30.04.2024 - Studies

"First we had no luck and then we had bad luck". The well-known saying of former Bundesliga striker Jürgen "Kobra" Wegmann (Borussia Dortmund, among others) is likely to be on the lips of one or two company managers when the going gets tough in terms of profit development.

Take Thomas Cangemi, for example. Until recently, Cangemi was head of New York Community Bancorp (NYCB). The share price of the US regional bank plummeted by 44 per cent within hours at the end of January following the announcement of a net loss of USD 260 million in the fourth quarter. The reason for this was provisions for problematic property exposures.1

One month later, Cangemi not only declared that this loss had increased to 2.7 billion dollars, but also announced his resignation after 27 years with the bank. The NYCB had just admitted to overvaluing goodwill by 2.4 billion dollars. The share price plummeted once again - to a 27-year low. A few days later, a capital increase brought some calm to the bank and the share price.

Goodwill is an item on the assets side of the balance sheet and represents the premium (less possible amortisation) that companies, insurers or banks have paid on the equivalent value of the acquired assets of new subsidiaries following takeovers.2

In theory, goodwill is supposed to reflect synergies that management boards hope to realise from company takeovers. As these cannot be permanent, goodwill must sooner or later disappear as a balance sheet item. Until a good 20 years ago, this was ensured by regular amortisation prescribed by the accounting rules.3 In addition, special write-downs were required if hopes for savings, sales or cash inflows from takeovers did not materialise.

For a good 20 years now, only such irregular, but in any case timely, devaluations should show a more realistic picture of the respective company - at least that is the wish of the rule-setters (so-called impairment-only).

However, this wish has not been fulfilled. For example, the NYBC is currently devaluing goodwill from "historical acquisitions" up to 2007.4

The London-based International Accounting Standards Board (IASB) has now presented a new regulation on goodwill.5 Anyone can comment on the exposure draft until 15 July.

The IASB defines the International Financial Reporting Standards (IFRS), which are primarily applied outside the USA and have their origins in the US Generally Accepted Accounting Principles (US GAAP). For a long time, the two were supposed to come together. However, the engagement has long since been broken and they are going their separate ways, even if there are still agreements on important issues. This is the case with goodwill, a problem child for both of them, to which their parents devote a great deal of attention.

Goodwill remains an asset in the balance sheet until the carrying amounts can no longer be maintained. To this end, companies must carry out an impairment test on goodwill as and when required. This is also obligatory once a year without cause.

An impairment loss is recognised, for example, if the estimated selling price of the business units on which the goodwill was recognised is no longer close to its carrying amount. Goodwill must also be amortised if the business outlook deteriorates to such an extent that original plans for expected sales and cash inflows have to be significantly reduced. Actually.

This is because an actual devaluation is the exception, even if the horizon has already darkened noticeably. CFOs and CEOs of acquisition-happy companies regularly avoid admitting that they have bought subsidiaries at too high a price. The accounting rules offer broad scope for this. This allows planning horizons to be extended. And the business units to which goodwill is allocated can be reorganised. These business units are often designed in such a way that no comparable market transaction can be found anyway - where there is no transaction, there is no price indication.

"The determination of the recoverable amount is subject to judgement and significant estimation uncertainties. Assumptions regarding the amount of net cash flows, long-term growth rates and discount factors are to be regarded as a significant source of estimation uncertainty due to their inherent uncertainty," says the German company Merck KGaA in its latest annual report on the impairment test.6

In any case, some companies in Europe even lack mandatory information. The information also differs.7

In its mandatory announcement to the stock exchange in 2019, the DAX-listed company Vonovia only made a footnote of a goodwill impairment of 1.9 billion euros.8 The headline stated that Vonovia was "continuing its good business performance". At the time, this was a matter of interpretation: the profit for the period plummeted by 90 per cent due to the goodwill impairment.

The problems with the allocation of goodwill to the business units and the chaotic information situation have now apparently also been recognised by the rule-makers in London. They admit that the impairment test for business units with goodwill is "complex, time-consuming and expensive" and that "sometimes" losses are "recognised too late". The acquired goodwill could be "masked".9

The IASB is now proposing extended disclosure requirements. For example, companies should make disclosures about the performance of business combinations. The main objectives of the company at the time of acquisition must be disclosed, as well as the associated objectives in the case of a "strategic business combination".

In future, companies should also limit the extent to which these main objectives and the associated targets are to be achieved in subsequent periods. Companies should provide "quantitative information" on expected synergies, divided into categories: Revenue synergies, cost synergies and any other type of synergies. Companies should also explain the "strategic rationale" behind a merger. Information on acquired pension liabilities and debt should be "enhanced". Assumptions on cash flows and discount rates should be "consistent" in future.

The proposed new disclosures would require an entity to disclose more direct information about the performance of business combinations so that users would no longer have to rely on the outcome of the impairment test, according to the IASB. The ideas put forward in the run-up to the proposal to require companies to recognise equity before goodwill or to abolish the annual impairment test were both rejected.

The regulations on goodwill are fundamental for a fundamental analysis of a balance sheet. This is because goodwill has risen to a central position. The brisk takeover activity of hundreds of thousands of companies has contributed to this, as has the almost notorious refusal of company managers to amortise goodwill at all.

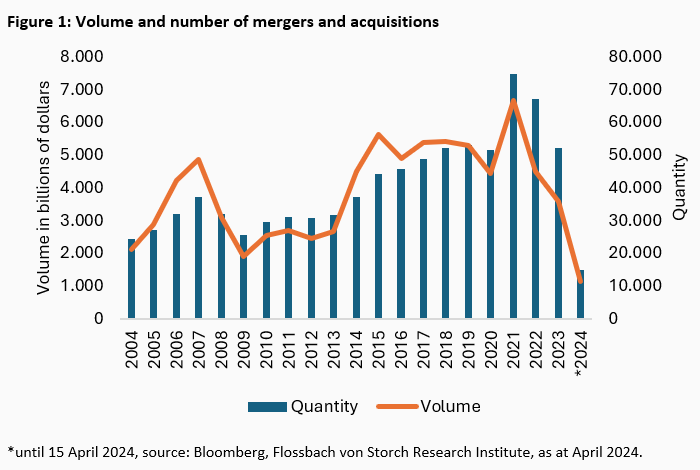

It can be assumed that the takeover-friendly balance sheet structure is a driver for the mergers & acquisitions (M&A) business.

The mergers and acquisitions business has been growing for 20 years with two interruptions: The financial crisis put the brakes on. Most recently, the level has been declining, presumably due to higher interest rates (figure 1).

Depending on the study, up to 90 per cent of all takeovers fail.10 Nevertheless, the cumulative volume of mergers and acquisitions over a good 20 years up to this April totalled 81 trillion dollars. According to data from Bloomberg, buyers paid an average takeover premium of 20.3 per cent on the last market value of the object of desire during this period. Market prices, as well as the most recent book values of the assets of the acquired subsidiaries, have nothing to do with goodwill and can at best be an indication (see footnote 2).

Goodwill is ultimately "only an asset by definition".11 And it is precisely "in bidding wars that a purchase price may ultimately be fixed that undoubtedly also contains overpayments".12

This is reflected. In the broad-based MSCI All Country World Index (MSCI ACWI), which comprises the most important shares in industrialised and emerging countries, goodwill accounted for a median of 6 per cent of equity, compared to just under 23 per cent in the Dax. Data on 2,338 companies was available for the global index. The average ratio of goodwill to equity was 28.1 per cent in the MSCI ACWI and 39.9 per cent in the 40 Dax companies.

The clear difference between the median and the average shows that the goodwill problem is concentrated on an elite group of companies whose business model is acquisition-driven (and where goodwill is not amortised). This is because goodwill only arises from takeovers. It is therefore also known as "derivative goodwill".

Goodwill generated in companies themselves (original goodwill) may not be capitalised - which is, of course, an accounting anomaly that is obvious to everyone. While synergy effects generated in companies that may have an impact in the future do not appear as an asset in the balance sheet, a buyer may recognise any premium, however high, on the acquired assets of a subsidiary as a supposed "hard" value.

Every fifth company in the MSCI ACWI has high goodwill of 50 per cent or more of equity; in the Dax, this even applies to four out of ten companies. On average, the ratio of goodwill to total assets for the 40 Dax companies is 14.3 per cent (MSCI ACWI: 9.7 per cent). Excluding financial groups, the average ratio of goodwill to non-current assets for Dax companies is 26.2 per cent (MSCI ACWI: 18.0 per cent).

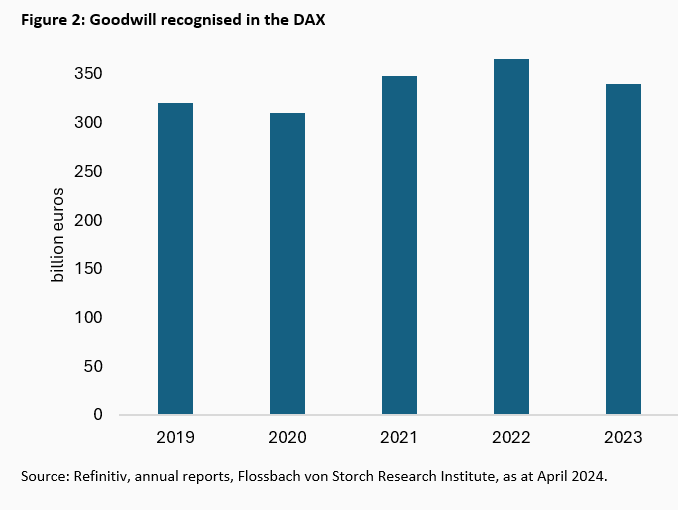

The Dax is therefore a proxy for a topic that has repeatedly taken the crown as the most discussed accounting issue for decades. Most recently, the goodwill recognised in the Dax in absolute terms was just under 341 billion euros (figure 2).

This is a good 25 billion euros less than in 2022, but this is hardly due to an increased, critical internal view of the companies on their acquisitions, which would be reflected in write-downs. Most of the decline can be explained by the deconsolidation of the Fresenius subsidiary Fresenius Medical Care, which alone reduced total goodwill in the DAX by 15.6 billion euros.

In the past financial year, the DAX companies wrote down goodwill by a good 7.2 billion euros or only around two per cent compared to the previous year. Added to this are currency effects as well as some acquisitions and disposals. Overall, a write-down of 6.7 billion euros by Bayer, primarily on the agricultural business, accounted for the lion's share.

If this devaluation and the previous year's goodwill of the Leverkusen-based company are deducted, the average devaluation is 0.15 per cent. In other words, this means that The DAX companies with goodwill on their balance sheets (apart from Bayer) expect to benefit from their acquired subsidiaries for another 667 years. However, whether there will be synergies from an acquisition made in 2005, 2010 or 2015 in 2690 is undoubtedly a rhetorical question.

The goodwill of the 2,338 companies in the MSCI ACWI for which data is available totals USD 7,886 billion with a market capitalisation of USD 64,900 billion. The DAX, with only 40 companies and a market capitalisation of just USD 1,980 billion, accounts for around five per cent of the goodwill reported by the 2,338 MSCI ACWI companies. This again shows the outstanding role of this balance sheet item for the leading German index.

How impairment-only has changed the balance sheets and thus the income statements can be clearly seen from the DAX companies: While in the years 2000 to 2004, before the new regulation, the annual depreciation averaged 8.5 per cent of the goodwill previously reported in the balance sheet (i.e. this would have disappeared after twelve years at the same rate of depreciation), in the 17 financial years thereafter it was only 1.4 per cent or one sixth of this.13 As a result, equity and the associated debt ratios, for example, as well as net profits are significantly lower on paper than before.

Not only in the DAX, but throughout Europe, companies are generally reluctant to amortise goodwill compared to the USA. This is shown by a study that analysed a total of more than 35,000 financial years.14 According to the study, US companies are more likely to amortise goodwill if there are economic indicators to do so. In addition, amortisation is regularly higher than in Europe. On the old continent, even the cumulative impairments "never reached the level of US companies", be it in one or more of the years observed.

In the Dax, significant, first-time write-downs on goodwill are a rarity. As a rule, the first significant write-down is followed by further write-downs in subsequent years, although not always immediately.

In the case of twelve drastic write-downs (or their announcement) of twelve different DAX companies over the past 20 years, the share prices in the year before the announcement of the write-down underperformed the benchmark index (DAX share price index in each case) by an average of 15.5 percentage points. After the write-downs, this underperformance decreased by a median of 2.7 percentage points.

A quarter of the shares outperformed the index before the devaluation, and two of these three shares also did so afterwards. Half of the shares outperformed the index after the devaluation, but only significantly in three cases.

An investor who had held all the respective shares one year before to one year after the announcement of the goodwill amortisation would have fared 5.5 percentage points worse than with the index itself. This is the result of a current analysis based on company information and the respective share prices.

The correlation does not necessarily have to be causal. Goodwill write-downs are usually also associated with other business difficulties.

The share price reactions to goodwill amortisation are "generally negative and significant", according to a study by the University of Kansas at Lawrence.15 According to the study, the immediate effects were in the order of minus 2.94 to minus 3.52 per cent of the share price. It was particularly noteworthy for investors that one year after the announcement, additional negative effects of minus 11.02 per cent had occurred. These results indicate that investors initially reacted below average to the announcement of goodwill amortisation and that they only became aware of the potential for further losses in the period following the announcement.

A study analysing goodwill impairment announcements by companies listed on Nordic stock markets and market reactions to them found "abnormal, negative price reactions".16 The empirical results indicated that goodwill impairments lead investors to lower their expectations, resulting in a negative share price performance following the impairment announcement.

A study of companies listed on the Chinese A-share market came to the conclusion that the avoidance of goodwill impairment is negatively associated with the future growth of a company and positively associated with the risk of a share price crash. These negative effects persisted for at least three years.17

Numerous studies have analysed the relationship between executive compensation and the associated policy on goodwill impairment. The result of such studies is regularly that the boardroom avoids devaluations in order not to jeopardise the bonus.18

Even during the financial crisis, when the share prices of DAX-listed companies more than halved on average, higher goodwill amortisation "largely failed to materialise, contrary to expectations". This is the bottom line of a study by the Chair of Accounting and Controlling at the TU Bergakademie Freiberg.19 After reviewing 640 balance sheets from 160 German listed companies, the conclusion was that larger write-downs on the shaky position of goodwill were almost only made when board members were replaced.

New managers apparently clean up their balance sheets quickly so that their predecessors' bad investments worth billions do not fall at their feet at some point. A new CFO then considers 39 per cent of the goodwill position to be no longer sustainable, while new CEOs also stand for a very high devaluation of 31 per cent on average, according to the findings of the University of Freiberg.

These results can also be confirmed anecdotally time and again: At Bayer, for example, just eight weeks after the premature resignation of predecessor Werner Baumann, the new CEO William Anderson announced a multi-billion dollar goodwill write-down "with regard to the glyphosate business".20 During his time in office, Baumann was responsible for the 63 billion dollar takeover of glyphosate manufacturer Monsanto, which immediately increased Bayer's goodwill position from just under 15 to more than 38 billion euros.

Such takeover manoeuvres change the balance sheet considerably. At Bayer, the ratio of net financial debt to equity rose from 9.8 per cent to 86.7 per cent within a year in the course of the takeover. Most recently, in the 2023 financial year, the high goodwill amortisation reduced equity. This drove the debt ratio to 104.3 per cent.

The ratio is usually part of the assessment of a company's creditworthiness and therefore its refinancing costs. If further goodwill amortisation cannot be absorbed by profits from operating activities, such a ratio deteriorates. Debt financing then becomes more complicated and more expensive. If the equity capital disappears, capital increases such as those at New York Community Bancorp are on the cards.

Such a development is not inevitable and does not constitute a recommendation for action for a share in isolation. This is because investors may have already anticipated such negative developments in individual cases.

The rule-makers have long been aware that the impairment-only approach for goodwill does not work in practice but sets false incentives and sends false signals. The planned extended mandatory disclosures will cure the symptoms, but not the disease.

It would be logical not to recognise acquired goodwill in the balance sheet in the first place, as is also the case for the original goodwill generated within the company. Direct offsetting via equity after a merger or takeover would show shareholders the true extent of the capital investment.

If a takeover pays off, as is repeatedly loudly proclaimed when transactions are concluded, then the equity paid out directly for the purchase of an acquisition builds up again over time via retained earnings. The cash inflows, which are very important for share valuation, would not be affected by such a regulation anyway.

This could regularly prevent reckless takeovers or lead to more price discipline. This would be bad for the shareholders of the takeover target and for the investment bankers and consultants involved in the transaction. Owners of acquirers, on the other hand, would have a much greater chance of being rewarded with real added value instead of just the air position of goodwill. The visibility of the success and failure of takeovers would be directly increased.

An alternative would be to allow the capitalisation of original goodwill. This in turn would lead to even more internal, difficult-to-understand valuations of asset items based on management estimates and further encourage balance sheet embellishments.

2 This is not about the difference between market capitalisation and book value, for example in the case of a takeover of a listed company. Rather, goodwill is the difference between the purchase price and the revalued assets less liabilities of the acquired subsidiary.

3 The rule of regular amortisation of goodwill was abolished under US GAAP in 2001. Under the international IFRS rules, which apply primarily to European companies, regular amortisation no longer applies for financial years beginning in April 2004.

4https://d18rn0p25nwr6d.cloudfront.net/CIK-0000910073/f96951bf-e346-4fd6-ac44-e2c05a7b481f.pdf

7 Wladislav Gawenko, Goodwill reporting in Europe: an empirical analysis with regard to quantitative and qualitative disclosures, KoR : internationale und kapitalmarktorientierte Rechnungslegung, issue 3/2021, pages 107-114

9 Page 5ff Exposure Draft

10https://hbr.org/2016/06/ma-the-one-thing-you-need-to-get-right

http://knowledge.wharton.upenn.edu/article/why-do-so-many-mergers-fail/

https://www.govcon.com/doc/kpmg-identifies-six-key-factors-for-successfu-0001

11 see page 1283: https://www.rechnungslegungsseminare.de/images/DB%2024-2021%20Wirth_K%C3%BCting_Dusemond.pdf

12 op. cit.

15https://www.tandfonline.com/doi/abs/10.2469/faj.v59.n6.2577

16https://gupea.ub.gu.se/bitstream/handle/2077/61397/gupea_2077_61397_1.pdf?sequence=1&isAllowed=y

17https://www.econstor.eu/bitstream/10419/241820/1/1738064417.pdf

18https://dash.harvard.edu/bitstream/handle/1/11320612/ramana,watts_evidence-on-the-use_SSRN-id1134943.pdf;jsessionid=1F845AA062B58570444DA48851CEFF56?sequence=1, https://onlinelibrary.wiley.com/doi/10.1111/j.1475-679X.2006.00200.x,

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3092658

19 Silvia Rogler, Sandro Veit Straub, Martin Tettenborn, KoR: internationale und kapitalmarktorientierte Rechnungslegung, issue 07 of 2 July 2012, pages 343-351

20https://www.bayer.com/media/bayer-senkt-ausblick-fuer-das-geschaeftsjahr/

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.

Christof Schürmann

Senior Research Analyst

At the Institute since 2022. The graduate in business administration (FH), previously worked as a journalist and deputy head of "Money" at WirtschaftsWoche. The trained banker and book author ("Die Bilanztrickser") taught balance sheet research part-time at the private university BiTS in Iserlohn.

All articles by Christof Schürmann