26.04.2024 - Comments

Last year, using a model based on the yield curve, we introduced a strategy for hedging an equity portfolio with put options. If the stock price drops below the option's strike price, this strategy can reduce the portfolio's decline in value. Conversely, if the stock price stays above the strike price, the investor will lose the premium paid for the hedge. We applied the strategy following this rule: Buy the put option when the ex-ante recession probability exceeds 50%. Remove the hedge when the recovery probability surpasses 90%. The yield curve provided the crucial signal for these probability calculations. Our experiment showed that this strategy could generate a modest excess return over a long period while reducing volatility.

However, we issued the following warning for the immediate future in our analysis:

“The success of the hedging strategy depends on the accuracy of the recession signals. As with any model, the forecasts are based on the regularities that can be inferred from the past. Each time, however, things could turn out differently. The model would have missed the recessions of 1990 and 2020. For the current economic development, on the other hand, there is a risk of a false forecast of the start of the recession.”1

This risk has materialized. Our post-mortem analysis shows that economic forecasts are highly uncertain and that hedging strategies based on such forecasts are at least risky in the short term.

„Soft Landing“, instead of „Hard Landing”

According to our model, the recession probability exceeded 50% in April 2023, triggering the hedging strategy for our hypothetical stock portfolio. However, thanks to strong consumer spending, the US economy grew faster than expected in 2023. The industrial sector recovered towards the end of the year, and the job market remained stable despite rising interest rates. Contrary to expectations, a "soft landing"—a reduction in inflation without a recession—seemed achievable.

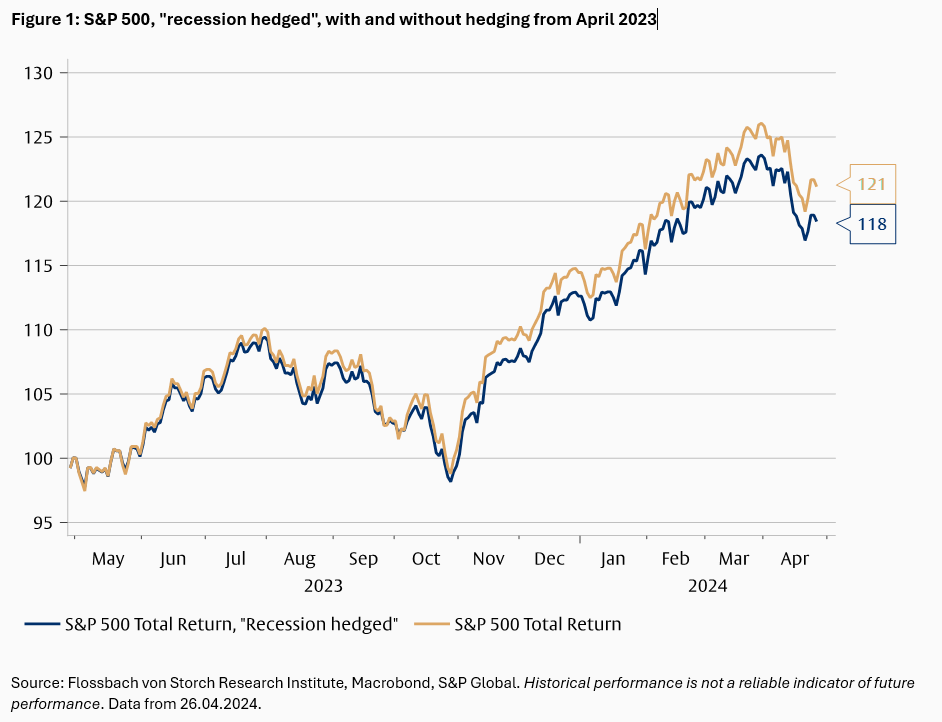

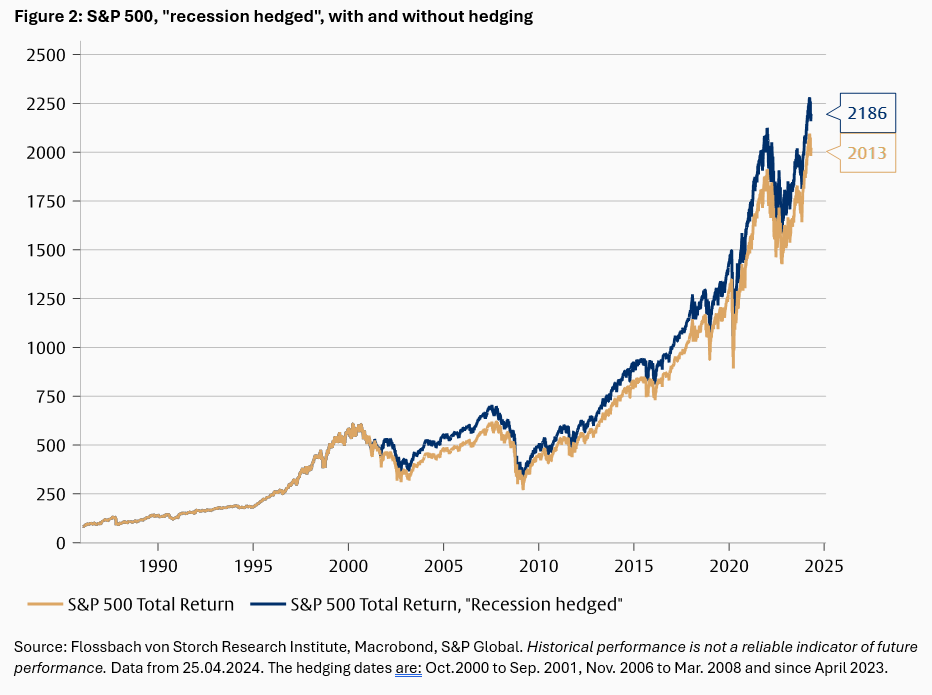

Since the hedging strategy activated in April 2023, investors would have lost the premiums for the put options (Fig. 1). Despite these losses, the total return of the portfolio, which has been managed with this strategy since its inception in 1986, remains higher than that of an unhedged portfolio (Fig. 2). However, the margin by which the average annual return exceeds that of the unhedged portfolio has narrowed from 30 basis points to 24 basis points due to last year's losses.

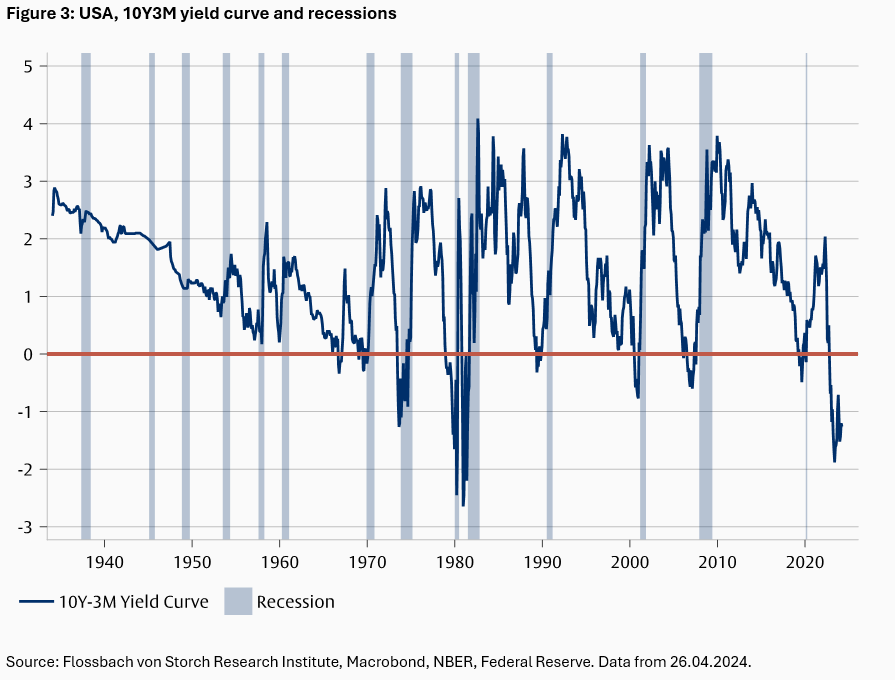

Our model was flawed because it is based on the yield curve. Since the 1970s, when the Fed gave up control of the yield curve, inversions of the yield curve have always led to a recession (Fig. 3). An inverted curve means that yields on short-dated bonds are higher than those on longer-dated bonds. This is unusual, as investors who hold bonds to maturity normally demand a higher yield for the longer commitment period. The curve therefore only inverts if investors expect short-term interest rates to be lowered in the future due to an impending recession. The sharp inversion at the end of 2022 was therefore interpreted as a clear recession signal.

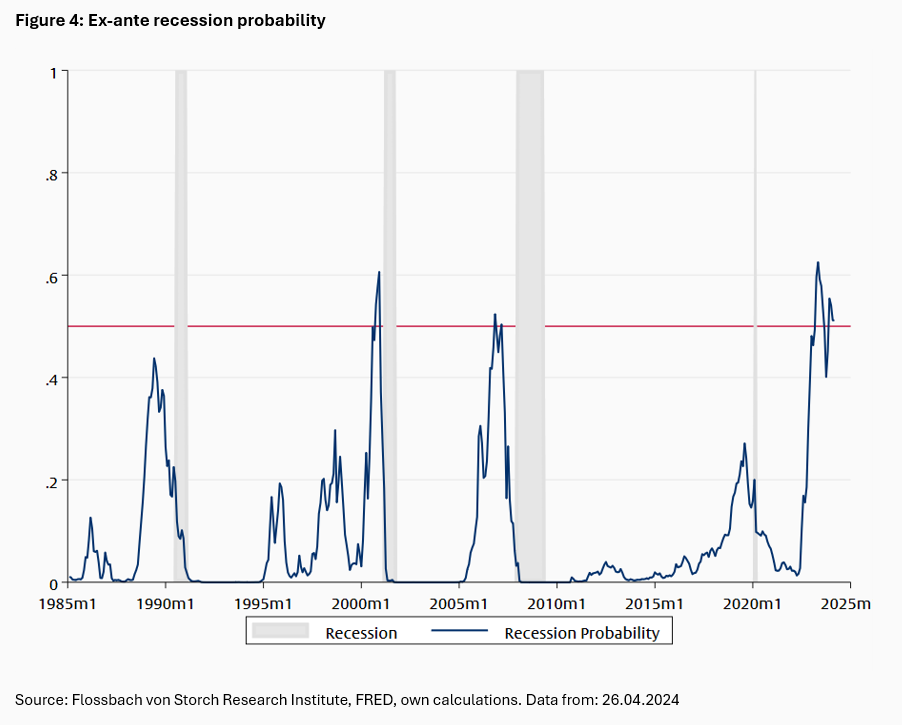

The narrative of a “soft landing” was, however, reinforced by economic data. Markets anticipated a reduction in short-term interest rates, also driven by the Fed's view that inflation had been conquered. This expectation has since been adjusted, as inflation did not decrease as anticipated. Nevertheless, a recession could still occur. Our model currently calculates a recession probability that remains higher than just before the financial crisis of 2007/2008 (Fig. 4).

The yield curve was once considered a reliable recession indicator. However, since 2022, it has been giving false signals. As a result, the premium for portfolio hedging based on these signals has been lost. This could change if the economy falls into a recession in the coming months. Then, the portfolio hedged since 1986 could catch up with the comparison portfolio. If a recession is further delayed, the accumulated surplus over time would be lost, and the hedging would have been a long-term disadvantage.

Very few investors would likely have the endurance for a very long-term hedging strategy, even if it proves successful after decades. For most, the investment horizon is shorter, making such hedging risky. Potential higher returns during a recession are offset by lower returns during extended periods of economic growth.

1 See Duarte, P. (2023), Inverse Yield Curve – and now?, Study, Flossbach von Storch Research Institute.

Legal notice

The information contained and opinions expressed in this document reflect the views of the author at the time of publication and are subject to change without prior notice. Forward-looking statements reflect the judgement and future expectations of the author. The opinions and expectations found in this document may differ from estimations found in other documents of Flossbach von Storch AG. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. This document does not constitute an offer to sell, purchase or subscribe to securities or other assets. The information and estimates contained herein do not constitute investment advice or any other form of recommendation. All information has been compiled with care. However, no guarantee is given as to the accuracy and completeness of information and no liability is accepted. Past performance is not a reliable indicator of future performance. All authorial rights and other rights, titles and claims (including copyrights, brands, patents, intellectual property rights and other rights) to, for and from all the information in this publication are subject, without restriction, to the applicable provisions and property rights of the registered owners. You do not acquire any rights to the contents. Copyright for contents created and published by Flossbach von Storch AG remains solely with Flossbach von Storch AG. Such content may not be reproduced or used in full or in part without the written approval of Flossbach von Storch AG.

Reprinting or making the content publicly available – in particular by including it in third-party websites – together with reproduction on data storage devices of any kind requires the prior written consent of Flossbach von Storch AG.

© 2024 Flossbach von Storch. All rights reserved.