05.01.2024 - Comments

Looking back at the past stock market year, the first impression one gets is that shares from Germany were quite successful. The shares of German companies achieved a combined performance of 19% in 2023.1 Of this, 15 percent was attributable to price gains and the remaining four percent to dividend payouts.

This is an extremely pleasing statistic when you consider that in the previous ten years, the arithmetic average annual return on the German stock market as a whole was just eight percent, or five percent excluding dividends. A rolling investment in a short-term German government bond would have generated a return of just 3.1% in 2023.2

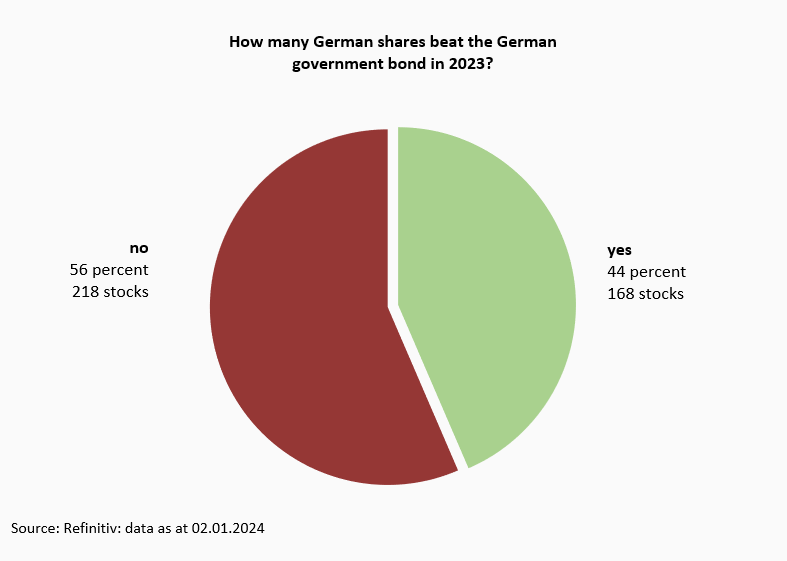

However, the statistics hide the fact that individual German stocks performed rather poorly last year. Only 44% of all German equities outperformed the short-term federal bond. In contrast, the majority (56%) of all German equities were unable to outperform the German government bond. This is a poor figure even by historical standards. In the past five years, 53% of German equities outperformed the German government bond.3

The comparison of stock returns and consumer price inflation, which was at 3.7% in December 2023, comes to a similar conclusion. An individual investment in 43% of all German shares would not compensate for inflation in 2023.

The probability of beating the German government bond or receiving an inflation compensation with a blind selection of a stock was lower than being right in a coin toss.

The reason why the overall market did well, but the majority of individual stocks did not, lies in the calculation method. Market and portfolio returns are calculated like a value-weighted index. In a value-weighted index, shares are included in the performance calculation in proportion to their market capitalization. Large stocks with a positive performance carried the overall market. Smaller stocks with a poor performance therefore only had a minor impact on the overall performance.

The differences in size become even more significant when looking at the value created for investors on the German stock exchange. Taken together, the 386 German shares created a value of 223 billion euros for their investors in 2023. The value corresponds to the sum of all dividends paid out plus the increase in the share price, which exceeded the yield on the short-term federal bond. For comparison: in the four previous years (2019 - 2022), an average annual value of EUR 110 billion was created for investors on the German stock market.

In purely mathematical terms, each of the 386 shares accounted for EUR 579 million of the EUR 223 billion in value created in 2023. But here, too, the statistics are deceptive. In 2023, value creation was more concentrated than it had been for a long time.

Just under a quarter of the total value created on the German stock market in 2023 was attributable to SAP shares alone. A further 14% of the total value was created by Siemens shares alone. 18 shares were already enough to account for the total value created on the German stock market in 2023.

The remaining 368 companies together did not create any value. Although half of them created a value of 86 billion euros, the other half destroyed a value of the same amount. Large companies whose shares performed poorly in the past stock market year contributed particularly strongly to the destruction of value.

Although value creation on the German capital market was also concentrated in the past, the concentration was particularly high in 2023. In the period from 2003 to 2022, one tenth of the shares traded were sufficient to achieve full value creation.4 Last year, five percent of shares (18 out of 386) were already sufficient for this.

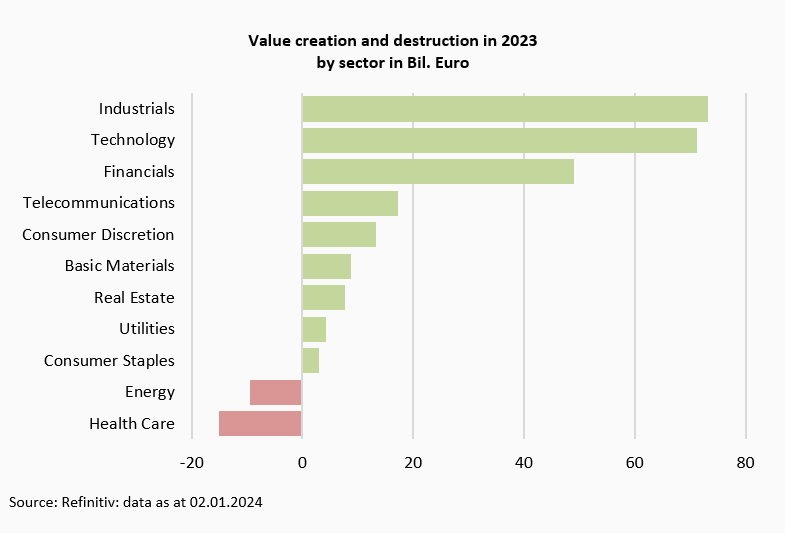

Looking at value creation by economic sector, the industrial goods sector accounted for the largest share, driven by shares in Siemens and Deutsche Post. In the technology sector, shares in Infineon Technologies and Nemetschek made a significant contribution to value creation alongside SAP. In the financial services sector, shares in Allianz and Munich Re were the main contributors to value creation.

In the healthcare sector, only a third of the shares contributed to value creation, but the number and size of the remaining shares outweighed the value destruction. In the energy sector, all shares caused value destruction.

For the German capital market year 2023, it can be stated that there were only a few stocks across the capital market with which the majority of all investors were able to make money. Uninformed investors had a worse chance of beating the German government bond or receiving inflation compensation than if they had bet on a coin toss. Investors who relied on participating in the winners by investing in an index automatically bought into the losers, who were in the majority last year.

The trick for investors last year was to identify the few stocks that contributed to value creation on the German capital market at an early stage.

Finally, investors should always be aware that looking at returns based on calendar years involves a certain degree of randomness. If a calendar year were to come to an end at the end of October, the German capital market would only achieve a return of 11% instead of 19% within twelve months and the year would no longer look so exceptionally good.

1 Refers to all 386 shares of German companies that are traded in the General and Prime Standard on the Deutsche Börse and thus represent the German stock market. At the beginning of the year, 383 companies were traded, 26 were delisted in the course of the year and three new shares were added. The CDAX share index comprises these stocks. Historical performance is not a reliable indicator of future performance.

2 Cumulative monthly return on an investment in a German government bond with one month to maturity. Historical performance is not a reliable indicator of future performance.

3 Compare Immenkötter (2021): „Das Risiko der einzelnen Aktie“, Flossbach von Storch Research Institute.

4 Compare: Immenkötter (2023): „Value Creation and Value Destruction on the German Stock Market“, Flossbach von Storch Research Institute.

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch SE. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch SE remains solely with Flossbach von Storch SE. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch SE.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch SE.

© 2024 Flossbach von Storch. All rights reserved.