15.01.2021 - Comments

Click here for the Real Economy Tracker

With the first Corona-Lockdown, global GDP slumped between 4% and 5% overall in 2020.1 First, China's GDP fell by 6.26% year-on-year in the first quarter of 2020. In the second quarter, the major industrialized nations followed suit: GDP in the US fell by 9.03% and in the Eurozone by 14.71%. The rapid recovery in China in the second quarter, driven by the industrial sector, was followed by the Eurozone (especially Germany) and the US in the third quarter of 2020. The recovery, however, was slowed down again by a second wave of infections in autumn and winter and the following lockdown measures. A new mutation of the coronavirus, spreading faster than the original variant, prompted governments to extend the renewed measures and travel restrictions in early 2021. The danger of a "double-dip recession" looms.

The effects of the second lockdown wave follow a similar pattern in Europe and the USA as during the first wave. In late 2020-Q1, the first restrictions the first lockdown were impsoed. In the second lockdown, governments started to shut down public life in 2020-Q4. Schools, retail stores, hotels, restaurants were closed, and other areas of public life were restricted. Factories and businesses, however, have remained open until now. In 2020-Q2 came the big slump followed by a recovery in 2020-Q3. Similar developments could now occur in 2021-Q1 and 2021-Q2. The developments in 2020Q1 - 2020Q3 could therefore serve as a pattern for assessing the development of the real economy in 2020Q4 - 2021Q2.

Lockdown 1 and 2 compared

People's mobility decreased almost as much in the second lockdown as in the first. Based on smartphone location data, applications such as Google Maps can be used to determine the number of visits to different locations, such as retail stores or transit stations. Because many users save the address of their workplace in Google Maps under the category "workplace", the number of visits here can also be determined. Google collects this data and publishes a mobility index. In Germany, the mobility index in all areas (workplaces, retail, transit stations) dropped even lower during the second lockdown than during the first. In France, the drop in mobility was between 67% and 80% of the drop in the first lockdown (Figures 1 and 2). In the U.S. (Figure 3), mobility data related to jobs and at transit stations fell almost as low as in April. On average, the recent drop in mobility data was 78% in the Euro Area2 and 81% in the U.S., relative the drop in the first lockdown.

The service sector was hit hardest in both lockdown episodes. As in the first lockdown, hotels, restaurants, and retail stores were closed in late 2020 to contain the accelerated spread of the virus. Figure 4 shows internet search intensity for the terms "hotel" and "restaurant" in 2020 relative to the average of the previous four years, with negative values indicating a decline in search intensity with respect to previous years. During the second lockdown, search intensity in Germany and France in particular, fell by a similar amount as in the first lockdown. In the U.S., the decline was not as sharp as in the Eurozone countries. On average, the decline in the Eurozone was 85% and in the USA 55% of the decline in the first lockdown.

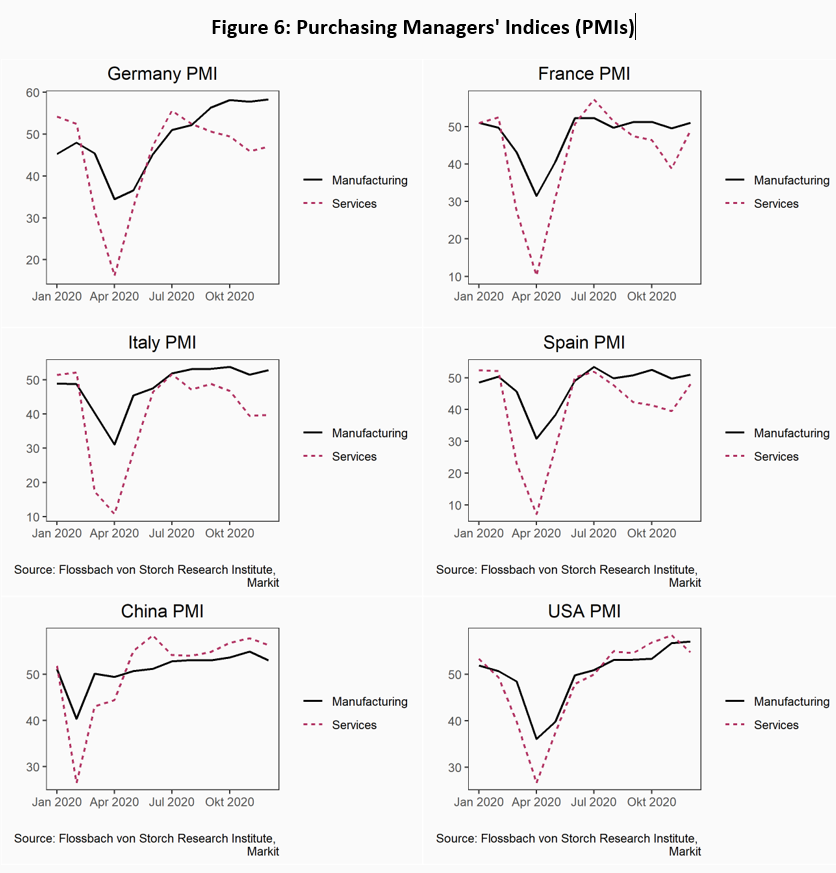

In contrast, industrial production in the Eurozone, especially in Germany and in the USA, maintained its momentum. While in the first lockdown, plants had to close and production stopped in most industries, the trade-offs governments considered for the second lockdown were different. The Purchasing Managers' Indices (PMIs) up to December 2020 show that, unlike the services sector, industry has this time hardly seen a decline, as opposed to April 2020.

Electricity consumption, a "real-time indicator" of industrial activity, fell significantly during the first lockdown relative to the average of the previous four years. In France, electricity consumption fell in November (during the second lockdown) but recovered strongly in December and January 2021. In Germany, electricity consumption fell in December 2020 (relative to previous years) but rose again in 2021. Overall, the decline in electricity consumption in the Euro Area is 33% and in the US 27% of the decline in the first lockdown.

Overall, the decline in economic activity in the second lockdown does not seem to be as severe as in the first, as shown by the development of industrial production. Mobility data decreased in the second lockdown by 78% in the Euro Area and 81% in the US relative to the first lockdown. Service sector activity fell by 85% in the Eurozone and 55% in the US relative to the decline in the first lockdown, according to Google Trends statistics. Electricity consumption fell by 33% in the Eurozone and 27% in the US relative to the first lockdown.

Assuming that this trend does not change much over the coming weeks, it is possible to estimate GDP growth in 2020Q4-2020Q2 as a share of the growth in 2020Q1-2020Q3. How high this share would be can be derived from the estimates above: weighting production with 60%, mobility with 20% and Google Trends statistics with 20%, we get a share of 43.5% for the US (mobility 81.3%*0.2 + services 26.8*0.2 + electricity consumption 27%*0.6). For the Eurozone the share would be 52.5% and for Germany 65.1%.

We weight electricity consumption somewhat more heavily than the other variables because mobility has strong seasonal fluctuations and Google unfortunately does not provide data on previous years to adjust for it. The fact that, for example, trips to work declined in the last few weeks of December is likely to have been due, not only to the lockdown, but also to the holidays and usual company closures. In addition, the hotel and restaurant sector does not contribute as much to economic development in the major industrialized countries.3

A simple simulation of GDP growth under the above assumptions shows that in 2021-Q1 GDP could fall by 4.4% in the USA and by 6% in the euro zone compared with the previous quarter. The recovery in 2021-Q2 would be 3.6% in the U.S. and 6.4% in the eurozone. Because mobility and service sector activity in Germany fell slightly more than in the first lockdown, we calculate a decline of 6.4% in 2021-Q1 and a recovery of 5.6% in 2021-Q2. Assuming a growth rate of 1% for Q3 and Q4, growth in 2021 as a whole would be just under 0.5% in the eurozone and 0.1% in the US. In Germany, the economy would contract by -1.3%. Germany could expect real GDP to stagnate if the changes in 2020-Q4 - 2021-Q2 were only 42% instead of the 65.1% we calculated for 2020-Q1 - 2020-Q3.

It is possible that the developments could be even worse than assumed in the simulations. Mutations of the virus have already led to greater travel restrictions between the UK and neighboring countries. It is possible that there could even be factory and business closures. In that case, industrial production, which has been spared so far, would also be affected. In recent days, there have also been reports of new outbreaks and renewed lockdowns in China. Should a second infection wave develop, further lockdowns could also weaken the Chinese economy.

Overall, our examination of the high-frequency indicators and the simulation derived from them for the development of real GDP show that economic forecasts published in the fall/winter of 2020 could soon be revised significantly downward. Whether this could impress the financial markets is another question. If past behavior patterns remain in place, the markets are likely to look ahead and benefit from the expectation of new liquidity floods from central banks.

1 See Global Economic Prospects, January 2021, The World Bank und OECD Economic Outlook 2020.

2 The average is calculated by using the indicators from the 4 largest countries in the Eurozone, namely Germany, France, Italy, and Spain.

3 Within the Eurozone, the relevance of these sectors varies. In our Real Economy Tracker, we present an activity index that summarizes the dynamics of all economic sectors and takes into account the differences between countries and sectors.

28.09.2020 - Macroeconomics

by Pablo Duarte

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.