08.04.2022 - Studies

At least in the German speaking world, the Saxon chief miner Hans Carl von Carlowitz is considered the founder of the term "sustainability". Carlowitz was concerned with forestry. In 1713, he gave King Friedrich of Saxony "out of love for the promotion of the general best" a fundamental work entitled Sylvicultura oeconomica, an "Instruction on Wild Tree Breeding" for overcoming the "Great Wood Shortage". There he coined the term “sustainable use”.1

We turned "sustainable use" into "sustainability", and on the one hand applied the term ever more broadly and on the other hand defined it in ever more detail.

A milestone in this process was the Brundtland Report presented by the United Nations in 1987, which defined sustainability in this way:

"Sustainable development is development that meets the needs of the present without compromising the ability of future generations to meet their own needs. "

Although this was entirely in Carlowitz's spirit, it already went far beyond his concern for forestry. Ecological, economic and social aspects of a general "sustainable development" came into focus. The authors of the Brundtland Report recognised that "[t]he satisfaction of human needs and aspirations is the primary goal of development." But over time, the holistic aspiration was fanned out into ecological, economic and social aspects of sustainability, as if these were three different dimensions of the term.

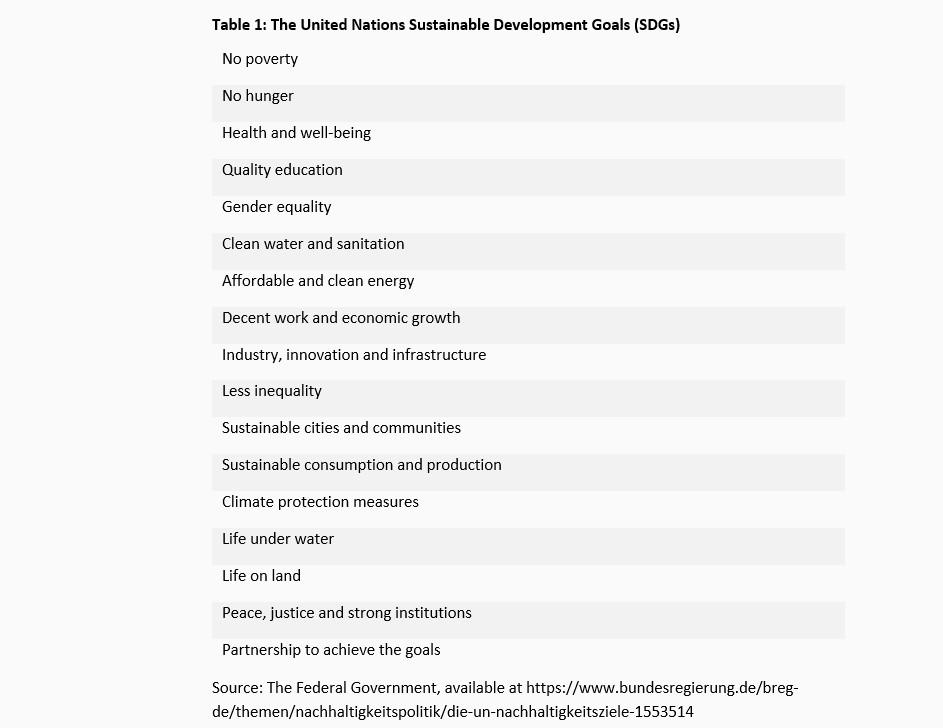

The Brundtland Report was then followed in 2015 by an "Agenda 2030" of the United Nations, in which no less than 17 Sustainable Development Goals are to be achieved by 2030 (Table 1).

It seems that the United Nations has set itself the goal of realising paradise on earth by 2030, despite the fact that the Brundtland Report already spoke of the "constraints imposed by the state of technology and social organisation on the ability of the environment to meet present and future needs".

The list of the 17 Sustainable Development Goals hides any conflicts among goals, but such conflicts are inherent in the world of scarcity. Equality supposedly leads to justice, although people are inherently unequal. Climate protection and economic growth supposedly go hand in hand, although climate protection incurs costs. And all nations are supposedly peacefully united in the fight against poverty and hunger, although wars are a permanent phenomenon and mainly responsible for poverty and hunger.

Nevertheless, with the German Sustainability Strategy in 2017, the Federal Government committed to an extremely detailed plan on how to implement these global sustainability goals.2 The latest Annual Economic Report of 22 January 2022 states:

"Last but not least, a further development towards a social-ecological market economy implies that the relevant financial and economic policy instruments are scrutinised with regard to their coherence with sustainability goals and, in case of doubt, adapted. "3

With its lexicographical listing of partly competing goals, the United Nations sustainability canon has above all created a quarry for organised interest groups, which from there break out easily usable goals for purpose-driven political lobbying. The most popular goal in the recent past has been climate protection, which has nurtured the most numerous and most powerful interest groups and left a deep mark in the direction of German and European economic policy.

In the paradise world of sustainability, there should be "a continuous steady and lasting use" in all economic sectors - and not only in the timber industry targeted by Carlowitz. Of course, this also includes the financial sector.

In 2004, a group of private and public financial organisations published a report entitled Who Cares Wins, prepared at the invitation of UN Secretary-General Kofi Annan.4 The aim of the report was to develop guidelines and recommendations on how environmental, social and corporate governance aspects could be better taken into account in asset management, securities trading and financial research. The report states (on page 3):

"A better inclusion of environmental, social and corporate governance (ESG) factors in investment decisions will ultimately contribute to more stable and predictable markets, which is in the interest of all market actors."

And Josef Ackermann, then Chairman of the Group Executive Committee of Deutsche Bank, was quoted in the same document with the following words:

"Creating long-term value for our shareholders while concurrently ensuring the enduring viability of our human and natural resources is an important part of our business philosophy".

The aim was to create "sustainable" financial markets by intensifying the focus on investments in "sustainable" assets. These were to contribute to a dynamic economy, the prerequisite for which was a vibrant civil society that ultimately depended on a sustainable planet Earth. The aim of the initiative was to better understand the environmental impact of economic activities, social concerns and corporate governance in investment, and to encourage issuers to better report in these fields.

No common-sense financial analyst or business leader could have objected to the proposition that an institution or company that is poorly managed, anti-social and systematically damaging to the environment would not be an attractive investment in the long term and would therefore not enjoy a lasting raison d'être in the market. Seen in this light, the call to take "ESG criteria" into account when investing seemed like a demand to invest with common sense - and not according to the parameters of modern finance theory consisting of market returns and price volatility.

However, common sense is often an all too scarce commodity. While the sustainability concept of the Brundtland Report evolved into the utopia of the UN Sustainable Development Goals, the "ESG criteria" of the Annan Report narrowed down to partial aspects that produced a mechanical rating system and government bureaucratic monsters.

Rating agencies have developed various "ESG ratings" that are supposed to measure the environmental friendliness, social compatibility and proper business management of economic enterprises according to bureaucratically prescribed criteria. In doing so, however, the agencies go far beyond what can be measured quantitatively. Ratings came into being to measure the probability of default on loans. Although qualitative factors also play a role here, a quantitative statement can be made on the basis of key figures from profit and loss account and balance sheet analysis.

In contrast, the concept of sustainability is very complex and involves conflicting goals. It cannot be defined without contradiction with the 17 Sustainability Goals, nor can it be broken down to the three factors "E", "S" and "G". It is impossible to implement the sustainability goals free of contradictions or to convert the ESG criteria into a measure for a "rating". Subjective and selective assessments dominate. Consequently, it is not surprising that the ESG ratings produced by the agencies are often inconsistent with each other.5

In the capital markets, investment fund providers have promised their clients higher returns from "sustainable" ("ESG") investments. They may have been influenced by the assessments of the Annan Report. In fact, ESG investments have at times indeed experienced larger price increases than the overall equity market. However, this was due to politically stimulated cash inflows, and not due to higher earnings prospects for these ventures that would justify higher returns.

In the long run, common sense tells us that investments selected according to ESG criteria must yield a lower return than the market as a whole. After all, if the investment universe is narrowed down to ESG-compliant stocks and investment funds are thus concentrated on a limited selection of stocks, lower returns are to be expected. In fact, the promises made by the providers have not been fulfilled either.6

They now have to face uncomfortable questions: Why have many Russian companies received similar ESG ratings as comparable European companies?7 How was it possible that some 300 ESG funds were exposed to Russia and their investors now face losses of more than 8 billion US dollars?8 Aswath Damodaran, Professor of Finance at the Stern School of Business at New York University has a harsh answer:

"I believe that ESG is, at its core, a feel-good scam that is enriching consultants, measurement services and fund managers, while doing close to nothing for the businesses and investors it claims to help, and even less for society."9

As a matter of fact, if investment funds on the public capital markets or bank loans are diverted from "brown" to "green" companies based on prescriptions of economic policy, profitable investment opportunities in "brown companies" open up for private equity investors. The cost of capital of these companies increases only slightly and their production continues as usual.

On the public side, the focus was on climate protection, which is mainly pursued by reducing carbon dioxide emissions. In March 2020, the European Union published a "taxonomy" that breaks down the climate and environmental impact of economic sectors in a catalogue of around 600 pages.10 On this basis, not only financial service providers are to inform their customers about investments, but also banks are to assess their credit risks associated with climate change. The US Securities and Exchange Commission recently took the same line with a 500-page report entitled "The Enhancement and Standardization of Climate-Related Disclosures for Investors".11 And the ECB also wants to make its monetary policy greener and thus more sustainable, although this entails risks for the safeguarding of price stability enshrined in its mandate.12

On the one hand, these extensive regulations are intended to provide more information that investors can include in their investment decisions. On the other hand, they also have the effect that the analysis of investments is reduced to officially propagated formulas. Thus, resources are not used where they can be used most efficiently and add the highest value to society, but where they are directed to by rules and regulations. It is not difficult to see that this not only reduces the quality of investment decisions, but also the overall economic productivity of capital, which then leads to less "sustainability" instead of more.

After the invasion of Ukraine by Russian troops on 24 February, Chancellor Olaf Scholz spoke of a turning point in the Bundestag on 27 February. The Bundestag applauded frenetically, as if celebrating the awakening from a dream world. But not only the dream world of German foreign and security policy but also the dream world of creating "sustainability" burst. On the hard ground of reality, there are conflicting goals in the pursuit of "sustainability" that have to be reconciled by choosing "trade-offs".

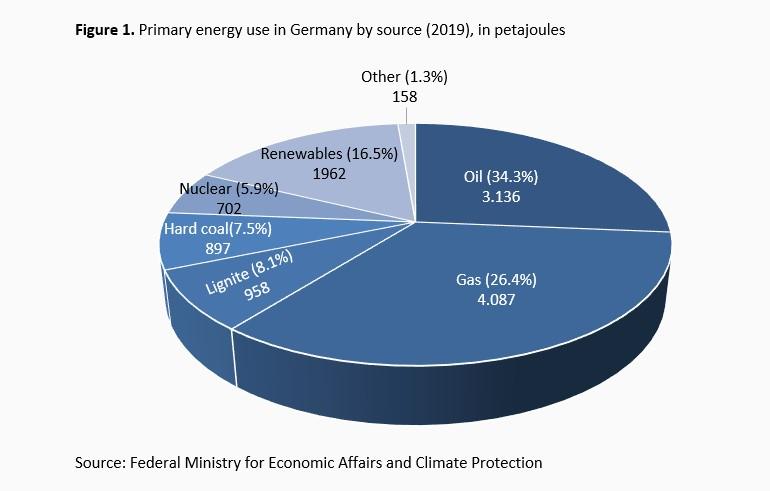

The Ukraine war made it particularly clear how the one-dimensional pursuit of climate protection by reducing carbon dioxide emissions and the ban on nuclear power created a cluster risk for energy supply. Germany's nuclear phase-out by 2022, adopted in 2011, and the phase-out of coal-fired power generation by 2034 for hard coal and by 2038 for lignite, adopted in 2020, have made Germany dependent on oil and gas imports from Russia. Until recently, oil and gas accounted for about 61 % of energy consumption in Germany (Figure 1). Of this, 55 % of the gas and 42 % of the oil was purchased from Russia. In addition, about 50 % of the coal used in Germany was imported from Russia.

As recently as the beginning of 2022, the Federal Ministry of Economics and Climate Protection planned in its Annual Economic Report to complete the phase-out of nuclear power this year and to accelerate the phase-out of coal energy:

"The coal phase-out in Germany will ideally be completed by 2030. The examination provided for in the Coal Phase-out Act as to whether the dates for the decommissioning of power plants, envisaged from 2030 onwards can be brought forward, should be anticipated from 2026 to 2022. The last nuclear power plants in Germany will be decommissioned at the end of 2022."

This deliberately increased Germany's energy dependence on Russian energy imports.

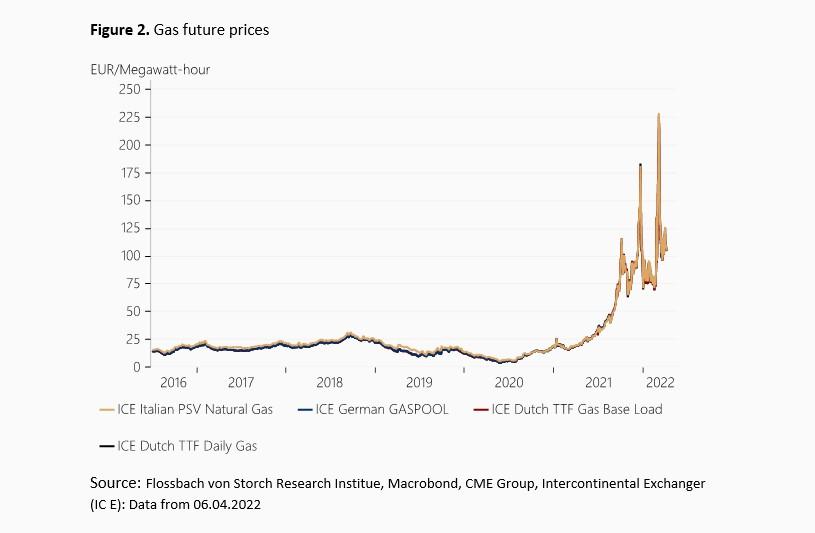

The climate goals were to be achieved, whatever the cost, without taking energy security and economic consequences into account.13 The Nordstream 2 gas pipeline grew to become the central pillar of the German energy transition. According to the coalition agreement of December 2021, fifty new gas-fired power plants were to be built that would be dependent on Russian gas. Due to the Ukraine war and the associated price increase for gas, this strategy failed spectacularly (Figure 2).

Ultimately, "sustainable" in the field of economics and finance means "profitable in the long term". Of course, this is only possible if the basis for life is preserved and socially acceptable efficient structures are used. However, it is not possible to create templates for this or to set timetables for achieving the goals.

The protection of our livelihoods ("environmental factors") includes not only the protection of the climate, but also the protection of the free social order. This also requires weapons, which are typically rated as not "ESG-compliant". And climate protection is not sustainable if the protective measures fuel social conflicts, lead to inefficient administrative structures, and regulations prevent innovations in politically defined "brown" companies, as is to be feared from the "Green Deal" and the "taxonomy" of the European Union.

“Social factors” must be seen in a social context. As harsh as it sounds, under certain circumstances child labour helps families to survive. Is it socially acceptable to boycott products made with child labour because of a supply chain law that does not take the circumstances into account?

Good governance and efficient administration ("corporate governance factors") are important. Consequently, environmental protection must not lead to the promotion of bad corporate governance and inefficient administrations. If there are conflicting goals, trade-offs between them must be found. However, ideological narrowness of vision and militant zeal directed only at partial aspects of sustainability do not allow for trade-offs.

Acting sustainably means following common sense, which is characterised by pragmatism and the ability to resolve conflicting goals by choosing trade-offs. In the long run – and therefore seen through the lens of sustainability – there is also no opposition between "shareholders" and "stakeholders". Because returns above costs, i.e. profits, are the prerequisite for any meaningful economic action for the benefit of all – society and the environment included.

1 Hans Carl von Carlowitz (1793). Sylvicultura oeconomica. Edited by Joachim Hamberger, oekom Verlag (Munich) 2013,

2 With Germanic obsession with detailed regulation, the 17 goals of the UN were increased to 63 for application in Germany. Progress towards the goals is to be monitored every two years using an indicator catalogue of the Federal Statistical Office specially constructed for this purpose. See also: https://www.destatis.de/DE/Themen/Gesellschaft-Umwelt/Nachhaltigkeitsindikatoren/_inhalt.html?__blob=publicationFile.

3 "Annual Economic Report: For a Social-Economic Market Economy - Shaping Transformation Innovatively", Federal Ministry of Economics and Climate Protection, p. 15.

6https://www.flossbachvonstorch-researchinstitute.com/de/studien/gestern-hui-morgen-pfui-faktorstrategien-auf-dem-europaeischen-etf-markt/ and https://aswathdamodaran.blogspot.com/2021/09/the-esg-movement-goodness-gravy-train.html

7https://corpgov.law.harvard.edu/2022/03/16/the-false-promise-of-esg/

8https://www.bloombergquint.com/onweb/esg-funds-had-8-3-billion-in-russia-assets-right-before-the-war

9https://aswathdamodaran.blogspot.com/

11https://www.sec.gov/rules/proposed/2022/33-11042.pdf

12https://www.ecb.europa.eu/ecb/climate/html/index.de.html

13 On the economic and social consequences of anti-environmental economic policies, see Gehringer, Agnieszka "The Green Reallocation", Flossbach von Storch Research Institute Macroeconomics 13/08/2019, available at: https://www.flossbachvonstorch-researchinstitute.com/fileadmin/user_upload/RI/Studien/files/study-190813-the-green-reallocation.pdf.

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch SE. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch SE remains solely with Flossbach von Storch SE. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch SE.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch SE.

© 2024 Flossbach von Storch. All rights reserved.