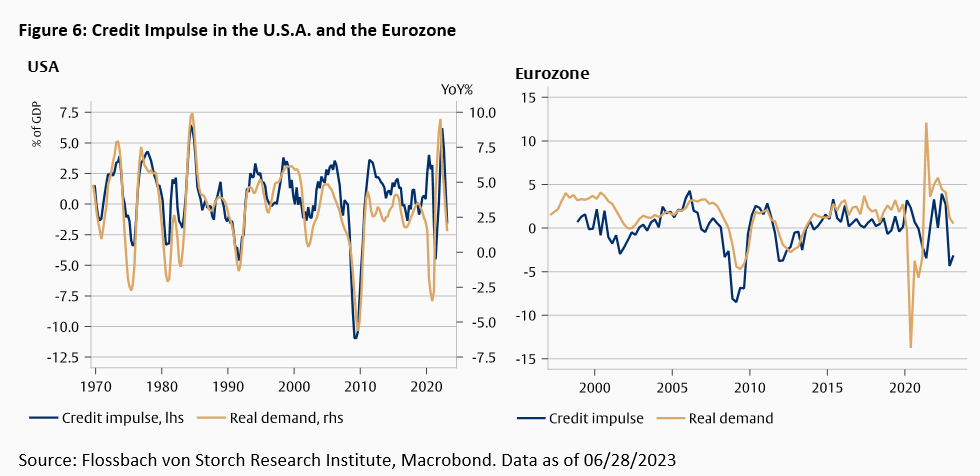

Monetary policy is transmitted to the real economy via the financial sector with a lag of more than a year. The increase in key interest rates by central banks makes credit more expensive, which reduces aggregate demand. The credit impulse, i.e. the change in the flow of credit from the financial sector to the private sector, has been a good indicator of real demand. In the USA and the euro zone, credit flows have fallen sharply. Consequently, inflationary pressures could ease thanks to a decline in aggregate demand.

Overall, the normalization of energy and consumer goods prices and the slowdown in the flow of credit point to easing inflation. But inflation has not yet been defeated. Eventually, inflation will subside, and like everything else in this world, inflation will have been "transitory" by then.

1 See Duarte (2021), „Inflationsnarrative bestimmen das Schicksal der Zentralbanken“, Comment, Flossbach von Storch Research Institute, 09.03.2021

09.03.2021 - Macroeconomics

by Pablo Duarte

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.