05.07.2023 - Studies

The calm in the financial sector is deceptive. New dangers from the banks are lurking beneath the surface.

Credit Suisse was quickly presented as a special case after its de facto bankruptcy this March. Regulators around the globe immediately sought to portray the case of the major Swiss bank as a solitary event within a robust banking landscape; a case that should not be generalised.

But a closer look reveals that there are parallels with other banks. The danger to the markets posed by the banks has not been lifted, but possibly only postponed.

A loss of customer confidence affected not only the major Swiss bank, but also three important US regional banks, each of which also had to be wound up.

It would therefore be naïve to believe that the problems at Credit Suisse and in the USA, which in addition to poor management also - or even primarily - have to do with the rapid rise in interest rates over the past 18 months, could not affect other banks.

Certainly, it is hardly feasible to uncover all the details in a sector that - measured by 20 countries worldwide with a relevant banking system - is worth more than 170 trillion dollars. But shining the spotlight on major problem areas is possible.

The main problem is the billions of dollars in investments on the balance sheets. Investments that, due to the rise in interest rates, no longer come close to matching the market values that have fallen in the opposite direction. This applies to the US banking sector as well as to its European counterpart. A special, additional problem on the old continent is the close link between the banking sector and the partly highly indebted states.

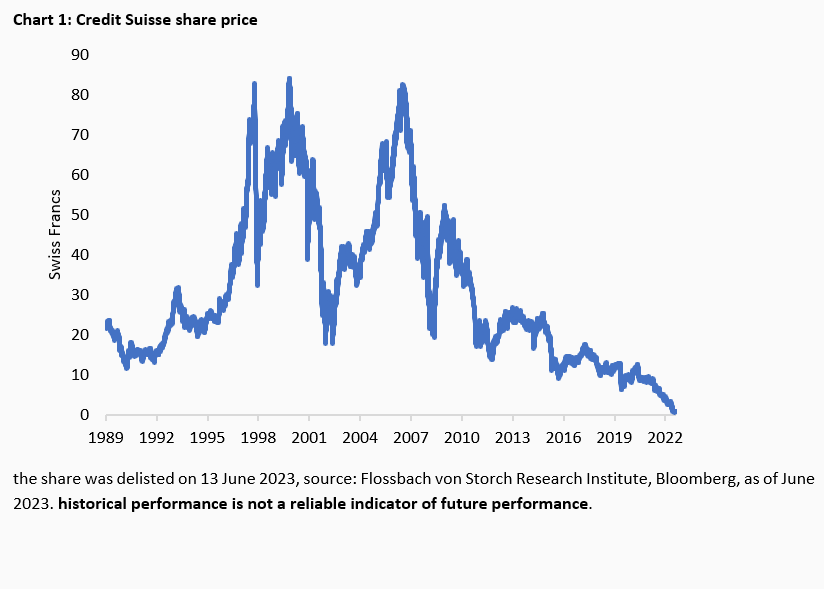

Anyone who is active in the markets cannot avoid keeping an eye on these risks, at least with one eye - and observing a few principles. Because if the banking system, the foundation of the global markets, cracks, then the upper floors will also start to slide. The 99 percent price loss suffered by those shareholders who once bought Credit Suisse shares at their highest prices shows the dimension (chart 1).

As a general rule, supervisory authorities and regulatory quotas cannot be relied upon. Just a few days before its rescue and forced marriage to its competitor UBS, the Swiss National Bank (SNB) and the financial market regulator Finma gave Credit Suisse a good report card: Credit Suisse met the capital and liquidity requirements placed on systemically important banks.

In fact, Credit Suisse last showed a regulatory Tier 1 capital ratio of 20.3 percent as of the end of March 2023 - well above the usual average. By comparison, the 122 most important banks in the EU showed an average Tier 1 ratio of 15.3 percent, according to the latest available data. At the 23 major US banks that the Federal Reserve just subjected to its annual stress test, the ratio is currently only 12.4 percent.

But confidence in the Credit Suisse balance sheet was long gone by then. Rightly so.

This is because the auditors of PwC already expressed a "contrary opinion on the effectiveness of the internal control systems" that the Swiss banking group had presented to the public within its financial reporting in the annual report 2022. As a central problem, PwC named the assessment of balance sheet valuations of asset and debt positions worth billions, which were in part only made according to estimates.

Overall, PwC stated in the audit opinion on the financial statements "that management has not developed and maintained an effective risk assessment process to identify and analyse the risk of material misstatement in its consolidated financial statements".1

Even the SNB had to admit meekly only in the second half of June this year that it could not yet assess how robust the newly merged bank UBS would be. "The data currently available are not sufficient to comprehensively assess the resilience of the merged bank in the context of such a forward-looking analysis," reads an SNB report.2 The good report card issued to Credit Suisse in March 2023 was thus probably wrong.

Consequently, it can be said that the much-vaunted, much-praised capital ratios of the banks, which are always prominently displayed in the shop window, are, at least in individual cases, much less meaningful and signify resilience than is generally assumed.

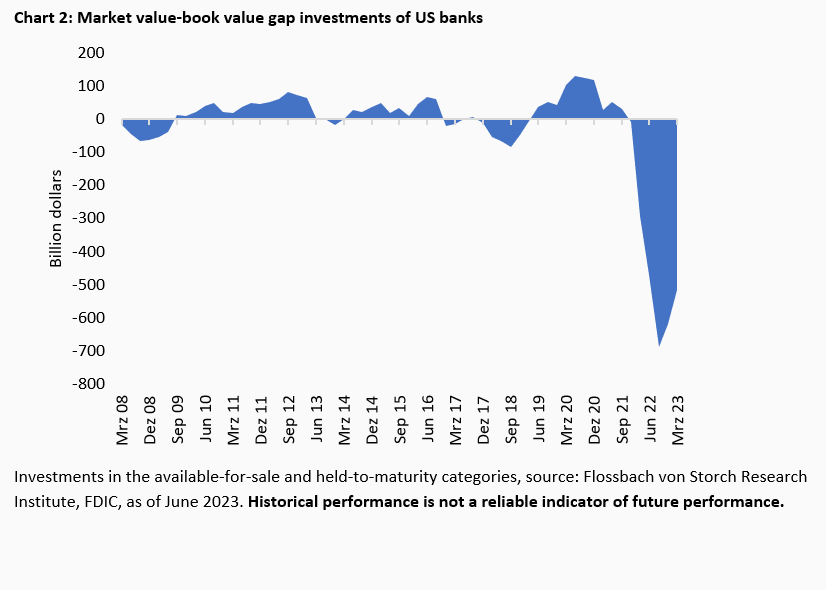

The second principle is that valuations of assets on balance sheets differ from market values. This is impressively shown by the latest investigation of the US deposit insurance company Federal Deposit Insurance Corporation (FDIC).

In order to identify possible instabilities, the FDIC just collected important data on the US financial sector. The main focus was on the gap between the values reported on the balance sheet and the actual market prices.

This is because, among others, the Californian Silicon Valley Bank (SVB) went under this year. At the end of September 2022, this gap at the US regional bank was around 18 billion dollars. Since clients had started withdrawing funds from their once good 180 billion dollars deposits since the second quarter of 2022, SVB ultimately had to realise book losses on the market to create liquidity - eroding its capital in the process.

Although there is now a slight all-clear for the US banking sector as a whole - but only from a record low. According to the FDIC, the book losses of the affected assets at the 4,672 US banks it covers in the first quarter of 2023 have now fallen by a good quarter from the low to 515.6 billion dollars.

At its peak, in the third quarter of 2022, the difference was still 689.9 billion dollars.3 Most recently, US banks reported a total of over 5.6 trillion dollars in such investments. The most recent book losses thus amounted to 9.2 percent of this.

By way of comparison: during the financial crisis, this market value-book value gap amounted to a maximum of a good 65 billion dollars in absolute terms (chart 2).

All US banks combined last reported Tier 1 capital of a good 2.1 trillion dollars, which financed a business volume of 23.7 trillion dollars. This means a leverage of a good eleven times the hard-core capital Tier 1 (equity plus reserves). At Credit Suisse, this leverage was 10.6 for the group at the end of 2022 - which should theoretically mean a somewhat lower risk.

But obviously not much can go wrong with such leverage, as has already been shown this year. If other (US) banks had to realise book value losses on the market, as SVB has already done, this would probably have the same effects: A lack of equity that could lead to bankruptcy and nervous market reactions.

It is true that the Tier 1 capital requirements are basically a ratio of only 4.5 percent of the so-called risk-weighted assets. But in practice, further capital buffers are required, especially for systemically important banks, so that the ratio requirements can easily be above the ten percent mark.

Markets and clients regularly react before the limit, which varies from bank to bank, is undershot, as recent experience such as the case of Credit Suisse also shows.

Whether Jerome Powell has this danger in mind? It is quite possible. On 22 June, the head of the Federal Reserve said that the capital requirements for large banks could be increased by 20 percent - which immediately led to a noticeable drop in the prices of US bank shares on the stock market.

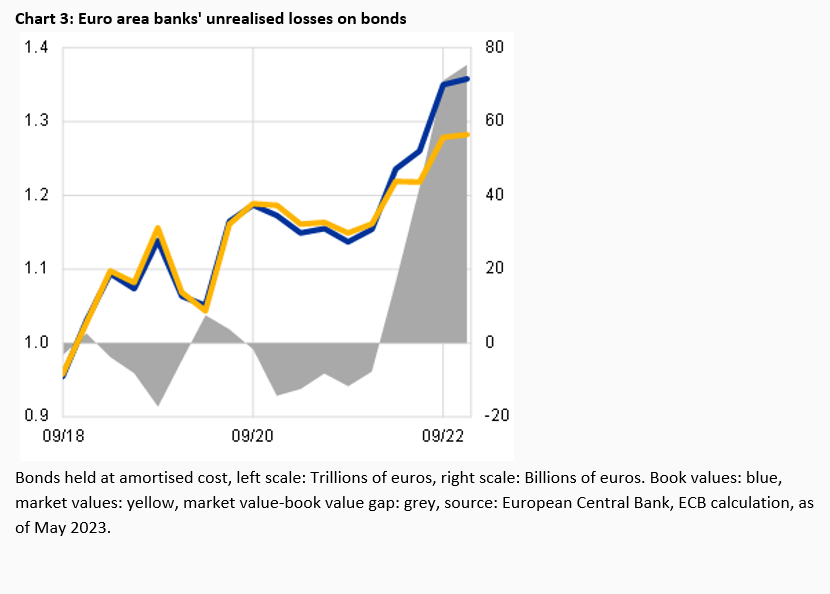

Meanwhile, in the Eurozone, the sun is shining brightly - at least if one uncritically follows the comments of the central bankers of the European Central Bank (ECB). The 111 major eurozone banks supervised by the ECB are sitting on "relatively modest unrealised losses related to sharp increases in interest rates", said Andrea Enria, the ECB's top supervisor, in mid-June.

For all banks under ECB supervision, "the total amount of unrealised losses is quite limited", Enria said. These losses were "in the range of 70 billion" euros (chart 3).

However, the sum of a good 70 billion euros, or about five percent difference to the book value, only includes a piece from possible losses of all investments. Because the ECB is looking at a small section of the balance sheet here, where book losses cannot be overlooked. But where else could they threaten? So, the basic principle is: If in doubt, take a closer look.

According to data from the European Banking Authority (EBA), the 122 banks it supervises in the European Union (EU), which are largely congruent with the 111 institutions supervised by the ECB, held just under 16.7 trillion euros in investments that are intended to remain on the books until maturity (investments at amortised cost). In addition, there is a good 1.1 trillion euros in investments that tend to be available for sale (investments at fair value through other comprehensive income).

The EBA estimates a total of 9.5 trillion euros as the banks' risk exposure. If there is also an average deviation of five percent from the prices to be realised, this would result in a hidden burden of 475 billion euros.

That would be about 28 percent of the equity capital of the 122 banks totalling 1.7 trillion euros. A sum that in turn amounts to almost 6.1 percent of the business volume - a leverage of 16.5 times the equity capital. Triple-digit billion losses on the investments of the 122 banks would be conceivable in a crisis scenario. 100 billion euros would amount to just 0.36 percent loss on all investments, or 1.05 percent on the investments that the EBA classifies as risk exposure.

The obvious one are losses from assets for which the credit risk has increased significantly, but which had not yet been impaired by banks. According to the EBA, according to the latest available data, this involved assets worth more than 1.4 trillion euros. And loans of more than 357 billion euros were already impaired or at risk of default (so-called non-performing loans).

In contrast, the agreed services for the vast majority of government bonds are running undisturbed. In the case of eurozone bonds, the holders benefit from the fact that the ECB continues to succeed in keeping both the prices for government bonds in general and, above all, the spread between weaker eurozone government bonds and German government bonds under control.

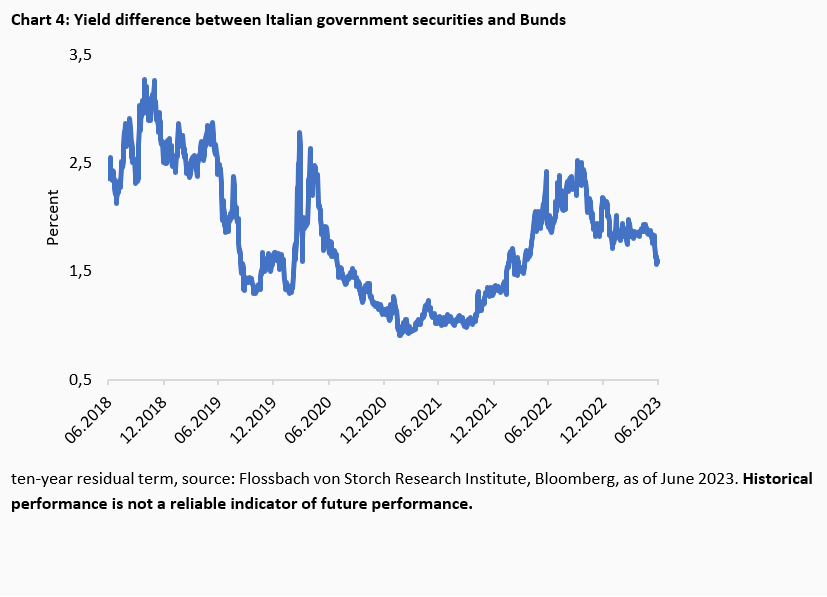

Highly indebted Italy is in first place here. Recently, the spread between the yields of Italian government bonds and German Bunds even declined significantly (chart 4).

But higher book or even real losses may only be postponed. It is true that the ECB has established systems in its emergency box to prevent a sovereign-bank doom loop.4 Only a year ago it added another line of defence with the Transmission Protection Instrument (TPI), which allows it to buy government bonds under only minor restrictions. Of course, TPI applies to the paper of all euro countries, but we are referring to Italy.

But whether the ECB will be able to tame market forces for all time is, of course, a question that will remain unanswered until it actually comes to an acid test, i.e., if large investors should speculate against a large euro country like Italy, as in the EMS crisis at the beginning of the 1990s.5

Then the problematic, because very close, link between government debt and bank balance sheets would come into play. A potentially fatal link that cannot be broken in the foreseeable future.

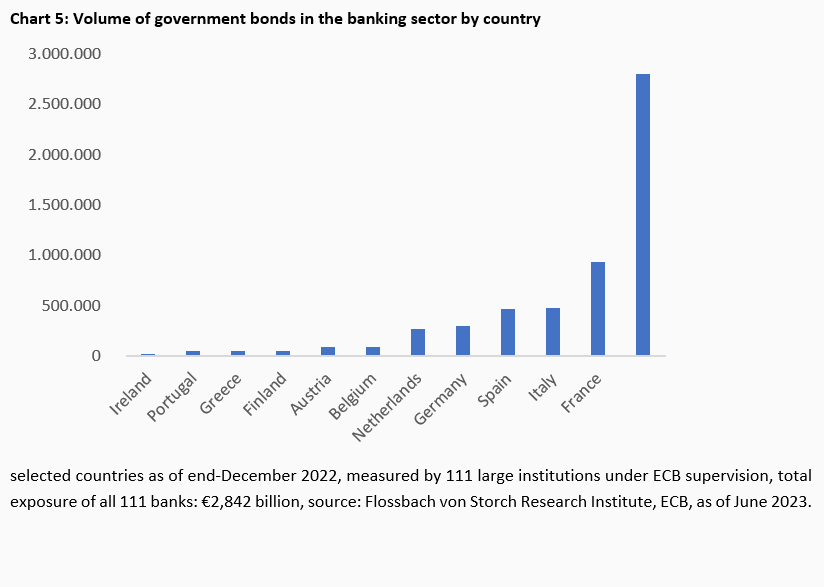

The 111 largest banks in the Eurozone alone, which manage 80 percent of the investments of all financial institutions in the monetary community, hold more than 2.8 trillion euros in government securities, of which French banks alone hold one third (chart 5).

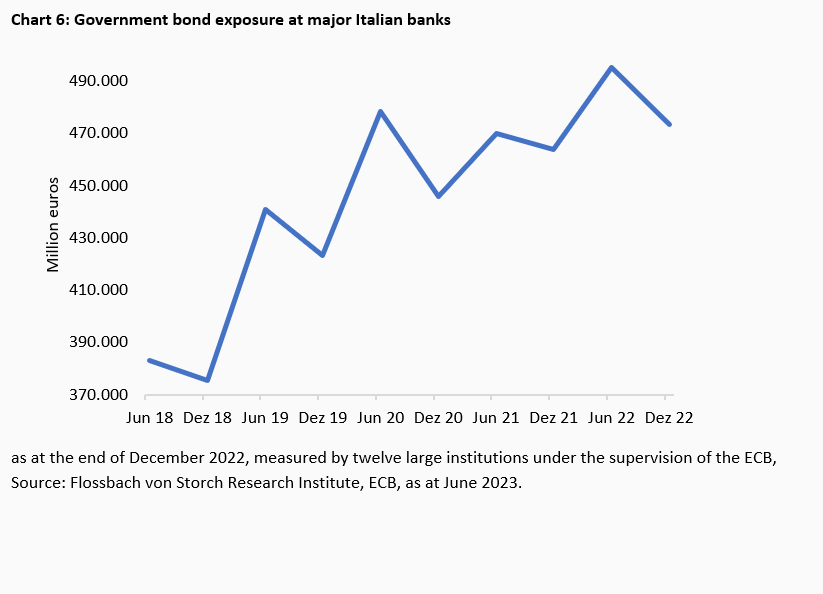

In the case of the major Italian banks, the portfolio has increased by a good quarter within four years since the end of 2018 alone (chart 6). This portfolio now amounts to 17.7 percent of the cumulative balance sheet total of the twelve banks.

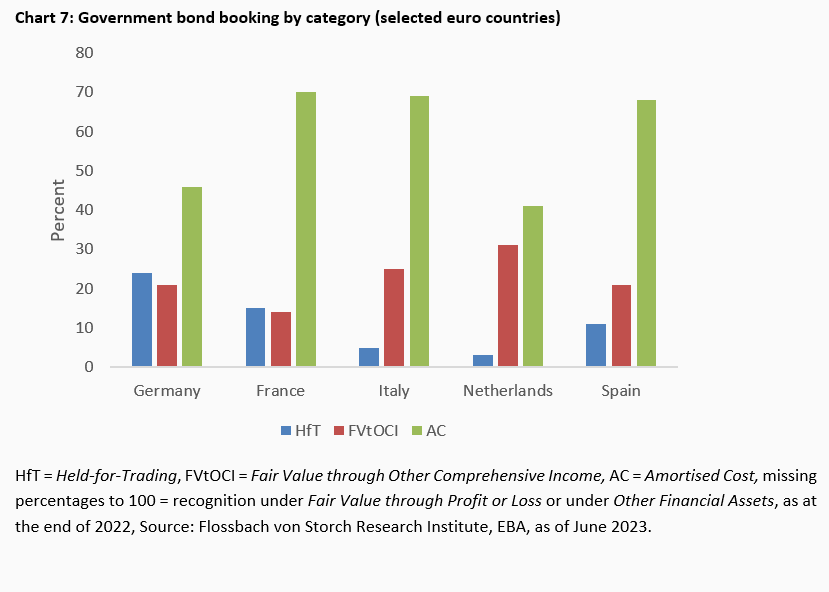

55 percent of the securities held by Italian banks had a residual maturity of five years or less - exactly the same as the average for all EU banks supervised by the EBA; for their French counterparts, the figure was 54 percent.

According to the EBA, French banks accounted for 84 percent of the bonds they held away from market prices. For Italian banks, the ratio was most recently 94 percent, divided into the categories amortised cost (for investments held to maturity) and fair value through other comprehensive income (for investments held for sale). In relative terms, German banks hold the most government securities accounted for at market prices (held-for-trading) (chart 7).

It would undoubtedly be problematic for all banks if they had to sell papers that are not intended for trading or short-term sale at market prices. Substantial losses would be the result.

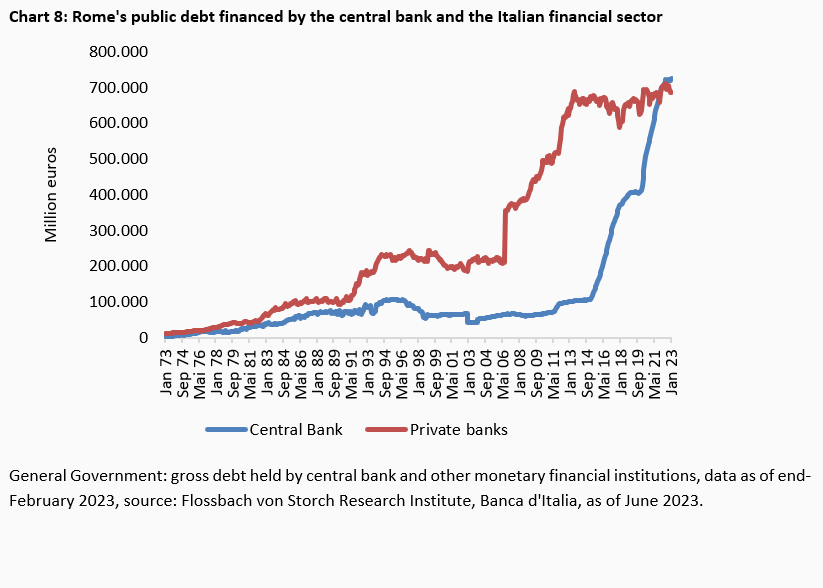

Viewed under a magnifying glass, since the financial crisis, the state budget in Rome in particular has become increasingly tied to the banks. The Italian financial sector as a whole (which also includes money market funds, for example) now finances its "own" state with almost 687 billion euros. Compared to before the financial crisis, this is more than three times the amount and corresponds to 198 percent of the capital of all banks on the balance sheet at the end of April.

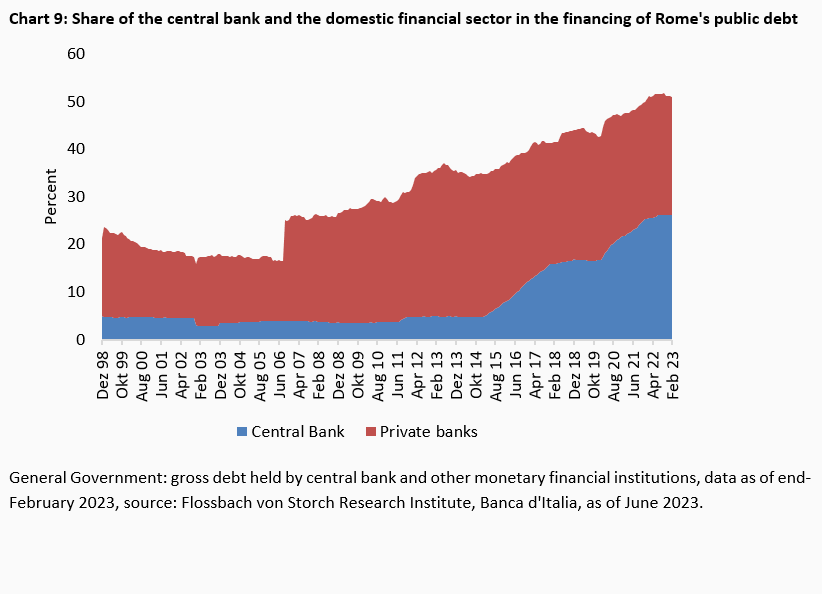

Since 2015, the ECB's bond-buying programme for euro states, which was adopted at the time, has also had an effect. In the meantime, the amount of Italy's government debt held by the central bank is even higher than that of the financial sector (chart 8).

As a result, more than half of Rome's 2.8 trillion euros debt is now on the books of the domestic financial sector and the ECB or the Banca d`Italia (chart 9).

While a central bank with negative equity capital would still be able to do business, this does not apply to private banks.

If, in a crisis situation, market prices for government bonds deteriorate and there is a simultaneous withdrawal of deposits by customers, then forced sales would burden the banks' capital and, in cases of high holdings, wipe them out - see Italy.

At the same time, the second most important pillar for the refinancing of debt for the Italian state, besides the ECB, would cease to exist. The same applies, albeit to a more limited extent, to other euro countries.

All in all, the outlook for financial stability remains fragile. In the US, banks are still sitting on huge book losses, and transactions may be too highly leveraged despite all regulation. A trigger for a new crisis would be, for example, the withdrawal of customer funds parked in accounts.

This also applies to European banks, where the mountain of sovereign debt on their books is a particular danger, as their market prices have fallen significantly.

France's financial sector and Italian banks are particularly at risk. A debt crisis in Rome is likely to trigger domino effects.

1 Annual Report 2022 Credit Suisse Group AG, p. 258-III

2https://www.snb.ch/n/mmr/reference/stabrep_2023/source/stabrep_2023.n.pdf

3 The book losses are divided into the two categories available-for-sale (231.6 billion dollars) and held-to-maturity (284 billion dollars). Available-for-sale losses (or gains) are not recognised in profit or loss, but in equity (via the so-called statement of comprehensive income). Held-to-maturity, on the other hand, only becomes material when sold or transferred to another category.

4 see also: https://www.flossbachvonstorch-researchinstitute.com/de/studien/die-known-unknowns-der-finanzrisiken/

5 in September 1992, the British pound sterling and the Italian lira had to leave the EMS exchange rate mechanism

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.

Christof Schürmann

Senior Research Analyst

At the Institute since 2022. The graduate in business administration (FH), previously worked as a journalist and deputy head of "Money" at WirtschaftsWoche. The trained banker and book author ("Die Bilanztrickser") taught balance sheet research part-time at the private university BiTS in Iserlohn.

All articles by Christof Schürmann